“Citizens of the U.S. and the world are heading into a future that few have prepared for. It will also turn out to be much worse than most realize as it will be unlike anything we have witnessed in the past.

Part of the reason we are in such a bad fix has to do with the compartmentalization and specialization of our modern educational and economic system. There are many intelligent people in the market doing smart things; however, they often have no clue on what the hell is going on in other industries or professions.

For example, there are many precious metals analysts for whom I have much respect, but who fail to understand the energy industry. Now, I imagine there are a few analysts in the precious metals Biz who do understand the ramifications of Peak Oil, but it may be more rewarding for them (financially) to keep their traps shut.

And then we have individuals who specialize in “Technical Analysis.” Many who have read my posts and articles realize that I believe that technical analysis is worthless in a rigged market. I also believe the big price moves in the gold and silver are more fundamental in nature than technical.

I explained this in detail in several recent articles by comparing the price movement of oil to that of gold and silver. I have republished two charts below that show how the price of gold and silver moved in parallel with the price of oil in the 1971-1980 time period:

Here we can see that silver and gold moved in tandem with the price of oil. Many investors still regurgitate the notion that the Hunt Brothers were solely responsible for pushing the price of silver to record highs in 1979.

If that was true, then who was pushing up the price of gold? Or, how about oil… who was responsible for increasing the price of oil by a factor of 10, from $3.29 in 1973 to $36.83 in 1980? If I were to ask these questions of someone who blurted out that the Hunt Brothers cornered the silver market… they would get a blank stare back from me, because they have no clue.

My articles get around the Internet. Someone on another blog made the comment, “comparing the price of silver to oil was silly”. They said it makes just as much sense to compare the price of silver to the price of potatoes.

Everyone is free to have their own opinion, but the fact is that energy is the key that drives the global economy. Energy allows silver to be mined, refined, transported, minted, traded and consumed. I happen to believe the price of energy controls the price of silver, and other commodities as well, for that matter.

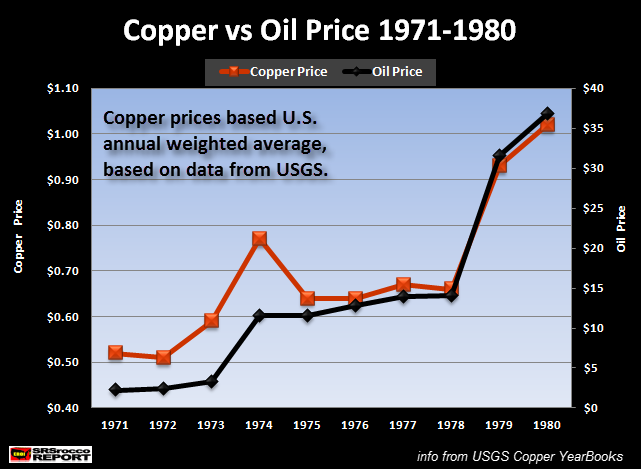

Let me see if I can provide another example that may win over the worst skeptics. If we look at the price movement of copper from 1971-1980, we see an interesting correlation to the price of oil:

Well… look at that. It is perhaps just another coincidence, the price of copper had a similar trend to the price of oil. As the price of oil shot up in 1979… so did the price of copper. Hell, the 1979 and 1980 copper-oil price lines are almost identical.

Copper didn’t enjoy the same percentage gains as gold or silver as it isn’t a sought after monetary metal. However, who was trying to corner the copper market in 1979-80 to push it up to new record highs? Do you ever hear anyone asking that question?

I bring up this subject so investors realize that the big price moves of gold and silver parallel the price movement of oil and are not due to technical analysis.

