I haven’t yet put out this December report until now because we are testing the boundaries and I wasn’t sure if we were going to see a new signal. We are very near overbought on a weekly chart and we are testing the upper boundaries of the downtrend on the monthly chart. With a significant enough move upwards the trend will change on a monthly basis, but with smaller a move upwards we will reach overbought in the weekly charts without changing the monthly trend. Much of this could change relatively quickly to signal that you should be either more cautious (overbought weekly without a trend change in monthly) or more aggressive (If a new uptrend on the monthly chart is signaled. But being that we are 7 days into December, if I wait until a signal changes there will be no December report at all so I will just tell you to be flexible in this volatile market that does not need much volume to fuel large moves due to the low mutual fund cash levels.

Additionally, I will be providing a more detailed trend report for 2012 later.

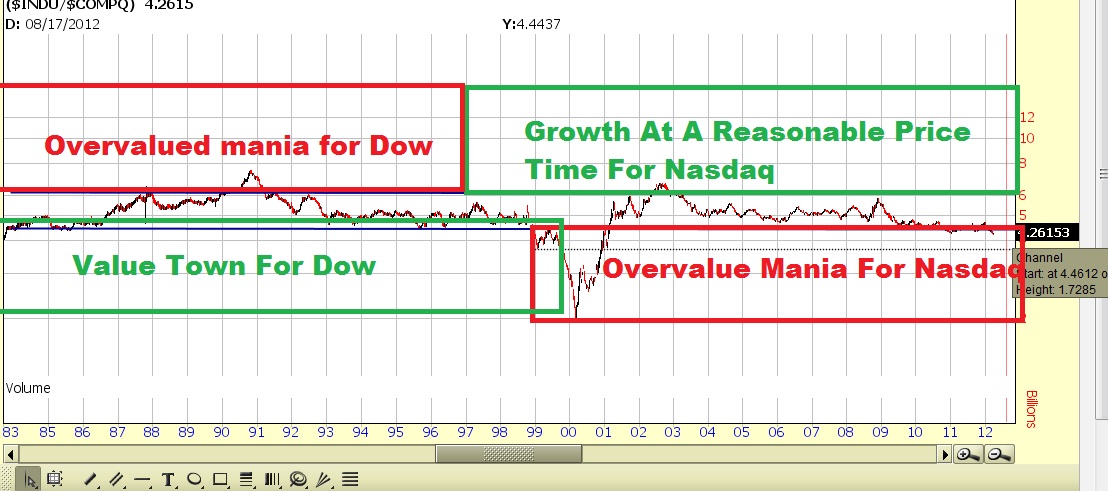

Some contrarian signals worth keeping an eye on in the future will be that dow/gold is fast approaching the long term support and I suspect we see gold pause in 2012

Also relevant is that it is down in the 50 to 90% range decline that you tend to see when bubble’s deflate. However, dow/gold has a history over the last 100 years of making such extreme moves, so perhaps this could be considered somewhat “normal”.

The 10 year treasury yield is coming off bubble highs that are not typical and are now also in the 50% to 90% decline range. Although there were days below the level, it has so far failed to produce a monthly close below the Jan 1941 low of 1.95. Right now it looks like we are essentially testing the lows on the yields.

keep track of updated 10 year treasury yields here.

I believe betting on higher yields is probably not the best idea when the market is looking weak, although there is still a chance yields could perhaps bottom in 2012, but more importantly it represent high risk in bonds that many people may not be aware of. Additionally, Low interest rates typically mean low expectations for stocks and growth as investments are bought on a relative basis. If you get a 3% yield putting your money in the bank and a 5% yield for a 10 year treasury you will need more than just a 7-8% yield to justify investing in stocks. Stocks will need to be more undervalued to justify the investment, or the expectations of growth must be higher. However, if you only get 1% interest at the bank and 2% interest in a 10 year, a 7-8% yield seems much better, and stocks should be considered much more attractive when bond yields are low (if you still expect them to yield 7-8% overall return), especially if expectations of growth rise in the future as wealth transfers out of bonds and into stocks.

Mutual fund cash levels are still near significant lows which is in contradiction with dow/gold and low interest rates being at ‘lows’. As a result I suspect we could see an extreme move at some point until these contrarian indicators are more in agreement. The path of least resistance seems to be lower, taking mutual fund cash levels higher… As the euro problems eventually reaches some kind of culmination at least in the next few years.

Liquid Assets of Stock Mutual Funds

Percentage of total net assets

http://ici.org/research/stats/trends/trends_10_11

July 2011 3.3% cash

August 2011: 3.4% cash

Sept 2011 3.8%R

Oct 2011 3.5%

(november 6.4, December 6.6?)

