This relief rally idea is getting old. They all turn into bear traps.

Comments »Monthly Archives: October 2011

Asian Markets Trade Mixed, Europe & U.S. Futures Up on Relief Rally

Jim Cramer’s Mad Money Monologue, 10/4/11

[YouTube:http://www.youtube.com/watch?v=kMTDAc3y6Gk&feature=youtube_gdata_player 603 500]

Comments »Old Man Buffett Plays it Cool with BofA

Billionaire investor Warren Buffett is not concerned by the sharp drop in Bank of America Corp shares in the last couple of days, despite his $5 billion investment in the company last month, he told Reuters Tuesday.

“We agreed to hold it for at least five years, so what I’m thinking about is where Bank of America will be in five years, and nothing in the last 24 hours or 48 hours has changed my views on that,” the Berkshire Hathaway Inc chief executive told Reuters on the sidelines of Fortune magazine’s Most Powerful Women Summit.

Comments »Oil Futures Rise in Asian Trading

Benchmark Nymex light, sweet crude-oil futures CL1X +2.68%advanced $1.94 to $77.61 a barrel in electronic trading during Asian trading hours Wednesday, taking back some recent losses. Crude-oil supplies fell by 3.1 million barrels for the week ended Sept. 30, the American Petroleum Institute reported late Tuesday. Analysts had been expecting supplies to rise, according to Bloomberg News. Oil finished below $76 a barrel for the first time in more than a year in regular New York trading Tuesday, pressured by worries about Europe’s debt crisis and the outlook for U.S. economic growth. “Oil prices remain under the sway of macroeconomic sentiment,” noted strategists at Barclays Capital.

Comments »President Co-Caine Starting to Resonate

Herman Caine, mathematician, former Deputy Chairman of the Fed, is now a contender for President.

Comments »Today’s ETF Winners

No. Ticker % Change

1 TNA 15.27

2 DRN 12.79

3 UWM 12.68

4 SOXL 12.67

5 MATL 11.00

6 SICK 10.90

7 ERX 8.35

8 MVV 8.24

9 FAS 8.13

10 KRE 8.02

11 USD 7.87

12 URE 7.78

13 UYM 7.76

14 UYG 7.44

15 IWC 7.18

16 IJS 7.05

17 DUST 7.02

18 MWJ 6.81

19 IJR 6.72

20 TYH 6.70

21 TQQQ 6.63

22 SAA 6.48

23 XIV 6.45

24 YINN 6.40

25 IWN 6.33

Today’s Tremendously Long List of Double Digit Winners

Min mkt cap: $100 mill.

