Big banks such as JPMorgan, Wells Fargo, Citigroup and Bank of America have been shafting depositors with terrible interest rates – refusing to keep pace with the Federal Reserve’s rate hikes.

JPMorgan, for example, has only raised its average deposit rate by 0.21 of a percentage point, despite the Federal Reserve raising rates by 1.25% over the same period – effectively punishing customers by locking them into historically low rates required to bail out the same banks which caused the financial crisis a decade ago.

The trend is so remarkable that analysts at Goldman Sachs Group Inc. (GS – Get Report) , a rival Wall Street firm with a comparatively tiny banking franchise, published a report on the matter earlier this month, noting that rates on savings were “virtually untouched” in 2017, even as banks charged fatter payments on loans and other assets whose rates jumped along with the Fed’s increases.

Consequently, a decade after the 2008 crisis, retirees and others who shun stocks and choose less volatile, government-insured savings accounts at big banks are still getting meager returns. –TheStreet

“Some of the big banks literally have not moved deposit yields higher at any time during this cycle of Fed rate hikes,” said Greg McBride, the chief financial analyst at BankRate.com, which tracks the savings and lending industry.

In fact, none of the Fed’s three rate hikes noted by Goldman were passed on to savers at JPMorgan, Bank of America and Wells Fargo, with Citigroup passing along just 4% of the rate increases, or 0.03 of a percentage point.

Goldman’s takeaway? Shareholders in big U.S. banks are “not to worry,” Goldman wrote in the Jan. 8 reports. “Large banks are still raising cheap funds.”

To review; Home lenders and “too big to fail” banks conspired with lawmakers to remove the Glass Steagall act, allowing banks to commingle investment and retail banking operations and making them “too big to fail.” Said banks then went on a drunken lending spree as politicians like Barney Frank pushed affirmative-action lending practices, while insisting that Fannie Mae and Freddie Mac were in great shape. This was very disrespectful to the stability of America’s financial institutions.

Of course, in order to keep banks alive, the Fed had to use trillions of taxpayer dollars and drop it’s target rate to a historically low zero percent to avoid what Ben Bernanke and Hank Paulson warned Congress was sure collapse were they not to act quickly.

And now – the same banks which created the crisis and then took taxpayer money during the crisis, refuses to reward savers now that the crisis is “over” (until it’s not) – driving up profits as they use the cheap deposits to fund loans written at the new, fed-hiked rates.

Partly as a result, JPMorgan’s net interest income – the difference between what it makes on loans and other interest-earning assets and what it pays out on deposits and other borrowings – jumped to $50.1 billion in 2017 or a 15% increase from 2015 levels.

For “retail, checking and core savings, there’s been little to no movement” on deposit rates, Marianne Lake, JPMorgan’s chief financial officer, confirmed to bank-stock analysts this month on a conference call.

She signaled that regular depositors might again see little improvement in 2018 on their savings rate, at least relative to the Fed’s expected rate increases of 0.5 percentage point to 1 percentage point.

“My expectation, just given where we are, in the absolute level of rates, is that on the retail space, we would still see a lot of discipline,” Lake told the analysts. –TheStreet

Smaller banks are the place to be

According to BankRate’s McBrde, higher deposit rates can be found at smaller banks and online financial institutions, which have been forced to pay higher rates to attract deposits. “They don’t have a branch on every corner, ATMs everywhere and their name on the stadium,” said McBride, adding “You’re not going to be able to out-market the big banks, so you pay a higher rate on deposits and compete that way.”