“The surveys of 56 leading investment houses in the United States, continental Europe, Britain and Japan showed a typical balanced portfolio held 6.6 percent of its assets in cash, its highest since at least December 2010, from 6.4 percent last month.”

http://news.yahoo.com/investors-brace-2012-higher-cash-stocks-reuters-poll-142220114.html

I don’t know if the spike up in November and December based on the survey can be reliable, but if so they have at least begun to take measures to raise cash and it would be a lot more healthy time to own stocks if true than it was in July.

Levels are still fairly low. This means there isn’t much left funding the rally and that the market is both prone to volatile moves as well as an eventual correction, or temporary bear market. Much like the end of any bubble when there is no longer cash to fuel the rally, a panic is more probable in this environment than in an environment where there is lots of cash on the sidelines. However, that is an over simplification as mutual fund cash level is low because money is flowing in and the federal reserve is currently expanding the money supply. The question is whether or not both public and private debt will continue to rise at a fast enough rate to increase the money supply. At some point it is likely it will not, which is why this is such a contrarian indicator that is more a signal of caution than a signal to trade on.

With Macroeconomic environment structurally unsound and the ECB forcing the rest of the world to print rather than making the ECB have the ability to have a more elastic money supply, they are delaying what should turn out to be a pretty significant problem at some point. I think we will see destruction around mid 2012 before a very significant low takes place most likely both in yields and real estate and possibly stock prices. The federal reserve’s actions have lulled mutual funds into complacency. You really could argue the decline of cash reserves has been in play since the early 90s

. That certainly doesn’t have much on the 30 year decline in bond yields though which I think is most likely out of these to bottom in 2012, which means bonds are actually quietly becoming a “higher risk” investment (relative to it’s return) in spite of people viewing them as the contrary.

. That certainly doesn’t have much on the 30 year decline in bond yields though which I think is most likely out of these to bottom in 2012, which means bonds are actually quietly becoming a “higher risk” investment (relative to it’s return) in spite of people viewing them as the contrary.

This could be seen as a bullish trend in treasuries, except for the fact that much like treasury bonds, it is historically very low and the trend is getting stale, and it too has declined well over the 50% requirement for a bubble to deflate, and the yields have the clear characteristics of a blow off climax, exponential top that a bubble has, followed by a sharp decline of over 50 to 90%, which hits the previous lows or undercuts the lows.

You probably don’t want to chase multidecade trends, but if you must, there are often a climax bottom/top to close your positions into, so hopefully for those chasing there is that parabolic move. It is an aggressive strategy, but perhaps worth considering the “greater fool” strategy if you are good at the financial game of chicken.

Believe it or not… not much has changed since the November Trend Report in terms of price trends in stocks. The stock prices continue to trend up on a weekly chart, and still have not broken the boundaries on the monthly chart. The limits are being pressed though and significant movement to the upside this month should reverse that trend. However the weekly charts are nearing overbought levels. In fact according to the slow stochastics, the dow is currently just barely overbought. The daily chart shows slow stochastics are at overbought levels as well furthering the case to be made of reducing risk. I would take profits into this strength and remain cautious. As we close out the year, I suspect the market will be vulnerable to a cascade downward sometime in 2012, and perhaps a panic if the ECB continues to print until eventually they run out of money (unless they are given the power to print an unlimited amount, something the Germans seem to fear) in spite of the already low treasury yields in the US and low expectations. If you got more cautious near overbought levels and then you rebalanced and got a little less cautious you should be able to ride the wave the right way.

There are many issues involved and eventually it connects towards being a political problem.

Things to look for to change the structure of the problem are

1)The ECB is given power to operate more like the Fed with an elastic money supply (power to print at will to prevent a bank-run).

2)A central Euro Bond is created

3)Mutual funds raise significant amounts of cash over time so that a sell off doesn’t risk further selling by everyone simultaneously.

4)The structure of leverage needs to be greatly toned down or it needs to be clear who can cover the obligations.

If an investment bank that sold derivatives to someone and the bank suddenly can’t pay, who fits the bill? Does the person buying derivatives even know who has the other side so they know whether or not they will get paid back or so they can attempt to price in the risk of not getting paid? Or do they just assume everything is okay and become complacent? What about those betting heavily on the decline of the bank that goes down, now how many more people betting against the failure on excessive leverage are in trouble? What about people with deposits at the bank who’s deposits were used to speculate on derivatives? What about all the debtors if you suddenly have a shortage of the cash? Bank runs would previously happen when something like 6% of the overall cash supply is withdrawn all at once, and the fed was designed to step in to prevent this from happening. The ECB has a limited ability and could eventually run out. But there also is some amount of change in each derivative’s underlying asset value that if exceeded, a derivative run could occur (depending on the derivative, the exposure, the overall amount of leverage, and how connected each asset is to each other and each investment bank is to another and so on). Well judging from the last bailout, it appears that tax payers and consumers and eventually bond holders are on the hook to some degree. Not 100% because Lehman didn’t get bailed out. TARP money and AIG bailout and Bear Sterns via non recourse loan by the federal reserve and what have you.

