Well I said this was a zero or 10x. Right now it’s looking like the former.

This is a kitchen sink financing, a solid 40% below yesterday’s closing price and well below the 20 day average price. They’re raising $60m to stem the burn and they simply do not care about the stock price right now.

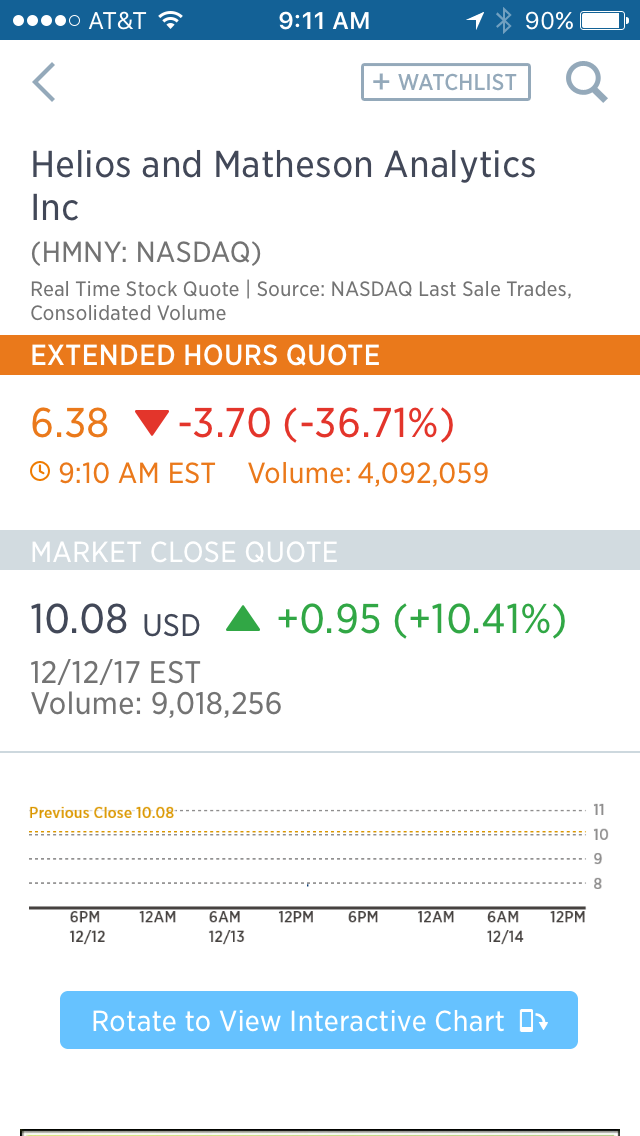

Shares are off by 35%.

Helios & Matheson prices 8,261,539 units (w/ each unit consisting of one common stock, one Series A warrant, and series B warrants) at $6.50/unit

Co announced the pricing of a best efforts underwritten public offering of an aggregate of 8,261,539 Series A units, with each Series A Unit consisting of (i) one share of the Company’s common stock, par value $0.01 per share, and (ii) one Series A Warrant to purchase one share of Common Stock; and (B) 969,230 Series B units , with each Series B Unit consisting of (i) one pre-funded Series B Warrant to purchase one share of Common Stock and (ii) one Series A Warrant, with anticipated gross proceeds of ~$60 mln, before deducting underwriting discounts and commissions and estimated offering expenses payable by HMNY

I’m HODLing this one.

If you enjoy the content at iBankCoin, please follow us on Twitter

put in your UVXY pile of shit

What’s with so much hate early in the trading day?

Does anyone know why we are up so much yet again in the DOW? The chances of tax reform and other shit passing got smaller with the ousting of a Senate seat. I am struggling to find yet another reason we are higher again. What did I miss?

That stuff doesn’t matter in a bull market. Tax reform could fail and the DOW will still rise 10-20% next year.

A secondary? The hell. Didn’t see that coming. (extra Sassy)

Based off Stocktwits it looks like there are a lot of retail bagholders in this one.

There were at least three red flags on this. Can you name any of them?

OK, if you don’t know any of them, try this: why did I buy this and what did I get wrong?

I think buybacks an stock offerings ar both massively misunderstood, as in, not all buybacks are good, and not all offerings are bad. The only thing that the retail investor – and often the analysts – considers is effect on shares outstanding. What is ignored is the massive exchange of cash.

For example, let’s say a stock has a market cap of around $100M, Cash on ahnd of around $2M, and Net Tangible Assets of around -35M. In that case, an extra $53M could be beneficial, no?

Not if the stock offering is 35 percent below current market price

LOL

I guess I was using this to make a more general point. For example, when shares are offered or purcahsed at the current stock price.

HMNY was always overpriced. On the positive side, at least the price should stabilize and maybe this will save retail investors from getting fleeced on this stock in the future.

Let me put it another way: if the stock offering was suddenly canceled, would that increase or decrease the current price and value of the stock, in your opinion.