I don’t have a position in DKS but I have about 50% of my portfolio tied up in retail stocks despite the economy showing signs of going utterly pear-shaped.

Investing isn’t about being smarter than everyone else. It’s about being smarter and/or faster than the masses. The idea is to find a particular set of specific measurable performance metrics or trends shortly before they become conventional wisdom then get long as you can stand and wait for the world to catch up to you.

Two important points on this strategy:

Timing is critical. Early is the same as Wrong. I want to be about a month ahead of the pack. Any longer than that and it’s time to rethink.

You have to understand the other side of your theme perfectly. When chess prodigy Bobby Fischer ran out of opponents he practiced against himself. You’d be amazed how hard that it is to compete against yourself in anything without cheating. Don’t invest until you can make a perfect case for how and why you could be wrong. Seek dissenting opinions.

My Thesis

I think this is the year Wall St rewards companies for spending on their core business rather than doing more buybacks. Specifically, I am investing in retailers that are a) growing their online business faster than the low teens rate of overall US ecommerce b) investing with the goal of seemlessly integrating on and offline… Customers don’t make the distinction between on an offline. It’s all just selling stuff. c) are willing to take an earnings hit in order to spend.

That last point is counter-intuitive. I want to be long stocks that are warnings-proof. Short interest at DKS is up >3x since last May. Most of them were betting earnings would miss. My bet (on retail in general) is earnings misses will be foregiven. If that happens the shorts are hosed. They have to cover because their catalyst (earnings miss) didn’t work.

We’ve seen Best Buy, Macy’s and JWN go up after bad reports (though in the case of JWN it took a while). So when DKS missed and fell 8% pre-market my question wasn’t why shares fell (they missed, duh) but if the stock could bounce, ala BBY:

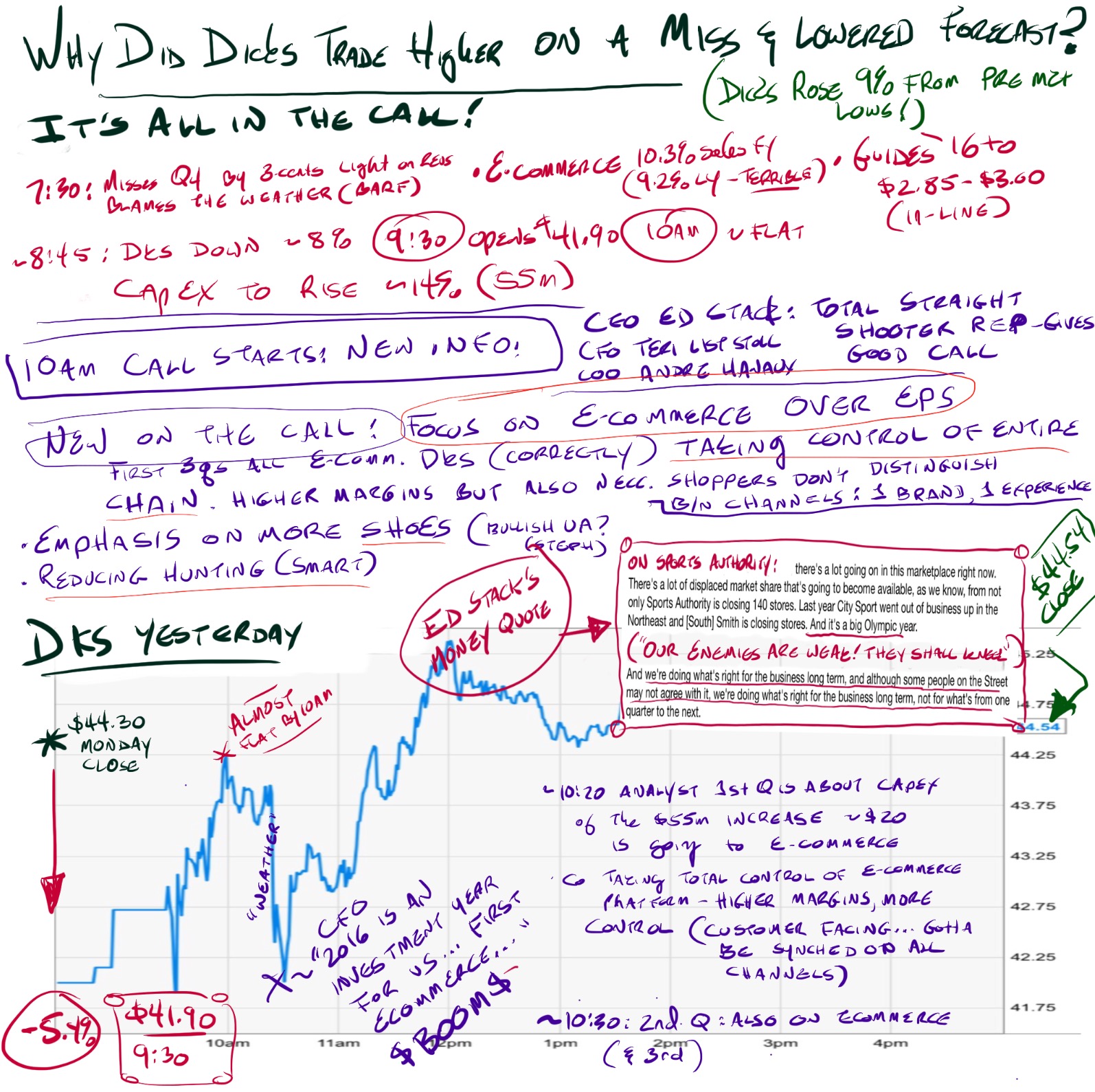

It did. Here, in nearly indecipherable but surprisingly useful form are my notes on the the surprises during the conference call that triggered a 9% rally from when DKS reported to the close of trading. If the rest of the retail sector continues to trade this way you can expect to see a lot more people getting on the retail train.

Those are the folks I want to sell to at higher prices.

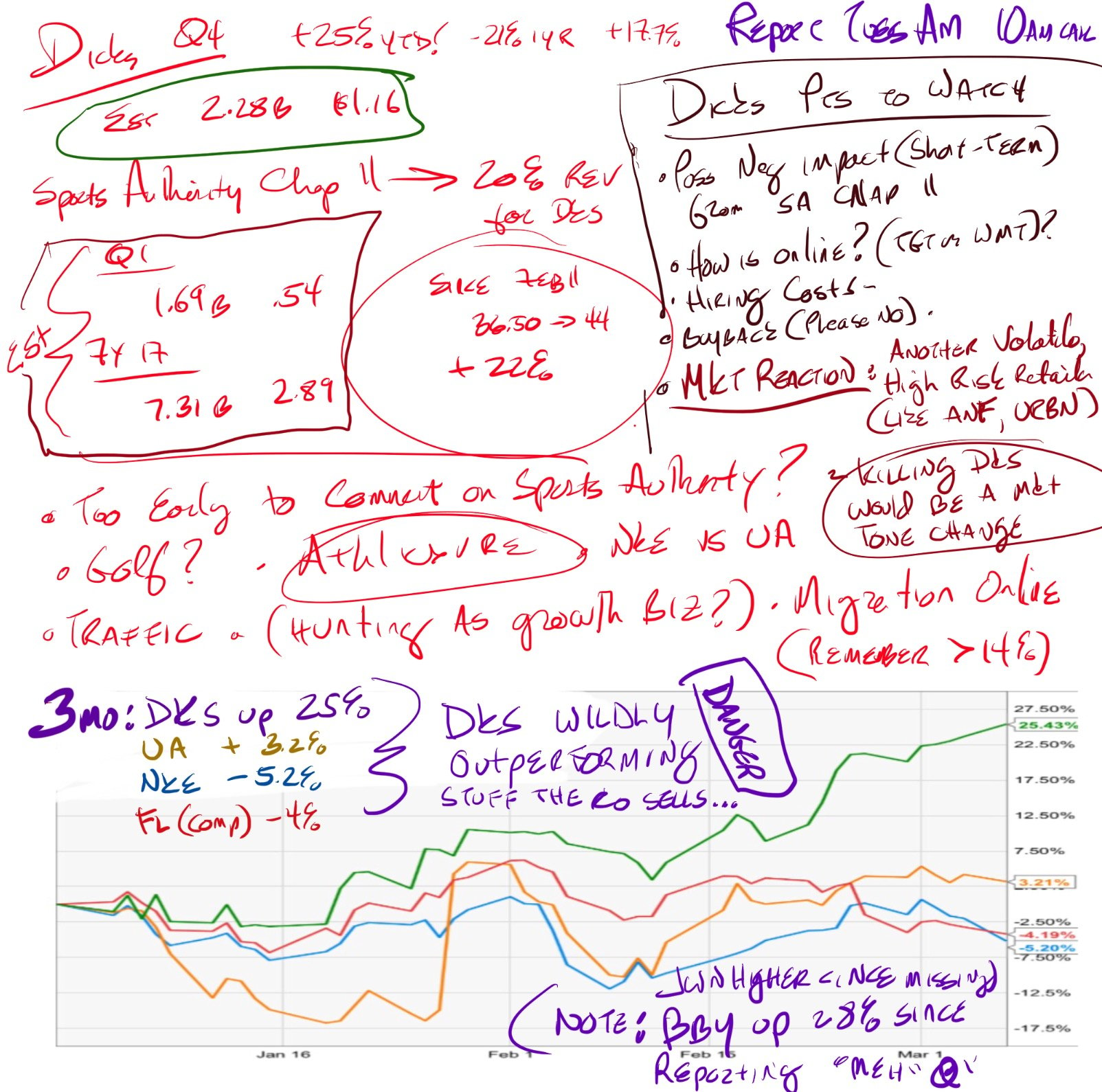

Estimates for Q1 stand at 54-cents on $2.28b. Full year is $2.89 on $7.31b. The co already warned for Q4.

