“It is finally happening in full view, in unmistakable manner, in a way that the awake, the aware, and the conscious can perceive in alarming stunning terms. The central force of Europe, the industrial juggernaut, the stable core, has begun to pivot East. The Germans have had enough, fed up with destructive US activities of all kinds. For the last few months, they have been laying out their indictment, their justification, their reasons to abandon the corrupt US-UK crowd. The bank wreckage, the market rigging, the endless wars, the sanctions which backfire, the sham monetary policy, the economic sabotage, the spying, the gold gimmicks, it has finally reached a critical level.

Germany has begun to move East in full view. Only the deaf dumb and blind cannot notice, and they will probably never notice. They are fodder. The awaited signals seen by the Jackass have finally arrived. The grand stage leans East for the European players, with steps taken to the right, the weight having shifted, the messages suddenly more angry, more filled with disgust, more loaded with open confrontation. The commercial forces aligned with Russia are coming to the fore. The departure after a recent re-election by Chancellor Merkel should serve as the final slam of the hammer. She stood in the wrong camp, the banker and politician camp. They do not run Germany.

The marriage is over, the glow gone, the lawyers in the room, the bitterness in the open. Those exciting Saturday nights with the Germans and French enjoying a good ride with Mustang Sally are over. The once vivacious peppery exhilarating relationship with steamy back room sessions has turned ugly, old, nasty. She has lost her appeal, and worse, has turned vicious and destructive. Sally has stolen the jewelry, wrecked the credit lines, undermined the day job, and backstabbed the neighbors. As time passes, more joint accounts are seen as drained. Sally must go. The once thrilling tosses replete with the excitement of a bucking mare have turned into a kick to the head, a broken bed, as the acidic Buck has fallen from grace and burns holes everywhere. The lascivious flow has turned blood red, hardly a monthly matter. The only thing holding the relationship and tight liaison together is the heavy narcotics flow through NATO bases and major European banks. Regardless, Sally must go. Her devious devices, tools, ploys, nasty friends, and antics threaten to wreck the European industry supply lines and heated homes. The nation’s accounts are depleted. Sally must go. Her ride is more like a kicking old hag with warts where a sexy smile once resided. Her trust is nowhere. She is wrecking the European house. Sally must go. When Germany turns away from Sally, and shows her the door, it will be clear in the global country club that Sally is gone. Then eastern winds will blow some fresh air on the putrid parlors.

The marriage is over, the glow gone, the lawyers in the room, the bitterness in the open. Those exciting Saturday nights with the Germans and French enjoying a good ride with Mustang Sally are over. The once vivacious peppery exhilarating relationship with steamy back room sessions has turned ugly, old, nasty. She has lost her appeal, and worse, has turned vicious and destructive. Sally has stolen the jewelry, wrecked the credit lines, undermined the day job, and backstabbed the neighbors. As time passes, more joint accounts are seen as drained. Sally must go. The once thrilling tosses replete with the excitement of a bucking mare have turned into a kick to the head, a broken bed, as the acidic Buck has fallen from grace and burns holes everywhere. The lascivious flow has turned blood red, hardly a monthly matter. The only thing holding the relationship and tight liaison together is the heavy narcotics flow through NATO bases and major European banks. Regardless, Sally must go. Her devious devices, tools, ploys, nasty friends, and antics threaten to wreck the European industry supply lines and heated homes. The nation’s accounts are depleted. Sally must go. Her ride is more like a kicking old hag with warts where a sexy smile once resided. Her trust is nowhere. She is wrecking the European house. Sally must go. When Germany turns away from Sally, and shows her the door, it will be clear in the global country club that Sally is gone. Then eastern winds will blow some fresh air on the putrid parlors.

BERLIN INDICTMENT CHARGES

Berlin is outraged by clear USGovt spying, and in process of conducting a Gold audit among their population. Germany is building motives to split from the Euro Monetary Union (common Euro currency) by forging stronger open ties with Russia & China. The justification is becoming plainly laid out, in four perceived indictment charges. The Jackass believes Germany will break from US/UK and its USDollar fiat currency regime over four primary thorny issues. The four are major indictments, all extremely serious, all indicative of a decayed system and morally bankrupt leadership. The charges are coming into view, highlighting fundamental commercial, philosophical, and ethical conflicts that distinguish the two nations (considering US/UK a single entity). The issues center on the following key differences:

- Good relations with Russia and continued energy supply from Gazprom

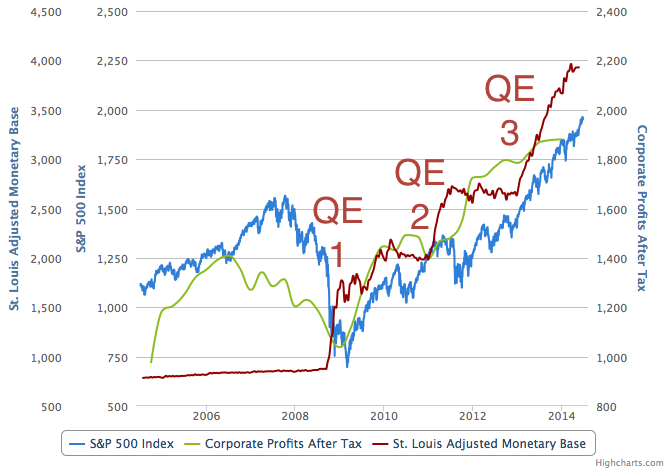

- Displeasure over planned Draghi Euro Central Bank bond monetization

- Disgust over NSA espionage by USGovt, with benefit for US corporations

- Damage to German population from gold price suppression.