No. Ticker % Change Market Cap

1 MILL 32.42 108,010,000

2 MELA 31.10 111,910,000

3 HIL 30.63 180,150,000

4 SGK 28.19 233,120,000

5 HHGP 26.30 112,440,000

6 EPHC 24.94 296,790,000

7 SATC 24.72 113,570,000

8 FMCN 24.31 2,280,000,000

9 PNX 23.71 141,890,000

10 LXRX 23.53 310,630,000

11 WAVX 23.32 185,480,000

12 JRN 22.99 166,900,000

13 KOPN 22.65 230,650,000

14 ETM 22.32 190,860,000

15 PMFG 22.30 278,750,000

16 CVGI 21.64 182,430,000

17 STP 21.47 306,670,000

18 JKS 21.44 112,270,000

19 BLDR 21.36 120,530,000

20 SQI 20.77 267,020,000

21 AMR 20.71 992,210,000

22 WMAR 20.68 159,500,000

23 MCRI 20.35 157,830,000

24 PRO 19.55 347,180,000

25 HVT 19.41 219,270,000

26 CVO 19.34 189,700,000

27 CDZI 19.31 112,260,000

28 CSU 19.27 148,600,000

29 COHU 19.14 238,560,000

30 HDY 19.05 577,630,000

31 SRI 19.03 120,970,000

32 APOG 18.91 241,460,000

33 ATSG 18.86 247,950,000

34 CSBK 18.79 227,400,000

35 ZQK 18.70 427,160,000

36 OVTI 18.57 836,920,000

37 IBOC 18.49 887,910,000

38 SIGA 18.49 149,840,000

39 LDL 18.44 152,620,000

40 ASGN 18.37 261,850,000

41 HOME 18.27 111,390,000

42 LAD 18.04 381,290,000

43 ASIA 17.97 530,860,000

44 VRTU 17.83 309,560,000

45 DRL 17.82 138,750,000

46 FBNC 17.73 158,980,000

47 TWER 17.70 120,340,000

48 SHOR 17.66 223,680,000

49 BALT 17.65 102,900,000

50 MERU 17.61 142,610,000

No. Ticker % Change Market Cap

51 LBAI 17.52 199,390,000

52 DRRX 17.48 140,790,000

53 MOD 17.45 422,230,000

54 KMGB 17.40 135,930,000

55 WRES 17.37 150,890,000

56 TMS 17.32 285,780,000

57 NWY 17.28 194,440,000

58 OMX 17.25 417,120,000

59 RENT 17.20 129,830,000

60 RLH 17.03 122,160,000

61 AP 17.01 211,150,000

62 IRBT 16.95 675,720,000

63 MBLX 16.95 149,270,000

64 MOSY 16.92 139,330,000

65 SPAR 16.85 122,920,000

66 ALJ 16.64 342,270,000

67 WTBA 16.63 141,310,000

68 JRCC 16.58 221,040,000

69 GBX 16.56 293,090,000

70 CBM 16.41 148,330,000

71 TZOO 16.37 346,010,000

72 JMP 16.36 120,440,000

73 ZIXI 16.36 141,010,000

74 CHTP 16.32 208,420,000

75 GTAT 16.29 839,170,000

76 PROJ 16.28 366,360,000

77 CPST 16.28 259,590,000

78 DHT 16.25 131,270,000

79 NOG 16.24 1,200,000,000

80 ATMI 16.23 501,100,000

81 TISI 16.21 402,160,000

82 LTXC 16.18 238,800,000

83 CTS 16.08 279,830,000

84 KRG 16.06 232,720,000

85 URZ 15.97 105,430,000

86 CSFL 15.95 146,890,000

87 CMCO 15.91 210,140,000

88 HUSA 15.82 428,830,000

89 FRM 15.70 200,670,000

90 BUSE 15.70 376,690,000

91 OCZ 15.68 226,630,000

92 PGNX 15.63 193,480,000

93 INWK 15.60 382,070,000

94 BKYF 15.47 150,570,000

95 BKR 15.35 178,350,000

96 CIGX 15.35 272,810,000

97 HELE 15.26 776,210,000

98 STNG 15.26 158,370,000

99 AGYS 15.24 163,930,000

100 PCX 15.20 772,260,000

No. Ticker % Change Market Cap

101 HT 15.09 587,800,000

102 KELYA 15.05 419,700,000

103 INHX 15.02 192,340,000

104 GFF 14.87 517,680,000

