The narrative of SIVB has been a FAG-bank in Silicon Valley that drains its region of money and then takes said monies to invest in start ups. After said start-ups grow up to become idiotic unicorns, they cash in and make their share price shoot the fuck higher.

This is their business model — attempt to prove me wrong.

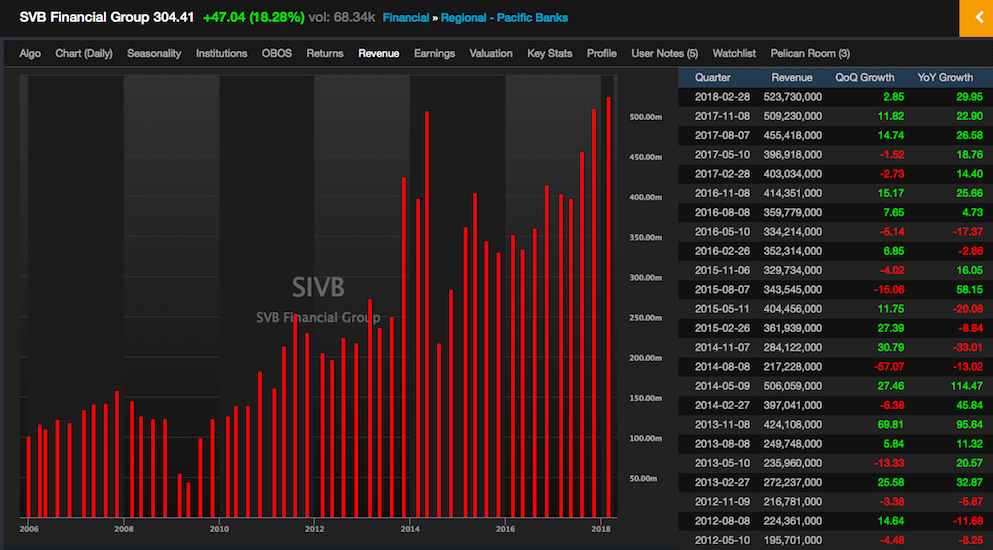

For a bank, the valuation is beyond comical. Anyone who knows the first thing about bank valuations knows that to trade over 3x book is folly. Yet, here we are shilling for SIVB above 3x book and a staggering 7x sales.

Granted, revenues are increasing at an abnormal rate — but that’s only because of the tech boom in the valley. Once that ends, so will the good times at SIVB.

Out of all of the stocks in finance with market caps above $10 billion, SIVB ranks near the very top. Note, it is the only actual bank on the list.

The only other bank in America trading at such a high valuation is FFIN. I have no idea what these losers do, only that it trades 3.5x book and 10x sales.

So is this the mother of all shorts?

I know some folks over there. Look into the spreads on credit lines to start ups. I think they average like L + 800.

Most important point is they are treated differently than other lenders by the regulators. When a normal bank lends money to a money losing enterprise it is “financing losses” and get to take a nice charge off. When SVB lends to a money losing company, it’s “managed cash burn” and gets to accrue their L + 800.

So that’s bullish as shit, correct? Mind you, I am moosh brained.

No idea if it’s a short or not. I am just pointing out a wide difference in SIVB compared to peers.

Can we look forward to updated chats?

A one stop analysis?

Fly?

Just acknowledge me .

Jeezuss Fly, tell this fucker he’s a special boy so he’ll STFU.