The Chipotle CFO, John Hartung, is a smart man. He’s probably a great CFO and an even better merchant of Mexican styled chicken sandwiches. However, he has no idea how deep the rabbit hole goes, in regards to his brand being tarnished due to the recent spate of ecoli related illnesses, born out of his restaurants. Truth is, none of us know how Chipotle will end up, or where the stock will be in 6-12 months from now.

But this is what we do know. The stock is off by almost 50% since the outbreak occurred. Sales have plummeted to the tune of 30%, while costs have risen. The company is intent on leveraging into this maelstrom by opening up another 220 stores and also buying back $750 million worth of its stock.

For the quarter, the company lost $26 million, compared to netting $122 million the year prior.

Due to the share buybacks and operating losses, the companies cash position has dwindled to $250 million.

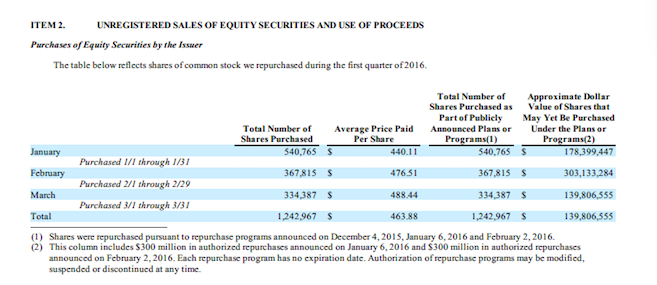

As of Q1 of 2016, the company had purchased $641 million worth of stock at an average cost of $463, for an unrealized loss of around $64 million.

Management is making a huge gamble with shareholder money, pretending they know what’s in store for the share price and gambling on whether or not another ecoli outbreak will be reported in one of their stores. Should that occur, this stock is going to get absolutely poleaxed. Why on earth is management taking on so much risk, when they themselves don’t even know the root causes of the contamination?

If they want to open another 220 stores, which will underperform by all historical CMG metrics, they should refrain from tossing money into a flaming barrel of garbage by buying back shares.

Comments »