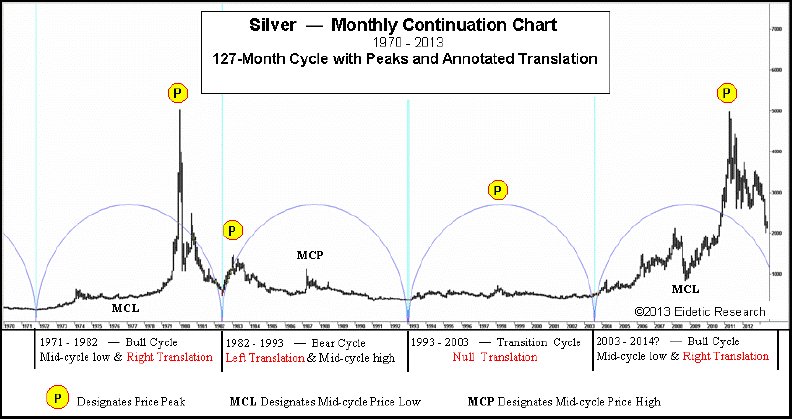

The long-term technical analysis chart of silver below is suggesting that cycles and waves may predict the future price of silver. I say throw-away the damn chart and follow the price of oil… it’s a much better indicator.

Why? Because, if you were to overlay the price of oil on this chart, you would find a similar trend-line. That being said, the price of oil is only a basic guideline to gauge the market price of gold and silver.

Due to the Financialization of the market by manufacturing hundreds of trillions of dollars worth of derivatives, fiat currency has been siphoned away from the physical market and into worthless paper garbage. We have no idea what the prices and costs of goods, services and commodities would be if the majority of fiat currency was invested directly into the physical markets rather than the $trillions in leveraged paper claims.

I would like to touch on one more subject as it pertains to technical analysis before I get into the wonderful subject of economic collapse.

In a recent article, “Silver – The Power of Thought Will Ultimately Prevail” the author Michael Noonan stated the following:

We keep moving away from discussing fundamentals because the fundamentals have not been reliable indicators in the supply/demand equation that normally determines price. Yet, almost every single article focuses on the record sales of numbers of coins offered to the public, charts showing overwhelmingly favorable statistics that favor higher silver prices, cost factors for mine production, decreasing supply relative to increasing demand.

How many times, and in how many ways can the same information be presented over the past year, and yet the price of silver languishes near recent lows?People have an appetite for this kind of information. It serves as a crutch to bolster flagging belief that silver and gold will rally any time soon.

Fundamentals are real. We are not being dismissive of their importance. Instead, we see the perception of their impact as being misplaced, for now. Ultimately, they will prevail, but the greater area of focus of a failed fiat financial system deserves center stage.

I disagree with Mr. Noonan on his current assessment of the fundamentals. While I don’t want to get into a TIT for TAT debate with Mr. Noonan on why I disagree, I believe it’s important to understand the difference between the two ideologies.

Mr. Noonan doesn’t focus on the fundamentals because they are, according to his analysis, “unreliable indicators.” Instead, he seems to suggest or imply that technical charts offer a better indicator. Now, I may be guilty of putting words in his mouth as he did not directly say that, but if you read his articles, you will find technical charts rather than fundamental analysis.

I believe that the fundamentals are everything in a rigged market…. even when the paper price doesn’t reflect it. It is more important to understand the energy fundamentals than it is to focus the on technical charts of silver. As I explained above, oil has been the major indicator in driving the price of gold and silver (and yes… copper).

Also, when investors understand the fundamentals of the energy-cost structure in the precious metal industry, they will be able to see there is a floor for the price of gold and silver. I still get investors emailing me stating that silver can go to $5.00 because it’s so cheap to mine.

In addition, technical analysis in a rigged market cannot grasp the serious problems looming in the energy industry. I just got off the phone with energy analyst Bill Powers of PowerEnergyInvestor.com… and I have to say the information he shared about the U.S. Shale gas industry is alarming. I will publish an article on this subject next week.

Let’s just say the price of natural gas in the United States is heading much higher. This will not be because of technical analysis, but rather in response to important fundamental causes, forces and data.

If you are an individual who believes the garbage forecasts put out by the Large Bloated Worthless Banks and Brokerage Houses claiming 20 years of growing natural gas production at low prices of $4.00 Mcf here in the U.S., get ready for a rude awakening.

This is the reason Mr. Noonan’s opinion on the fundamentals are wrong. While I agree with Mr. Noonan that the “Failed Fiat System” deserves focus, peak oil is the reason the Fiat Monetary System is headed for certain death.

Again… technical analysis is worthless in understanding the ramifications of peak oil and its impact on the United States and the world going forward.

The Coming Economic Collapse Will Be Much Worse Than Most Realize…”

Full article

Comments »