Here’s my real-life pre-release cheat sheet*:

At this point you may be sick of retail coverage. You may prefer sexier stocks doing business in the cloud or selling $10 hamburgers. Or maybe you’re looking to scrape some goop off the bottom of the wreckage field that is energy.

Maybe you want to debate Apple some more or chase Tesla. Can Disney regain its downtrend?

I get it. Those are sexy stocks in the headlines. I was asked me about Palo Alto Networks as I was getting prepped for a routine colonoscopy last week. (The answer: “Too much risk just to get back to even. Go for ANF if you want the same danger seeking rush with more upside. Can I get the Michael Jackson drug now?”)

If you want cocktail party chatter stocks go play with Valeant. I hate cocktail parties in general and giving stock picks at said parties in particular. Professionally speaking I’m in it for winning, making money and scratching my creative itch, in no particular order.

Retail is where the money is in stocks right now. That alone makes the sector sexy as far as I’m concerned but I’m sort of a hussy that way.

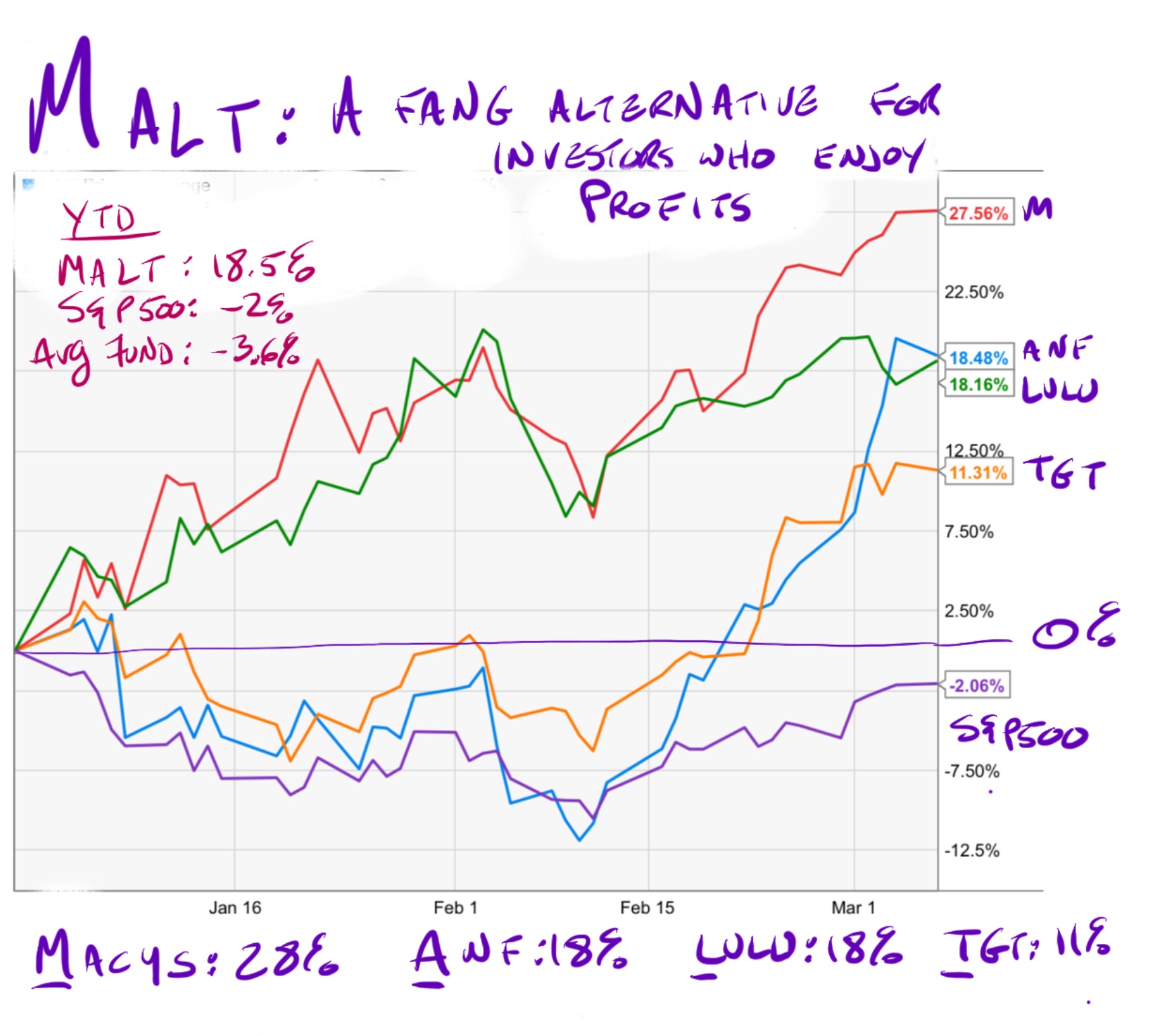

5 minutes ago I dubbed this basket of stocks-I-own MALT just because I wanted to respond to something I heard my friend (name drop!) Becky say on the TV. It stands for Mr Awesome Likes These. Later I realized MALT is also the first initial of these stocks in order of performance year to date (Macy’s, ANF, LULU and Target).