The damage began with the refusal to repatriation German official gold by the New York Fed. The damage ends with the USGovt NSA espionage. Germany is very angry, sufficiently motivated to part ways with the US/Anglo camp. The plan to make distance from the British & Americans appears to be well along in execution. The critical stake in the ground was the prosecution, investigation, and forced actions during the Deutsche Bank actions. The trained eye and informed view notices the intense activity for the last two years, as closing all the back doors from the gold halls. Some major eruptions can no longer be brushed aside as simple anomalies. The boils, open sores, and deep rashes are visible everywhere. The London Fix is being abandoned, Deutsche Bank forfeiting its seat, regulatory bodies in the deeply corrupted London Centre concluding nothing askew and all is well. The LIBOR scandal has some German ignition points, with no prosecutions anywhere in sight. The FOREX and Gold derivatives are under intense scrutiny, again with a German hand to unwind the corrupted arenas, with massive naked short raids continuing in the last two weeks.

EXIT USDOLLAR, ENTER GOLD STANDARD

The plan seem obvious for Germany, to exit the USDollar, but first to embrace the Euro as a caretaker currency platform before the Eurasian Trade Zone comes together and offers a gold-backed continental currency with broad shoulders. All of Europe will rally around the Euro flagpole, hunker down during the other financial HAARP-like storm (bearing Weimar nameplate), and ride the storm until the Russian-Chinese hard asset currency arrives. The BRICS have invaded the mainstream Western stage and hold a banner for all to see. The stage has been altered, its weight shifted, leaning to the East. Tremendously important historical events are occurring. The King Dollar is wounded mortally, having fallen off the throne, looking weakened, haggard, and ashen. Sympathy for the US-UK corrupt violent vindictive crew has vanished. Next comes the assaults on the European Commission, that corrupt den.

The path to the Gold Trade Standard is becoming visible, the key break being the divorce between Germany and the US/UK fascists. It complements the divorce between the US and Saudis which has occurred since March. That break has been detailed in public Jackass essays. The German break is the new event, with current episodes absolutely mesmerizing for their importance and shock. Some US press sources are awakening. The United States Govt has treated France and Germany like adversaries, even enemy camps. The BNP Paribas case was atrocious for its devious ploys, giving old line Europeans a kick to the head. The US rats have infiltrated with organized networks of espionage agents. The press prefers to describe them as merely eavesdropping. In reality they are gathering information on Germany strategic planning, on Germany corporate contracts in development, and on German political functions. The consequence is a coordinated indictment taking shape which will result in the final steps coming to pass in the Global Paradigm Shift. The USDollar will be chucked into the dustbin of history, but first, it will be kicked to the used car scrap heap where it awaits finally processing. That processing consists of the conversion of USTreasury Bonds into Gold bullion on a massive scale at numerous offices. The BRICS Banks are ready to do business. They are two, the Development Bank and the Contingency Reserve Arrangement (CRA). In time the CRA will be known as the New IMF for its function, while the Development Bank will be known as the Central Bank housing gold.

ESPIONAGE AGAINST ALLY

The attention has gone from Sally to Ally, the relation turned quietly hostile. Not the queer conversion of GMAC into an empty bag lending institution, but rather the key Central European Ally in NATO. In the past Hat Trick Letter essays, items #1 and #2 have been addressed, focus having been on the deteriorated Ukraine situation and the antagonistic Bundesbank position. The US fictional output from destructive fracking and deceptive shale projects has been pledged to Europe, in a massive ruse that is vacant on its face. Huge 95% writedowns of shale oil reserves like by Monterey in California, combined with departures of fracking firms like Medallion in Western Pennsylvania, testify to the fact that the USGovt strategy is a ruse with empty tube. The German central bank has challenged the Draghi EuroCB not to embark on destructive unsterilized bond monetization. In the past, the EuroCB policy disagreements on phony bond patches and bond monetization have been the source of great conflict, even with German high court rulings against the EuroCB. The LTRO (Long Term Refinancing Operation) is but another device from the same Weimar laboratory, a mere banker con game with super seniority rights to favor the elite investors.

In extreme focus in the past month is item #3, the nefarious NSA espionage. Those who call it eavesdropping miss the point. It is not about catching juicy information on politician affairs. It is not to grab a lead on Merkel’s next luncheon for tabloid display. It is to seize information on Russian and Chinese developments and plans, on the commercial front and financial sector respectively. It is to infiltrate the German computer systems and communication systems, probably to plant Trojan Horses for later leverage in blackmail at the state level. The Berlin officials are well aware. The entire NSA espionage chapter appears to be exploding on the scene. In fact, word has come that Russian Intelligence offices tipped off the Berlin officials about the USGovt NSA activity before arrests were made last week. The Snowden files are being used in important ways. The Central European source stated briefly, “The comical part in all this is that Russian intelligence FSB and GRU tipped the German authorities off by providing the leads.” The Germans followed up quickly, so quickly that a divorce is the conclusion. In the meantime, the German-Russian cooperation with trust develops while the German-Anglo trust withers away. The break between the Germans and the Fascists from US-UK-EU may be closer than ever, as history is turned on its head since World War II. The entrenched Fascists on the global financial war front are the Americans and British accomplices, the big corrupt banks being the pillboxes. They will be abandoned, or toppled. At risk is the NATO Alliance. If and when Germany pivots fully eastward, the NATO membership will be rendered empty chair with a speaker phone attached.

GOLD ROOM CRIME….”

Full article

Comments »