They were supposed to report crummy earnings. After all, we’ve been led to believe the banks were toast and that earnings were going to be the worst since 2009. Jamie Dimon is built from a different cloth.

JPM crushed it by nine cents and beat on the top line as well. The stock is ripping higher in the pre-market, higher by 3.1%.

Via Briefing.com

- Reports Q1 (Mar) earnings of $1.35 per share, $0.09 better than the Capital IQ Consensus of $1.26; revenues fell 3.7% year/year to $23.2 bln vs the $22.87 bln Capital IQ Consensus.

- Tangible book value per share of $48.96, up 8%.

- Average core loans up 17% YoY and 3% QoQ.

- Net interest income was $11.7 billion, up $723 million, primarily driven by loan growth and the impact of higher rates on cash, partially offset by lower investment securities.

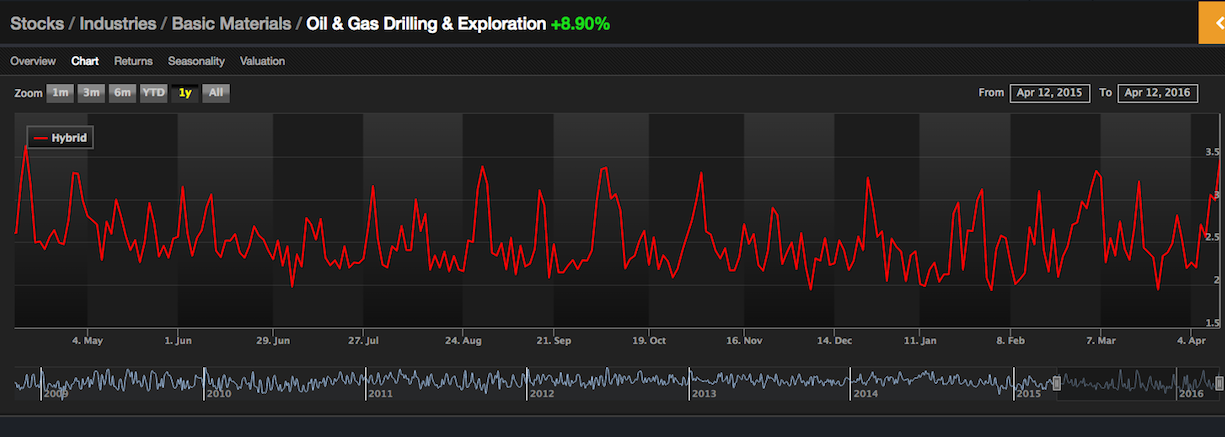

- Provision for credit losses was $1.8 billion, compared with $959 million in the prior-year quarter, predominantly due to reserve increases in the current quarter versus reserve releases in the prior-year quarter. The reserve increases in the current quarter reflected an increase in wholesale reserves of $713 million, primarily driven by downgrades, including $529 million in Oil & Gas and Natural Gas Pipelines, and $162 million in Metals & Mining (Guidance was for approx $500 mln in Oil and $100 mln in Gas).

- C & IB Unit

- Banking revenue was $2.4 billion, down 19%.

- Investment Banking revenue was $1.2 billion, down 24%, on lower debt and equity underwriting fees, partially offset by higher advisory fees.

- Lending revenue was $302 million, down 31%, reflecting mark-to-market losses on hedges of accrual loans and lower gains on securities received from restructurings.

- Markets & Investor Services revenue was $5.7 billion, down 13%, driven by lower Markets revenue, down 11%.

- Fixed Income Markets revenue was down 13%, reflecting an increase in the Rates business which was more than offset by lower performance across other asset classes.

- Equity Markets revenue was down 5%, reflecting weaker results in Americas derivatives, partially offset by strong results in Asia derivatives.

- JPM plans to increase capital return in the first half of 2016 as the board approved an incremental $1.9 billion in share buybacks.