I prefer Mr Awesome Likes These but the company initials might make a better mnemonic strategy.

Dick’s

Retailers are shaking off horrendous earnings and exploding to the upside when they hurdle the lowest of bars. URBN thinks it’s a pizza chain and shares are up 10% after they avoided blowing up by more than expected last night. These stocks move big and have been reacting well. In part that’s because merchants started reporting near the market lows February 11th.

Something else is going on here. The retailers were sticky before the market cratered. Dicks is up 25% in 3 months, a period during which they guided lower! The stock is way outperforming shares of the companies whose product it sells. Nike and UA have been slumping while Dick’s keeps chugging along.

BBY shares are up 8% since the miss. They never really even dropped. JWN sounded like lost children on their call and the stock has already recovered. With futures lower this AM and Dick’s set to report any minute I think DKS shares are your market tell of the day.

There are a lot of moving parts to this story. If you do conference calls, tune in to DKS through the webcast at 10am. Management is a hoot (the quarter they chucked golf under bus is legendary) and the company has its finger on the pulse of things you wouldn’t expect like fashion via Athleisure.

Some stocks are for buying (like the MALT group!). Dick’s is just one to watch.

Rememeber: it’s about guidance, stock reaction and brands.

Enjoy! And… Just because I’m not mature and it must be said… I don’t know why the company has kept the name.

I know the notes look chaotic. That was also true of yesterday’s Shake-Shack cheat sheet, which ended up mostly being a bubble shaped hamburger when I realized how insane SHAK’s valuation is. Do your best to make sense of what I’ve written. I promise there’s value in there somewhere.

Retail is a game of expectations and momentum. Tell the customer what to expect then give them just a little bit more. As long as a chain is doing that well the business (and stock) will survive inevitable setbacks.

