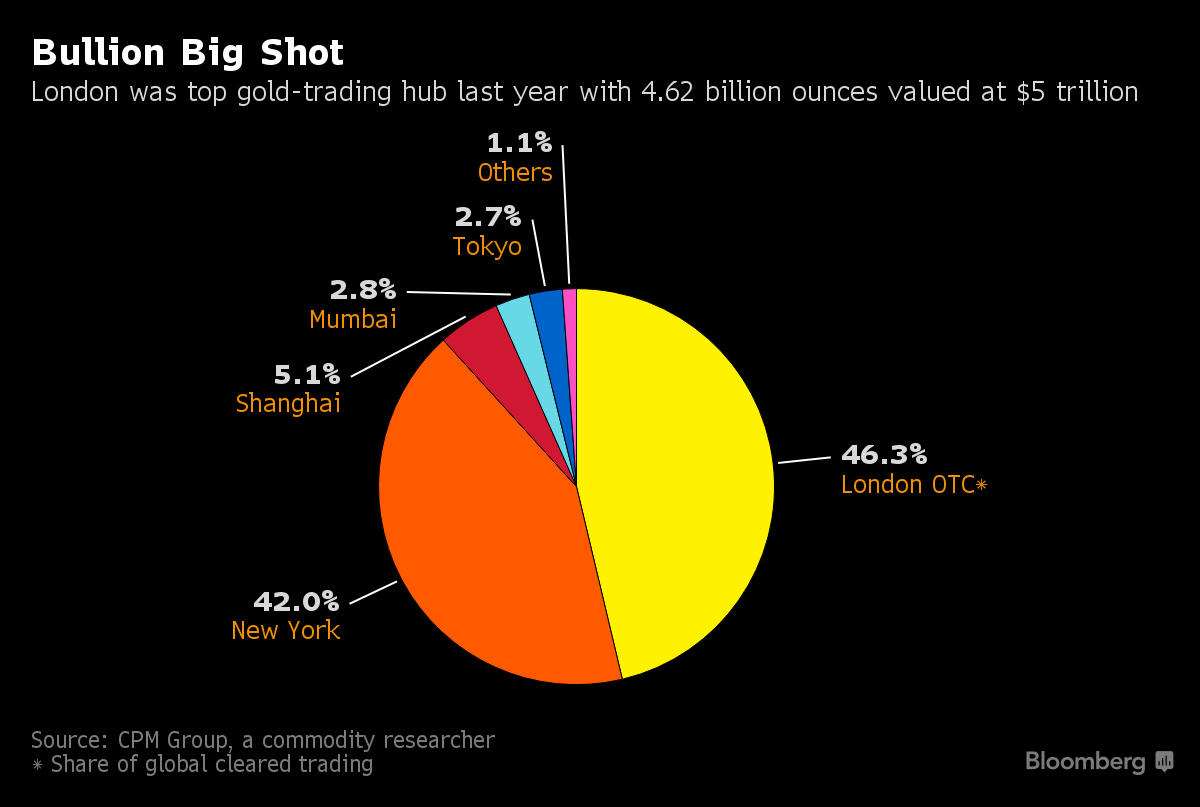

The $5 trillion gold market has, yet again, become a head scratcher for market participants.

Bears, esp. on technicals grounds, call for further downside. There are two distinct scenarios which have yet to play out fully. The move in gold over the 9/11 – 12/15 could be a correction in a dominant bull market (my current positioning/thinking). Alternatively, the 12/15 – 9/16 gold rally could be a correction in a dominant bear market.

Bulls point to supply/demand fundamentals and likely ongoing support from global central bank shenanigans. The current geopolitical environment is what one would call supportive of higher prices. Think USA/Russia Cold War 2.0., N. Korea (nukes), the South China Sea (China, or “Jhina” as Trump appears to pronounce it) and Mosul, Iraq (ISIS).