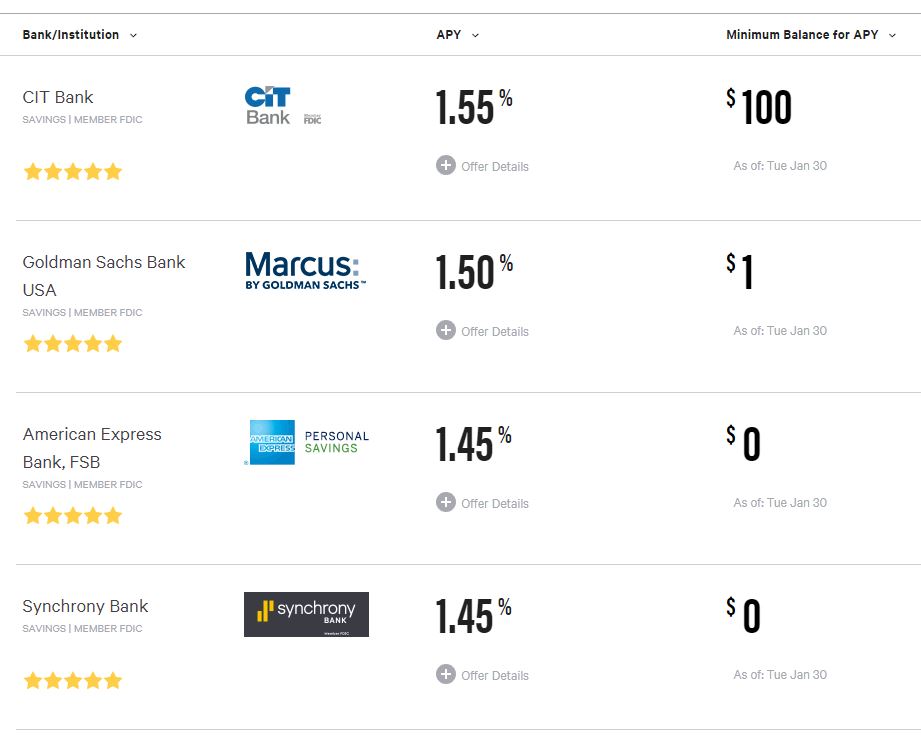

According to Bankrate, the top four savings rates can be found at CIT Bank, Goldman Sachs’ Marcus Bank (which wrote the analysis referenced in this article), American Express, and Synchrony Bank – the largest provider of private label credit cards in the US to brands such as Amazon, Walmart, Lowe’s.

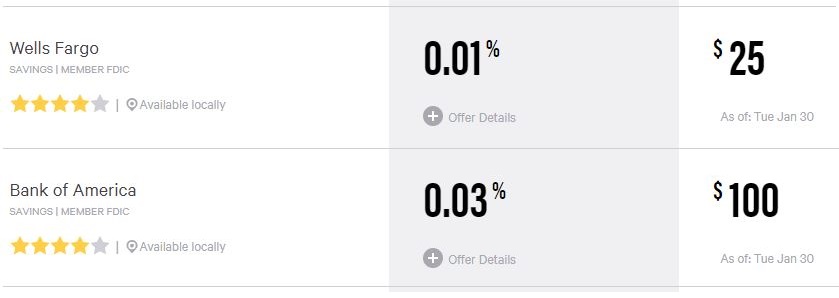

Meanwhile, Wells Fargo and Bank of America clock in near the bottom of the list.

Bank of America CEO Brian Moynihan justifies his bank’s crappy deposit rates by pointing to all of the wonderful services and conveniences offered by their savings accounts, which apparently can’t be found elsewhere. Moynihan also points to an increase in average checking account balances – suggesting that savers are more interested in safety than return on capital.

Citigroup CFO John Gerspach said that the low deposit rates are a “reflection of the state of competition” between banks. “Given deposit rates have been largely unchanged following the December 2017 hike, strong industry deposit growth suggests larger banks continue to have little problem raising cheap funds,” wrote the Goldman analysts.

In previous periods, top-yielding savings accounts kept pace with the Fed’s increases, and would anticipate rate hikes by competitively raising their own payouts in advance according to McBride. Now, the top payers have a correlation with the fed of around 0.5, and the rates are dismal.

If and when the much talked about volatility rears its head in 2018, any hopes savers had of higher rates on their cash will be sadly disappointed.

If you enjoy the content at iBankCoin, please follow us on Twitter

the fleecing continues

Meh. It’s always risky to rely on the return of a single asset.

People that diversified their savings into productive assets like stocks and bonds have done remarkably well.

Are you a communist? A shadow russian agent?

Honest question. after all who complains about banks actually making bigger profit off the sleepy assets not producing anything? It’s either capital is put to work or else be prepared to get it seized by the ones who are willing to put them to work (ie: banks).