I’m all for crazy. But this morning’s Goldman Apple rationale steals the show. They’re projecting Apple will switch into a services company, ditch the whole growth model, and focus on monetizing their business.

Why does Goldman think this?

Umm, just because.

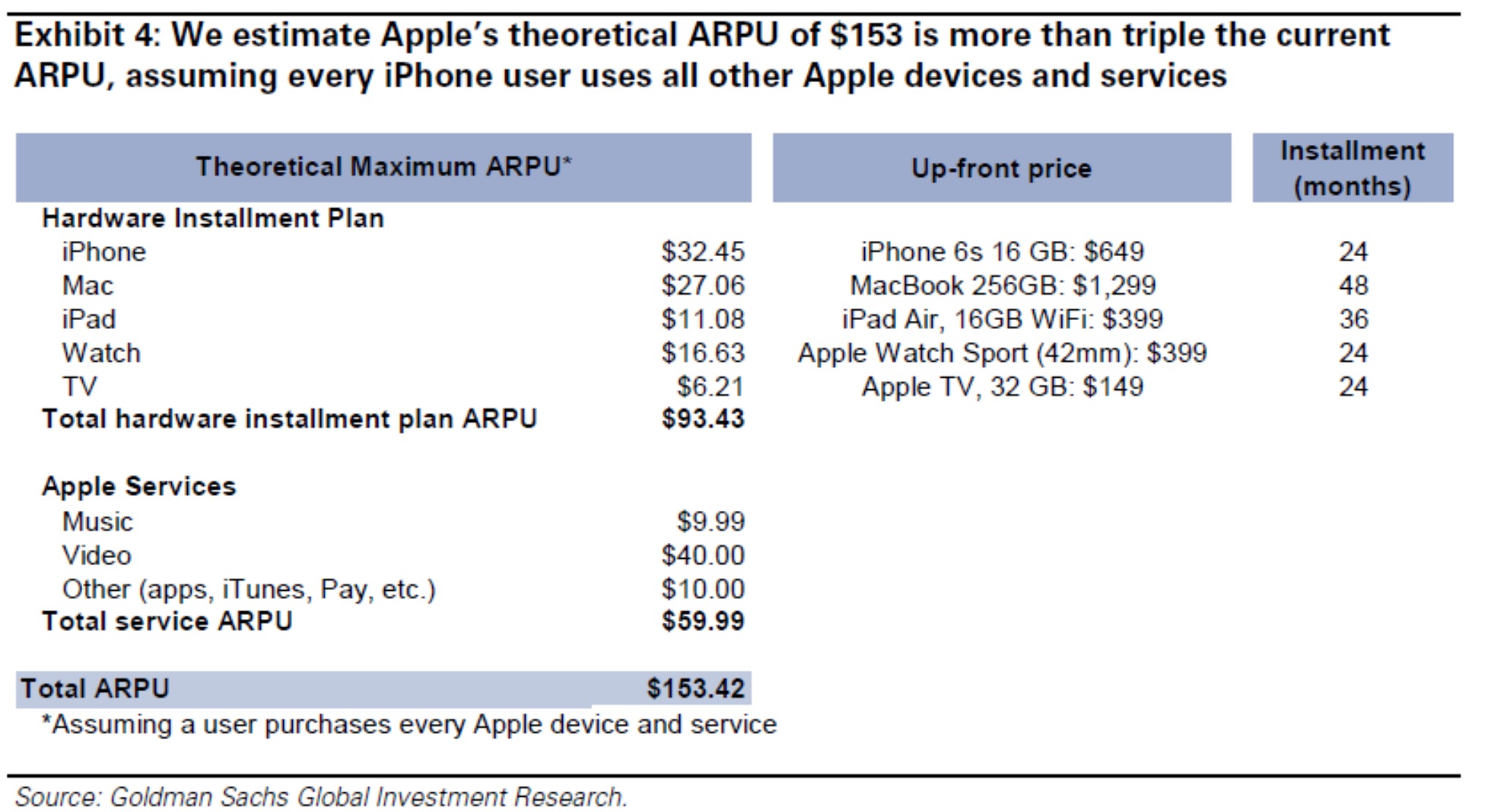

Theoretically, Apple could transition other products to installment plans as well, and charge customers a monthly bill that also includes its other services such as Apple TV and Music. We think a potential live TV service from Apple would be a key enabler of this transition to an “Apple-as-a-Service” business model.

They even took the time to lay out their fantasy island projections, suggesting that revenue per customer could jump from $41 to $153 (LOLz).

What does it all mean, man? It means revenues (takes pull on marijuana filled blunt) can jump to $553 billion by 2017, from the current $233 billion.

Their price target is $163.

If you enjoy the content at iBankCoin, please follow us on Twitter

They’re quoting you on zerohedge now. http://www.zerohedge.com/news/2015-11-18/it-will-sune-be-over-axiom-says-sunedison-credit-event-appears-more-likely-sees-pric

Tyler has good taste.

Is there an edit required in the third sentence?

yes, thanks

Very funny post. Creates a great image of the analysts lolling around and coming up with their stuff.

Good Lord that makes 2 of my holdings on Ball Sachs conviction list ( extra KMI). Should I commence call selling put buying?

GS also initiated coverage of BLUE with $165 price target. Closed yesterday at $79.61. WTF?

Because if there’s one thing people love, it’s being charged monthly subscription fees…

I wonder if they were channeling the Big Lebowski when writing the report. I’d like to believe so.

That report is right on, man. Mind if I do a J?

Is there a name associated with the report so we can publicly humiliate him/her at some future date?

I agree with their thinking, for what it’s worth.

you can agree with the thinking all you want. That still doesn’t make it likely to happen.

What makes this analysis even more absurd and quite frankly odd, is that off revenue increase of around 140% they expect the stock to rise by only $47. Truly remarkable… My bet is someone from Citi or JP wrote this in the guise of a Goldman analyst.