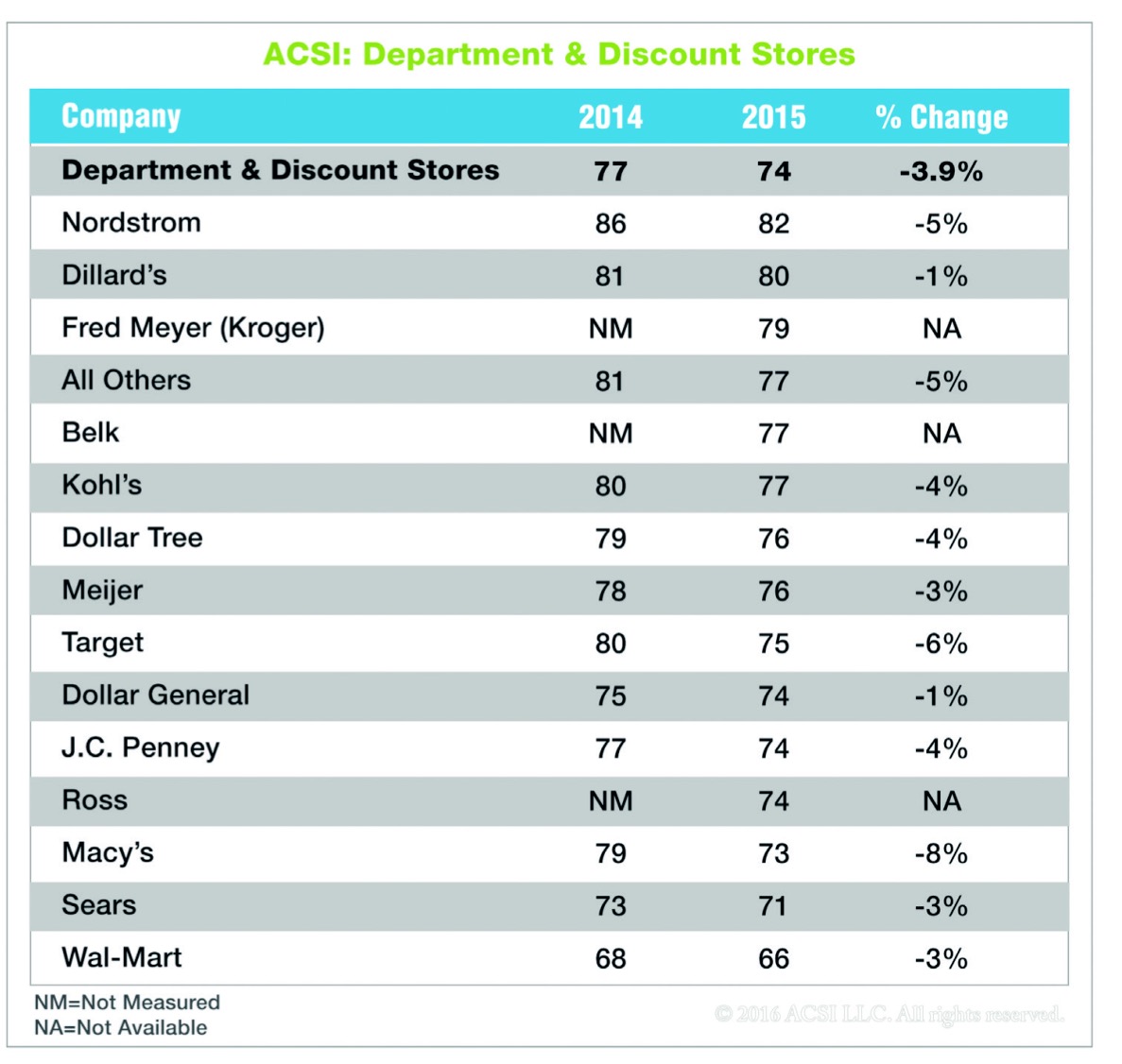

Shoppers are surprisingly reasonable. They don’t expect to have their hand held at a Target. They just want the store clean and orderly. Department stores need fancier fixtures than discounters. All grocery stores have to seem clean.

The ASCI numbers are typically fairly well correlated. In better economies customers want their arse kissed more. Not one merchant scored higher this year. I blame the Millennials and their sense of entitlement.

There are some notable standouts. Home Depot’s less capable sibling Lowe’s had the biggest drop in the survey. Only 74% of Lowe’s customers were happy with their experience in 2015, down from 81% in 2014. Home Depot stomped a mudhole in estimates this morning (in a good way) and we hear from Lowe’s tomorrow.

The fact that HD and LOW fell is also an economic tell on housing. Housing supply stores have a hard time staffing in hot housing markets. Anyone who knows how build can make more money practicing their craft than working retail.

Big Freaking Problems for Macy’s

I showed the department stores earlier but it’s worth revisiting.

Macy’s customer satisfaction drop off was the second largest in the survey but suggests a much bigger problem than Lowe’s. When I rant about retailers wasting money on buybacks it isn’t (only) because I’m an ass. It’s because I’ve worked retail. I was at Macy’s when the chain went bankrupt in the early 90s.

All this is really personal to me. When I see an 8% drop off in customer satisfaction at Macy’s I see a bunch of laid off employees sitting at home as customers go un-waited on in stores and bankers collect pennies per share on Macy’s dumbass buyback. I see a company dying. I see it all at once.

Which doesn’t make Macy’s a short. In fact, I’m long because I believe management will be ousted by the end of the year. But customers won’t come back just because some activist starts spinning off Macy’s stores. The chain will die. It can’t justify it’s own existence as it is. As the fixtures start falling apart and the place becomes a dump shoppers will stay away in droves.

The other day my lab took himself for a walk. He’s 11 and I’m attached to him the way a man gets tied into a dog after a while. He defines an era of my life.

So my heart sank when I found Dunkin’ slowly loping towards me across a street in front of an oncoming car. It’s a residential road so the neighbor’s car only bruised my knee a little when I threw myself on the hood to save a slightly decrepit animal that’s pushing 90 in people years.

The feeling of dread I had watching the scene unfold, that sense of “oh crap, I’m watching this thing die”, has lingered with me all week. That’s what I see with Macy’s. It’s an old, dumb, sort of lovable-ish animal about to unwittingly kill itself for no good reason at all.

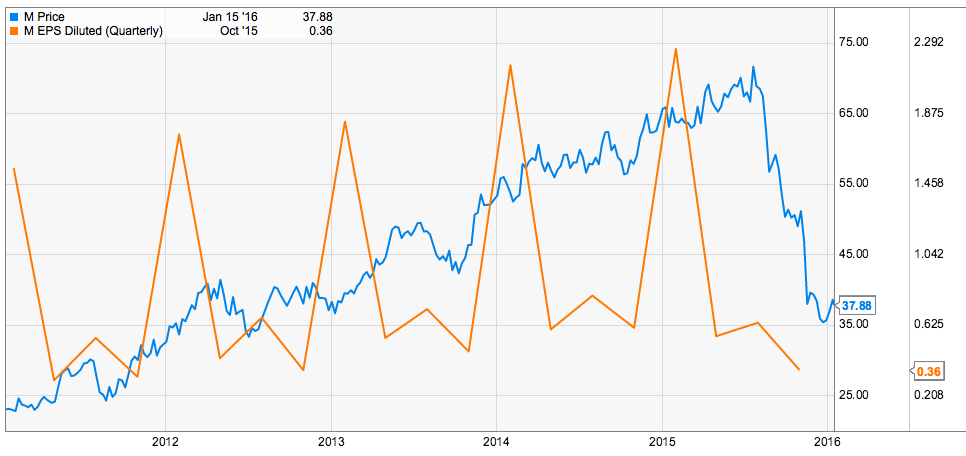

Shares of Macy’s are higher in the pre-market after the company reported exactly the type of dumpster fire Wall Street was told to expect.

