Via ETFProphet, I bring you a link where Tom Demark is calling for a “significant top.” It seems most of the traders out there agree with Demark and are looking for a serious pullback here, with many calling for a beyond serious, slit-yer-wrist variety of pullback.

I believe those looking for a slit-yer-wrist pullback are over reacting. In fact, I’ll go on record right here and state that this pullback will be between 3-6% on the SPY, and that SPY will test the 1/18/2011 high before a deeper pullback occurs.

Before you remove all your hedges, know that I am engaging in a bit of braggadocio in order to generate some discussion on this matter.

I have tried to model the recent market action, and here is what I have come up with it.

The S&P 500 is up over +20% since August 31st, 2010. Today, the pullback on SPY was -1.0%. Thus we have 97 trading days since this move began (not counting today).

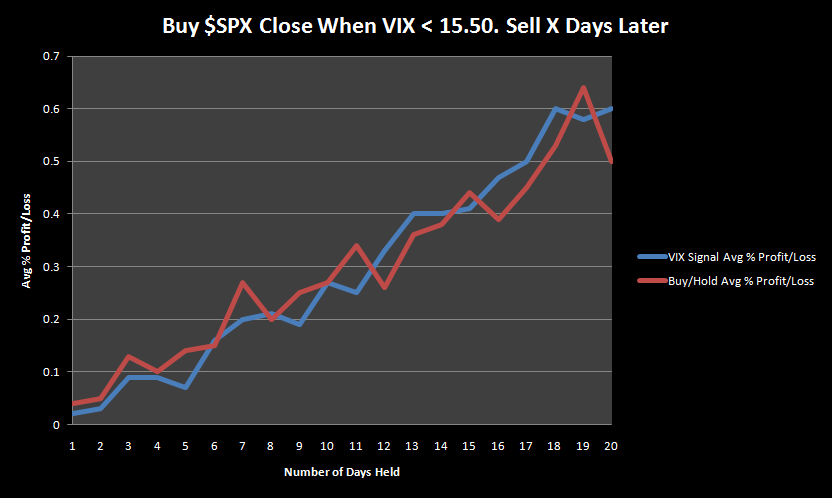

The Rules:

Buy $SPX when the 97 day Rate-of-Change > +20% AND today’s close was > -.90% beneath the previous close.

Sell X days later.

No commissions or slippage were added. I used 50 years worth of data with the first trade occurring on 10/9/1970.

The Results:

Any discussion on this type of modeling should begin with sample size. If the trade is held for the full 20 bars, there are 23 instances of this setup over the last 50 years. The statisticians would prefer 30 instances, but then that would assume that the market adheres to a standard distribution.

- The winner average profit levels out around +3%.

- The loser average loss levels out around -2%.

- Based on the % of Winners and the Max. Trade % Drawdown, most of the damage tends to peak about 1 week after the setup.

- On day 7, the % of Winners climbs above 60% and peaks at 74% on day 15.

The big takeaway here is that an object in motion (the market) tends to stay in motion (apologies to Newton). In the past, after having climbed so far, so quickly, the market’s velocity has enabled it to maintain momentum. Galileo called this inertia. The bears will likely call it “Bernankery.”

Comments »

{kind=link}