105 PLXT 14.87 134,050,000

106 BPAX 14.85 222,210,000

107 FBN 14.81 114,340,000

108 SMP 14.79 276,980,000

109 HFWA 14.79 160,970,000

110 GFIG 14.78 487,580,000

111 CYTX 14.73 158,700,000

112 TNK 14.73 239,550,000

113 CLMS 14.66 201,460,000

114 YGE 14.63 452,420,000

115 ENTR 14.63 357,070,000

116 BGFV 14.59 131,850,000

117 TPLM 14.59 142,310,000

118 ASI 14.56 181,880,000

119 CDR 14.55 207,330,000

120 CIA 14.55 320,170,000

121 SAIA 14.53 166,120,000

122 SURW 14.50 138,930,000

123 MRGE 14.47 483,190,000

124 WIBC 14.46 177,510,000

125 FOLD 14.41 117,640,000

126 FXEN 14.40 216,660,000

127 WNC 14.32 301,480,000

128 SMBL 14.26 330,650,000

129 KAI 14.25 219,280,000

130 CAS 14.22 252,040,000

131 UBSH 14.19 264,380,000

132 GLDD 14.18 239,780,000

133 BFIN 14.13 130,890,000

134 VICR 14.13 340,320,000

135 ROCK 14.06 247,170,000

136 LUB 14.06 115,370,000

137 SSYS 14.00 380,900,000

138 BNCL 13.99 574,340,000

139 DW 13.94 441,300,000

140 CDI 13.91 204,710,000

141 ACPW 13.91 103,390,000

142 MGI 13.88 928,800,000

143 KWR 13.87 332,370,000

144 SAH 13.85 572,230,000

145 VVTV 13.81 114,380,000

146 CCNE 13.80 149,270,000

147 AFAM 13.77 155,570,000

148 MLHR 13.75 1,040,000,000

149 CFNL 13.73 249,390,000

150 FCBC 13.71 169,850,000

No. Ticker % Change Market Cap

151 PLFE 13.69 218,260,000

152 RLJ 13.67 1,250,000,000

153 HNI 13.64 856,640,000

154 CPF 13.64 430,740,000

155 IO 13.63 733,800,000

156 TESO 13.62 392,670,000

157 CHFC 13.61 420,350,000

158 ESIO 13.60 341,740,000

159 VHC 13.57 754,250,000

160 VDSI 13.56 177,150,000

161 SWS 13.51 137,310,000

162 OYOG 13.47 333,110,000

163 LZB 13.46 385,740,000

164 IFSIA 13.45 776,530,000

165 TSL 13.44 392,370,000

166 ABG 13.34 533,010,000

167 MEI 13.31 275,060,000

168 CWCO 13.27 114,740,000

169 PNFP 13.23 366,000,000

170 CGX 13.21 400,000,000

171 SHEN 13.19 248,750,000

172 CENT 13.15 368,770,000

173 CIR 13.13 506,690,000

174 ELY 13.11 334,100,000

175 ALGN 13.11 1,190,000,000

176 CBOU 13.08 245,130,000

177 SCBT 13.07 332,770,000

178 UEIC 13.07 235,720,000

179 NCS 13.06 150,440,000

180 EBF 13.06 340,270,000

181 NATR 13.04 194,490,000

182 KSWS 13.03 151,130,000

183 USU 13.01 150,030,000

184 KNL 13.00 633,670,000

185 FUR 12.99 268,940,000

186 ININ 12.98 509,700,000

187 PRSC 12.97 138,380,000

188 HSII 12.95 293,450,000

189 VSEC 12.90 131,970,000

190 FMBI 12.88 545,160,000

191 RSYS 12.87 171,510,000

192 TCBK 12.87 196,050,000

193 COR 12.85 252,890,000

194 KFY 12.85 581,710,000

195 SBX 12.83 145,360,000

196 LIOX 12.83 142,220,000

197 CBEY 12.81 216,830,000

198 BOOM 12.80 210,310,000

199 CBK 12.80 126,380,000

200 MPG 12.77 104,570,000

No. Ticker % Change Market Cap

201 SWHC 12.77 151,840,000

202 HNR 12.77 292,450,000

203 XIDE 12.77 293,630,000

204 PAG 12.75 1,470,000,000

205 GLCH 12.73 136,470,000