5)If the federal reserve is just going to print the money, this could bring up another problem of skyrocketing debt to cover the panic type events, and if so it is more reason why debt should only be allowed in times of national emergency, because how can you suddenly fund payments for potentially as bad as many times the global GDP without consequences? But realistically, that is not the system. The system does unfortunately have the side effect of perhaps too strong of central government.

There are many structural problems that can’t easily be satisfied without reform, but extreme reform that essentially would ipe out the system to start over would probably be too destructive.

While the weekly chart is actually showing a bullish divergence as it makes higher highs in the slow stochastic while price makes lower highs, the monthly chart continues to show higher lows in price while the RSI makes lower lows. The price action is not to be trusted. The important thing remains the trend which also is in conflict with the weekly chart showing an uptrend still. The monthly trend is more accurate and results in greater moves but a longer time period. However the weekly is still to be respected. The allocation in the trend trader is cautious and will get more cautious if we hit overbought on the weekly chart without breaking the monthly trend. Additionally, it is worth watching the trend channel shown above, although you should still be cautious because of the likelihood that this is going to be a false move due to the bearish divergence, you should still watch the key levels of support and resistance, perhaps to slightly adjust or use it to rebalance and reassess your positions. I believe a decline is still coming, but you must remain flexible, and betting against assets going up is traditionally a low probability trade unless everything lines up, so the alternative is to have a larger “risk off” position and minimize the “risk on” position unless the ideal set up occurs. Unfortunately Things just aren’t in alignment to make that kind of bet. Instead, being cautious and participating in a mixture of “risk on” (stocks, gold, oil, commodities, etc), “risk off (currency trades, US treasury bonds, Cash) and relatively “delta neutral” (complex options strategies, or else arbitrage plays, bullish and bearish bets in anticipation of earnings, pair trades, post earnings pair trade plays, etc), with a cautious or aggressive weighting depending upon the signals you are getting makes sense. At the moment it is one of caution. Should the crisis escalate to panic due to a number of things such as euro problems, defaults, or further US downgrades setting off fear of a global contagion, not only risk on assets are at risk but even potentially some arbitrage deals that may be dependent upon financing may have difficulties. Others may get cold feet… If possible they will find a way to weasel out. Such recently happened between Skyworks Solutions who was going to buy out Advanced Analogic Technologies. Skyworks made accusations of “fraud” and that the numbers weren’t correct. Advanced Analogic fired back with a counters that they weren’t honoring the terms of the agreement. Finally Skyworks Solution said it would buy it for a slightly lower offer ($5.85 instead of $6.0+). In another deal TAM and LFL were in agreement of a deal until a regulatory investigation delayed the deal “6 to 9 months” and that the merger would likely not take place until the 4th quarter. It still has not gone through. This type of things happens. Deals still go through they just get delayed. This makes using options as leverage to beef up these returns more risky, esp when the market is vulnerable, and the annualized return could end up significantly lower than initially expected if the deal gets delayed. As such, these “risk arbitrage” plays are not as “neutral” to market conditions as you would ideally hope, especially when market is vulnerable, however they do still have the ability to help to lower your correlation and boost your return in all market conditions. They do have a very high success rate in all conditions if you don’t measure a “delay” or a lower offer as a failure. Talking about arbitrage is something that books have been written on and cannot be covered briefly, but the concept is the important part. The concept is that REDUCING correlation is often productive to boosting your return on risk even if the return of that other asset is less. Some misunderstand this and say “diversification” or slightly better “multiple asset classes” for this same reason, but that only sometimes and only partially reduces your correlation. A portfolio with a return of 7% gain with a 2% drawdown is better than one with a 10% gain and a 4% drawdown. Use leverage and your 7% return becomes a 14% return with roughly 4% drawdown (plus leverage costs), or use less leverage and be somewhere between if you can’t handle it. The return on risk is what is important and the LEVERAGE is what you use to determine the magnitude of that risk/reward profile that determines your return. Reducing correlation through relatively “delta neutral” strategy(such as arbitrage), as well as owning a mixture of “risk on” and “risk off” is a great way to boost your return on risk. Now taking the THEORY of this and putting it into practice is another issue. If you pick individual stocks, there are risks among those companies. You might have the downside of investing in some bad companies in with the good if you just pick an index fund such as the SPY, and you might take on stock’s individual risks to a limited degree but you avoid the risk of a real shocker that can wipe out a huge portion of your cash such as accounting fraud, or an FBI raid and findings of illegal activities, or a major lawsuit, etc. Increasing positions reduces this risk but has the cost of a lot more fees and it is more difficult to manage more positions and you risk making mistakes. So it’s a trade off you have to deal with. I prefer using ETFs mostly with a few occasional individual value stocks with a small amount of capital and even smaller amount of “option gambles”.

In conclusion of this trend report, a lot of cash and “risk off” assets are advised and confirmed with the monthly trend. The “arbitrage” deals must be picked cautiously and you should make sure they are not heavily dependent on financing.

Comments »