Bitcoin has been quietly rallying and currently trades above $635. The best explanation I have heard thus far for the phenomenon of bitcoin is that it is a solution looking for a problem. Gold has been singled out as nature’s bitcoin. The forthcoming bitcoin ETF (Q1 2017 approval?) from the twins; Winklevoss Bitcoin Trust, ticker COIN has been touted as a reason for a skyward trajectory in the leading cryposcrip going forward. Truth really is stranger than fiction. I would fade that move, although the underlying blockchain technology clearly has merit. The recently approved IEX exchange (The Investors’ Exchange) will be utilizing blockchain technology with partner/spin-out TradeWind to roll out a safer, more transparent gold trading alternative. I for one would prefer to trade gold on Katsuyama-san’s portal and give fictional Satoshi Nakamoto-san’s fraud fraught bitcoin rabbit hole a wide berth.

The LBMA gold conference here in Singapore kicked off Monday. It appears ICE got the jump on LBMA for a gold future to help clear the London daily auction (central clearing via ICE). If the fixed income derivative market is any guide, 1st mover advantage is important and to the victor go the spoils. Watch this space.

I have written a couple of posts on the gold market in 2016 and way to play it. January 10th would certainly have had you in early on the 2016 move, but as if often the case, gold equities are not for the faint of heart. Most names are 20% off their 2016 high print.

http://ibankcoin.com/firehorsecaper/2016/01/10/gold-get-some/

PRETIUM RESOURCES:

This follow up post will be on Pretium Resources, PVG on the NYSE the TSX in Canadian Dollars. PVG closed up 6.21% on 10/18/16 to close at C$12.83 in CAD. PVG in the US closed up 6.41% to US$9.80. Market cap US$1.8bln.

2016 YTD performance; PVG +94% (21% off YTD high of $12.41), GDX +76%, GDXJ 111%.

Latest Pretium investor presentation (required reading):

http://s1.q4cdn.com/222336918/files/doc_presentations/2016/denver-gold-forum-2016.pdf

Pretium is a Canada-based (British Columbia) development stage gold mining company, slated to move to production by mid-2017 of their 100% owned Brucejack project in Northern B.C.. Brucejack’s Valley of the Kings (VOK 6.6mm) and the nearby West Zone (0.6mm) have proven and probable reserves of 7.5mm /oz. of gold. An 18 year mine life is assumed. All-in sustained cost (AISC) per ounce of gold is US$446 (several majors are > $1,200 as a comp). Target production is just over 500,000 oz. per annum. The project IRR with gold at $1,250 exceeds 35%. The project also contains a lot of silver, the bulk, 26mm oz. P&P, at the West Zone with an additional 4.6mm oz. of silver from VOK.

What makes the Brucejack site and hence Pretium so compelling?

High grade deposit. Gold at 14.1 g/t. It is not an exaggeration to say that Brucejack is one of the highest grade gold discoveries of the last 1/2 century. This is both good and bad in that high grade deposits tend to be uneven. Grade varies considerable overly the broader deposit. The road to 7mm ounces P&P has at times been harrowing for investors. A relatively large scale 10,000 ton bulk sampling conducted by Snowden Mineral Services in 2013 netted 4,215 ounces of gold (versus 4,000 oz. expected). Strathcona at one juncture in October 2013 burst Pretium’s balloon, sending the stock down nearly 30% to sub C$3.00 by stating, “There are no valid gold mineral resources for the Valley of the Kings zone, and without mineral resources there can be no mineral reserves, and without mineral reserves there can be no basis for a Feasibility Study.” Snowden Mining Industry Consultants took over the study from Strathcona at the direction of Pretium management, employing Pretium’s preferred bulk sample method (i.e. run the full sample through the mill and see what comes out, hard to argue with as it is difficult to cherry pick a 10,000 tonne sample). Pretium have reported some intersections grading as high a 1,000 grams of gold per metric tonne. Impressive indeed.