Those of you who took part in last night’s investor Bootcamp know I’m long the stock. The thesis isn’t my confidence in management. Quite the opposite. Macy’s has terminal cash flow cancer. The play here is the company falling into activist hands.

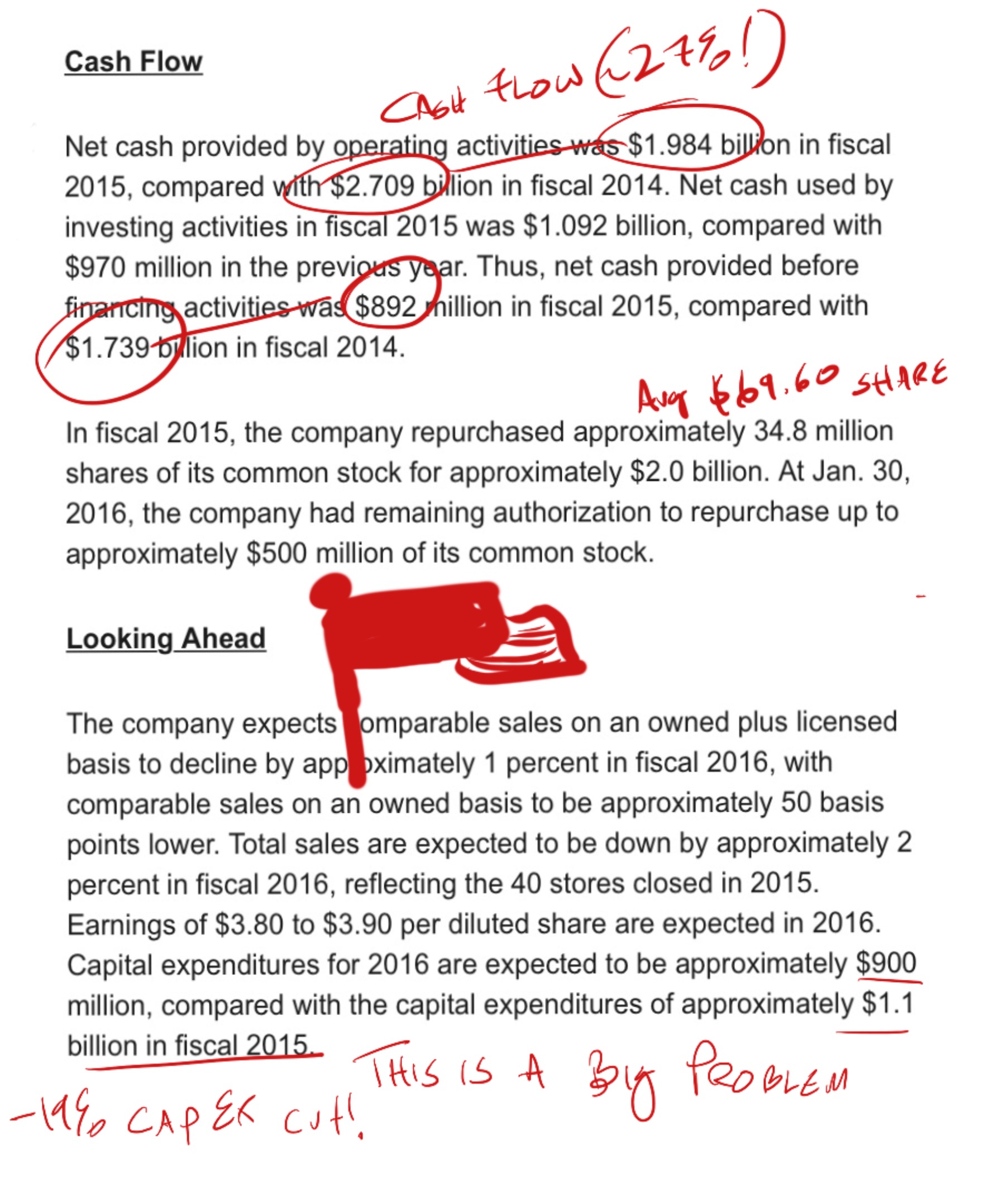

From that admittedly dark perspective here’s my favorite part of the quarter:

Cash flow from operations fell 27% last year. Despite the decline in liquidity Macy’s spent $2b on buybacks (avg cost: $69.80). They made up the difference by cutting cap ex. Cutting cap ex is death in retail. Cap ex is retail speak for store maintenance and the little touches that make a customer feel special.

