Beginning in around 2002/3 the energy/commodity complex began a magnificent rise as the sleeping Chinese dragon began to awake from its slumber ahead of the Beijing Olympics. The effects were widespread, even in locations that had zero exposure to China, investing capital began to flow into these sectors. The narrative of the Commodity Super Cycle began to play out and the bobble-heads on financial media all had hard-on’s for any natural resource plays which were going to supply the raw materials for China’s growth. Commodities, once viewed as speculation only, became the new asset class of choice and the ETF industry eventually took full advantage.

I was in the mining consulting industry during most of these commodity bull years and companies were spending a lot of money. We were hiring like crazy and there wasn’t enough talent around to finish all of the projects we had. Production companies were investing in land, transportation infrastructure, exploration, permitting, and equipment. Rising commodity prices now meant that resources/reserves that were once thought to be economically unfeasible were now “in the money”, so to speak. Times were good, but it was the classical example of strong demand (and higher prices) leading to over-investment, leading to low oversupply (and lower prices) leading to weak demand. You don’t need a Harvard Business School degree to recognize what’s happened:

The Boom is now a Bust.

The problem now is figuring out where we are in the cycle. I think much of the bust has already taken place in regards to commodity prices however, they are mean reverting instruments and will probably overshoot to the downside just like they did on the upside – so stay clear of them in my opinion. Furthermore, the Fed’s monetary tightening narrative should lead to more commodity downside; read my last article for details: http://ibankcoin.com/dyer440/2015/11/06/fed-trade-school/

Think back to what the world was like in 2002/3, think about the size of the businesses in many of these sectors: energy, mining, chemicals, transportation, etc. These sectors are going back to at least 2002/3 levels. Just like the consulting company I used to work for, they will have to shrink.

The interesting thing to note is that all these companies are managed by HBS type personalities, and the hubris at the top is simply incredible. They should all be scrambling to save their companies but instead they’re missing the writing on the wall – this is especially true in the Oil & Gas industry. Managers typically have a hard time acting like traders; when we realize a mistake – we get out and cut our losses (at least we should) . We shouldn’t sit around with our fingers crossed hoping for a rebound.

So Here’s the Trade:

I looked for a company with the following attributes:

- Overpriced relative to P/E

- Large Cap

- Tradeable, liquid options

- Large Dividend

- Still has enough meat on the bones to short

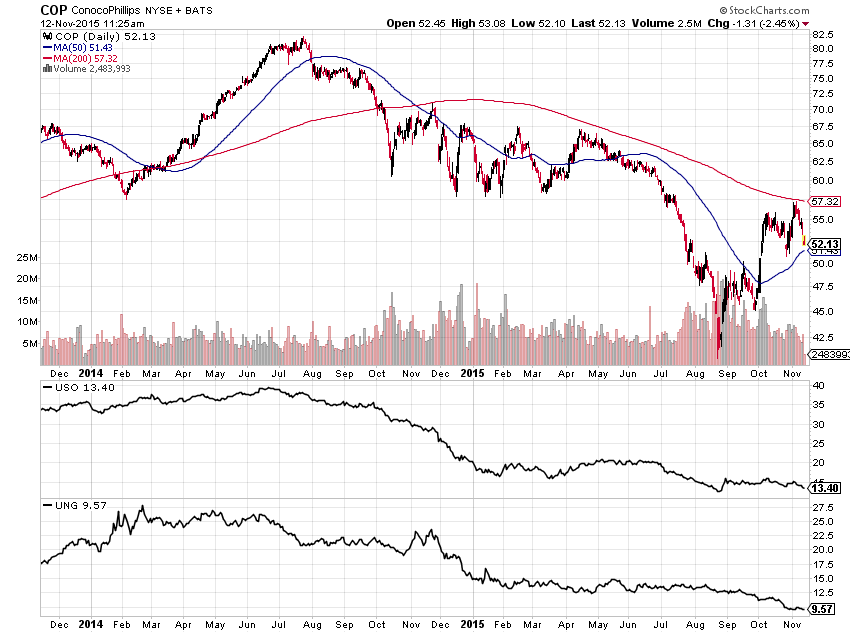

The winner is ConocoPhillips (COP). COP has a forward earnings P/E of around 85, and they are attempting to defend their dividend which is around 7%. The bullish thesis on COP is “collect 7% while you wait for oil to rebound”. That is insane. Last quarter COP generated $1.93 billion in operating cash flow, but spent $2.17 billion in CAPEX and another $920 million on dividends.

The bottom line is they will have to cut their dividend distribution. That, combined with the commodity price exposure and you have the recipe for a fine-looking short trade. Use the recent high’s ($57-ish) as a stop loss , and the recent lows ($42-ish) as a price target.

Refer to the COP chart below:

Comments »