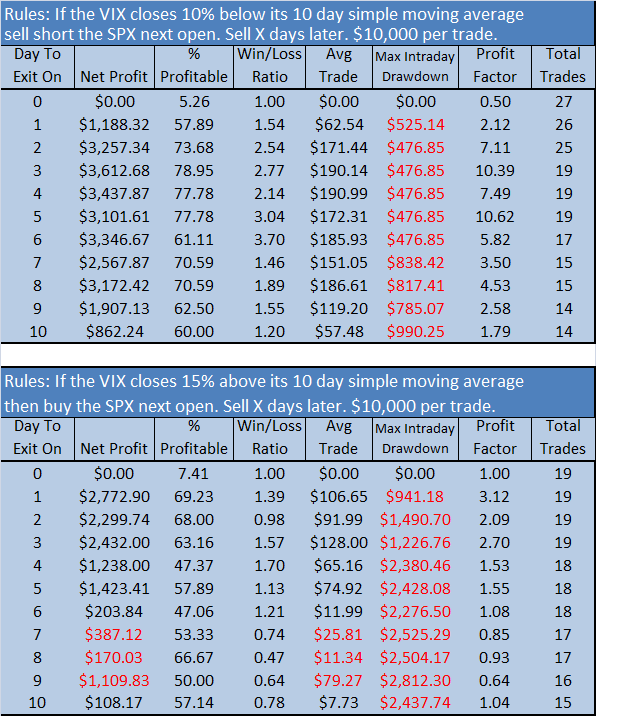

When deciding how much to lose on a trade, or where to place a stop, traders use a variety of position-sizing methods to arrive at a position that works for their style and risk profile. One method I do not like is when traders allow the amount of capital lost to determine where the stop is placed. Below is how traders typically set up that type of position:

100K to invest. Put roughly 10% into each 10 different stocks, ETFs, etc. For each 10K position, the trader now decides he does not want to lose more than 1K, so he sets his stop at 10% beneath entry.

The problem with this method is that some trading vehicles are inherently more volatile than others. A 10K position with a 10% stop in an extremely volatile ETF (the double inverse financials SKF) will consistently rob the account of 1K when the stop is hit.

The extreme volatility should not come as a surprise; remember the leveraged ETFs are designed to move twice the DAILY return of the underlying. As volatility and leverage build on themselves, the multi-week or multi-month returns of these leveraged ETFs can be many times more or less than the return of the underlying.

But we must get back to our trader with 10% allocated to 10 trading vehicles, each with a 10% stop.

Why a 10% stop? Again, we are creatures of habit, and we like round numbers. It may be that many breakout traders use an 8% stop, due to the notariety an 8% stop-loss garnered in the publications of William O’Neil and Investors Business Daily. The point is the trader is still allowing the amount of capital lost to determine the stop level rather than the movement of the trading vehicle.

Since we know leveraged ETFs are at least twice as volatile as their underlying, and by extension, twice as volatile as much of the common stock constituting the index, shouldn’t any stop set for leveraged ETFs be at least TWICE the stop the trader would normally use when not trading leveraged instruments? If breakout traders allow a stock to move at least 8% before accepting the trade as a loss, traders using breakout setups on leveraged ETFs should consider allowing at least a 16% stop.

So what money managment strategies do we use to build a position around the movement of the trading vehicle rather than the loss of capital?

- First the trader must examine the volatility of the leveraged ETF. How far might it move against his account before the signal/pattern is proven to be wrong? In my personal trading of diETFs I find that 15% is about right, but for purposes of discussion and round numbers we’ll use 20% as the distance a diETF is allowed to move against us before stopping out the position.               Â

- Secondly, the trader must pre-determine what percent of his or her overall account value to risk on this trade. If meticulous records are kept, he may determine that he has a very high winning percentage, and is therefore willing to risk 3% on each trade (50K*.03 = $1,500 a trade risked). For purposes of simplicity and round numbers, we’ll use 2% as the amount of total equity risked on each trade (50K*.02 = $1,000)

Below is a spreadsheet showing recent trade sequences for two ETFs: The Proshares Ultra Long SSO (which is supposed to move twice the daily amount of the S&P 500 index) and SPY, which is the unleveraged tracking ETF for the S&P 500. Both money managment methods (position-size built on capital loss, and position-size built on movement of the trading vehicle) are represented in the sheet. The ETF is assumed to be bought on the open of 1/6.

The upper half of the sheet show the results of buying 10K worth of SSO and 10K worth of SPY, using a 10% stop (limiting capital loss to $1,000). As expected, by 1/16, SSO has lost twice as much as the SPY position, even though both positions started out at 10K. The stop in SSO was hit on the 4th day and the stop in SPY was hit on the 7th day.

The upper half shows that the leveraged ETF did nothing except double the risk for the trader.

The lower half of the sheet shows what happens when the trader builds a position based on the movement of the leveraged ETF. As these are volatile, his stop will be hit when the ETF moves 20% against him. He is still risking $1,000 per trade, as he was in the upper half trades.

He builds the position like this:

On 1/6, he uses the opening price to calculate the 20% move ( $28.46*.20 = $5.69). He then divides the amount he is willing to risk by this figure ($1,000/$5.69 = 175.74) He would then buy 175 shares (I always round down.) This results in him buying a position that is roughly half the size he would buy if he was using the other method.

On the spreadsheet above, note the figures circled in green. The lower figure is half the amount of the upper figure. Now note the figures circled in red. The lower figure is almost the same as the upper figure. In essence, money managment has captured the leverage of the ETF while keeping the risk at levels associated with trading the non-leveraged ETF.

Pay careful attention to the figures circled in blue. Note that the leveraged ETF position-sized using a capital loss method would lose over 4x more in 9 days than the non-leveraged SPY, even though both were initially risking the same amount ($1,000).

In Part 3 I’ll show a winning trade series using the two different money managment techniques and then present some closing thoughts.

Comments »

{kind=link}