Macy’s can’t afford to cut cap ex more. In the just-released ASCI report on consumer satisfaction Macy’s had by far the largest year over year decline among general merchants:

Macy’s scores lower than JC Penney. If they were running M for the long haul they would Jack up cap ex dramatically. Macy’s is going the other way, reducing spending in stores by 19%.

As my dad was fond of telling me, “a dirty store says f*** you to the customer”. Macy’s is planning to insult even more customers this year.

This isn’t a long term position. It’s a trade and it’s working. If you want to hear more sign up now for Part 2 of the iBankCoin Bootcamp.

Off to the Macy’s call… This oughta be interesting.

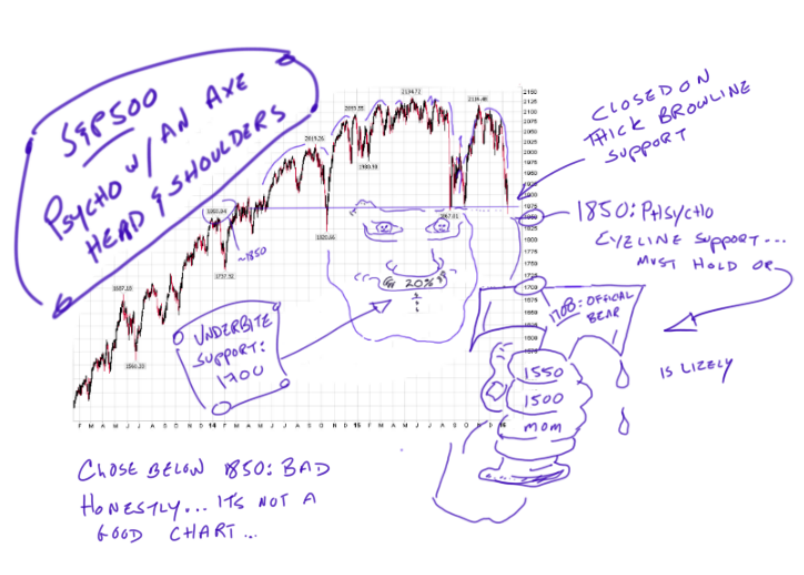

There was a little bounce on Friday. Which is to say we didn’t close on the lows.

The bullish scenario is we’re oversold, sentiment is “wetting myself” and it wouldn’t be a bear market if it didn’t squeeze the hell out of bears every once in a while. We’re down 10% in a straight line. That doesn’t mean tomorrow is “due” to move higher. That’s not how odds work.

Market days are independent, for betting purposes. Like a roulette table. Sharp reversals can and do occur within larger trends but by definition they have to be random.

A face-ripping, explosion of a rally is coming but there aren’t any cheap ways to wager on it. Calls are still expensive. Stocks aren’t cheap, or even possible to value, in theory until oil stabilizes AND China gets done having to kick traders in the ass with jackboots to get them to buy stocks in the Shanghai Comp ($SSEC). (see: China Has Us By the Wontons).

Head and shoulders, only scarier…

You want to get long ordinary stocks? Yeah. All bullshit aside. It’s a terrible stock market. That’s an awful chart, even without the monster.

Buybacks Bite

The fundamentals are just as bad. I’ve been doing some work on buybacks. To bring you up to speed; companies have borrowing a lot of money to buy back shares. Corporations aren’t stockpiling cash, at least not in the US. They’ve levered up to inflate short term EPS. Leverage taken on to do buybacks is about to be a Big Freaking Deal. Other folks have noticed this (a couple in the comment section). It’s very bad.

Buybacks are this era’s Greenmail. Just a different way for activists to generate short term performance. They work in up cycles. As long-term plans buybacks are a short-sighted, indefensibly cynical allocation of capital to appease hedge funds. Since this opinion runs contrary to the Word of Saint Buffett of Omaha I’ve taken endless abuse for mocking buybacks of the last few years.

I’m about to be right in a huge way. Which sort of sucks.

Ive been looking at these things all weekend. I’ll use Macy’s as an example but they’re far from alone

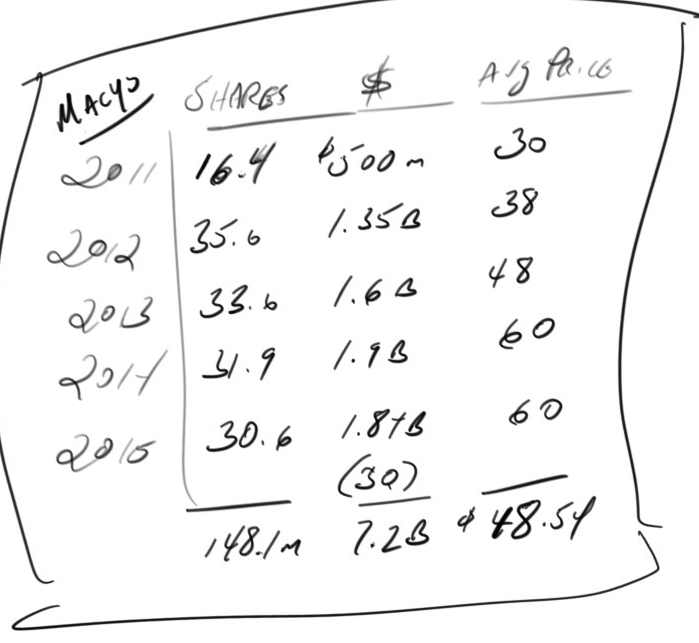

Here’s what Macy’s has done in buybacks since 2011:

Forgive my handwriting. It’s a little sloppy. I’ve been looking at this stuff since 2am.