As an aside, Strathcona have retained a very strong reputation in their field. Their report on the now famous Bre-X scam in May 1997 laid bare the record setting fraud that had been perpetrated on global investors. At its peak, Bre-X had a $6bln market cap.

http://www.wsj.com/articles/SB86279977155130500

A full quarter before the definitive Strathcona report the stock fell from C$20 to the mid $2’s when the proposed 15% partner Freeport McMoRan Inc. (FCX) found scant amounts of gold from their independent testing of samples drawn by drilling parallel to Bre-X’s. I was a buyer for size, not believing that a scam of this magnitude could be possible. The meticulous detail required to salt over 3km of core samples over an extended period and have them tell an intelligible story seemed to me a stretch. The report was to come out on a Friday and the stock had levitated modestly to a 3 handle. “Dr. No”, as Strathcona’s Farquarhson was known, put a scare into me given the highly spec nature of my stock wager with that days horoscope putting me over the edge. I sold 10,000 of my 12,000 shares and saw them open the following Monday (post report – no gold) at 8 cents. I had clearly dodged a bullet and did what any 30 yr old punter in the same situation would do. Hanging my hat in Japan at the time, I walked into a Harley Davidson dealership and pointed to the two-tone silver/black 1997 Softail Custom. ¥2.1mm changed hands and I kindly asked the proprietor to point me the direction of central Tokyo as the 2-wheeled beast sprung from the captivity of the showroom.

Managements’ vision/acumen. Robert Quartermain is Pretium’s Founder, CEO and also acts as Chairman. Quartermain’s history with the Brucejack site is very interesting in and of itself. While at Silver Standard, where he spent 25 years of is 40 year mining career, the Snowfield/Brucejack assets were purchased for $3mm (5 cents per ounce of silver in the ground). Pretium’s IPO at C$6 raising $283mm in 2010 provided the capital to allow the company to purchase the assets for $450mm and Pretium’s market cap now stands at $1.8bln. At 0.63% of NAV and commercial production less than a year away, I do not think the story has fully played out yet.

Operations; permits / funding / construction. Permitting is a huge issue in all jurisdictions. The delays can be staggering. A decade ago a time frame of 3-5 years would be typical for the requisite environmental assessments and permits. Today estimates would be 7-10 (The Canadian government recently approved the BC domiciled Pacific Northwest LNG project with 190 conditions, mercy me).

The full project cost (through production in mid 2017) of US$686mm has now been fully funded, $540mm financing package (largely debt) and $146mm via equity. The amount of support infrastructure required for such a remote location is daunting and all observers have been impressed by the progress Pretium has made to date. To put this capital budget in context, Toronto is spending C$3bln ($2.3bln) for 1 (one) subway stop in Scarborough (Manhattan’s Second Ave. line will have a comparable cost at $2.23bln/mile, but at least it has 3 stops!).

Top Shareholders (%): Van Eck Associates 9.97 Silver Standard Resources 9.50, Zijin Mining 5.04, Black Rock Asset Management 4.97, Orion Mine Finance 2.57, Pretivm Management 2.00 (41% institutional ownership). Franco Nevada Corporation have purchased a modest royalty interest in the Brucejack project.

Given the site is open in all directions there certainly exists the possibility of an increase in the reserve numbers over time. Most see the likely catalyst as being M&A related as the majors are keen to fill gaps in their production profile and average down their ASIC in low risk jurisdictions. Post permitting, Canada certainly fits the bill.

Analysts are bullish on the Pretium story, with targets as high as C$20 one year out (vs. C$12.83 spot, +55%). I think it could eclipse the all time high of $18.24 and reach $20 which would be good for a double from spot $9.80. It certainly will not get there is a straight line, but hopefully it will be devoid of the high wire peril evident in 2013. The story has been effectively de-risked, as much as a small cap gold mining stock can be.

Hopefully the toys will be funded is a more traditional fashion this time around. Street bikes are now off limits (wifey), but maybe a Nissan GT-R?

JCG

Follow me on twitter @firehorsecaper

Disclosure: Long 1/4 portion PVG in Canadian dollars, usually hold in USD as well. High beta gold play.

Note: Gold – a good delivery bar (think central banks and bullion banks) contains 400 troy ounces (12.4kg. or 438.9oz). A kilobar (preferred in Asia and with individual investors) weighs 1000 grams and contains 32.15 troy ounces. An ounce of gold contains 31.1 grams.

Comments »