The scribbling says Macy’s spent $7.2b buying 148.1 million shares at an average of $48.54 from 2011 through last October 15. The stock is down 50% in 6 months, well below $40.

Some very basic accounting: Repurchased shares aren’t “bought and held”. They are retired to reduce the share count. Effectively the shares, and money spent on them are just lit on fire.

Because all repurchased shares go to zero (with the weird approval of investors) it technically doesn’t matter that Macy’s would be down $1.6b on its Macy’s position of repurchased shares. Again, if they had any value at all. That’s a loss of 22% against a 45% gain in the S&P500. Buybacks are tantamount to a group of executives running a hedge fund that buys only one stock, on which it has limitless inside information and Macy’s lost 22%.

The simple numerical fact of this makes the idea that buybacks “are an expression of confidence” laughably obtuse. When a buddy brags about his kid being a great athlete do you take him at face value? Of course not. CEOs always like their chances. That’s what makes them good CEOs. It also makes them shitty stock pickers.

Like most companies Macy’s always thinks its own stock is a buy. In the short term, buybacks boost earnings per share, often triggering CEO bonuses and delighting activists! For a while

It’s a predictable sequence

For a while EPS looks awesome because of the share reduction but net income lags. The whole time enterprise value is erodes. Long-term investors get a bigger chunk of a lesser business and no cash at all. Then the earnings (orange line) rolls over and takes the stock with it:

Oh yeah. “Money is returned to shareholders!”

(Dispense with this quickly: When Wall Street tells you it’s giving you cash and you don’t see any money in your hand you’ve been had.)

Debt is a cruel mistress.

Retail is an insanely low margin business that requires constant investment. Macy’s has a 4.9% net margin. So when Macy’s borrows $500,000,000 at 3.7% to buy back stock it sounds cheap but it’s just about the company’s entire margin on $500,000,000 in sales in a growing economy.

Bookie or banker, loan givers don’t care about your personal problems. “No winter so coats didn’t sell? Screw you, give me my money. Bought your own shares at $50 and now you don’t have the shares or the cash? TS, give me my money.”

Now business has turned down, stores haven’t gotten any attention. Activists are prodding mercilessly. Macy’s is sitting on billions of dollars in winter coats in some sort of monumental inventory screw up that we’ll never know the full story on. Seriously, they could do hands across America tying coat sleeves together. It’s insane.

Oh yeah, Macy’s is on credit watch.

So earnings, both on a net and per share basis are going to end up much, much lower than expected. Shareholders have no cash. Macy’s has no cash. They just have 80% of the world’s down and impatient bankers.

The activists have the cash. Because they sold their shares to Macy’s and the rest of the muppets.

Macy’s and its shareholders have been conned. Everyone buying into buybacks has been. Corporate America borrowed cheap and bought itself. According to FactSet as of Q3 180 S&P500 companies have spent more on buybacks than they’ve earned in the last 12 months.

It’s not a story across the whole market yet. It will be.

The analyst blamed weak sales. That’s the nicest possible take.

Macy’s liquidity problems are the result of years of systemic, moronic capital allocation. The company was an accident waiting to happen. As it turns out, that accident was the weather.

As of the end of last October Macy’s had repurchased $1.84 billion of its own shares at an average cost of $60.13. In part to help fund these buybacks Macy’s issued $500 million in debt last December. At 3.45% interest Macy’s figured it was a no-lose opportunity.

Macy’s was wrong. Shares are in the mid-$30s and the company still has to pay the juice on the debt. The bet big and wrong. In a low-margin business that’s very bad.

Macy’s is down a paper loss of about $700 million on the shares it retired. Earnings per share fell anyway. The fact that it would have been worse without the buyback isn’t really any consolation. Macy’s has guided lower twice for Q4. It now expects to make $2.18 to $2.23 compared to $2.44 last year.

The smart play for Macy’s would have been buying puts instead of all that stock and those winter jackets.

Macy’s is just begging for an activist to come in and beat some sense into the place. At best department stores have a 5-10% margin. Macy’s is much worse than that. The stock is down 50% in 6 months. That could look like a bargain a year from now.

Same Store Sales

Gap hates shareholders. That’s the only explanation for why they still release same store sales.

Gap stock was up big all day and crashed after-hours.