206 PCRX 12.73 151,650,000

207 XRM 12.71 146,510,000

208 PBY 12.67 519,890,000

209 SXI 12.64 370,730,000

210 CBR 12.59 218,280,000

211 JASO 12.58 292,730,000

212 MCS 12.57 295,210,000

213 ABD 12.56 263,210,000

214 PKY 12.56 243,410,000

215 GST 12.55 189,400,000

216 UFCS 12.52 423,660,000

217 FTK 12.50 232,420,000

218 MG 12.50 485,900,000

219 ZEP 12.49 312,860,000

220 HTLF 12.49 210,620,000

221 IN 12.48 388,540,000

222 PSEM 12.45 181,350,000

223 STMP 12.45 276,620,000

224 MOV 12.44 302,890,000

225 ANAD 12.44 146,480,000

226 FIX 12.44 314,300,000

227 PKE 12.41 443,210,000

228 PGI 12.41 328,910,000

229 NGS 12.37 156,860,000

230 CLFC 12.33 187,220,000

231 PKT 12.32 122,240,000

232 ISSI 12.32 210,060,000

233 AEGR 12.30 254,240,000

234 SCS 12.30 803,720,000

235 TMP 12.30 365,550,000

236 FSS 12.29 274,850,000

237 MLNK 12.28 151,180,000

238 FBC 12.22 271,550,000

239 ARII 12.19 328,390,000

240 QLTY 12.17 208,580,000

241 EXL 12.17 277,460,000

242 HOTT 12.16 342,690,000

243 EPL 12.15 445,410,000

244 SPRD 12.15 841,290,000

245 XRTX 12.10 266,770,000

246 RST 12.10 186,510,000

247 VVI 12.09 328,620,000

248 ACCL 12.09 334,910,000

249 EXEL 12.07 704,200,000

250 ZINC 12.06 282,710,000

No. Ticker % Change Market Cap

251 TLB 12.05 176,070,000

252 LABL 12.02 285,390,000

253 AHS 12.02 161,930,000

254 IPAR 12.01 471,830,000

255 RTK 11.99 167,530,000

256 NAK 11.97 509,060,000

257 SIMO 11.96 330,350,000

258 RPTP 11.96 153,260,000

259 LMIA 11.94 197,160,000

260 STEL 11.93 215,950,000

261 URI 11.89 993,410,000

262 SHFL 11.89 415,130,000

263 DLX 11.86 949,210,000

264 AVNW 11.84 137,240,000

265 PERY 11.83 287,410,000

266 FFIC 11.83 332,880,000

267 OME 11.82 175,920,000

268 SHLD 11.79 6,120,000,000

269 KLIC 11.79 542,330,000

270 DK 11.74 653,480,000

271 ISLE 11.73 187,450,000

272 NCT 11.73 297,380,000

273 PEBO 11.70 105,950,000

274 LXU 11.69 638,020,000

275 BPFH 11.68 458,820,000

276 CMRG 11.67 170,910,000

277 SMCI 11.65 457,920,000

278 SASR 11.64 352,540,000

279 AMWD 11.64 173,340,000

280 DNDN 11.63 1,340,000,000

281 CONN 11.63 228,880,000

282 ACTV 11.60 770,650,000

283 BANF 11.57 505,890,000

284 SHOO 11.57 1,210,000,000

285 CHRS 11.57 302,830,000

286 OPWV 11.56 133,290,000

287 ARCL 11.54 204,770,000

288 NEWS 11.53 468,760,000

289 BWS 11.53 298,830,000

290 SSD 11.53 1,160,000,000

291 FSR 11.50 545,440,000

292 NP 11.50 212,540,000

293 ETH 11.50 391,860,000

294 KCP 11.47 195,690,000

295 BRKS 11.44 526,490,000

296 DAL 11.43 6,350,000,000

297 ASTE 11.41 664,220,000

298 CYNO 11.41 127,260,000

299 AF 11.39 715,420,000

300 OCFC 11.38 207,620,000

No. Ticker % Change Market Cap

301 RNST 11.36 319,030,000

302 NARA 11.36 231,250,000

303 MEA 11.35 185,060,000

304 NX 11.32 405,430,000

305 CATY 11.32 894,900,000

306 GRC 11.31 518,170,000

307 GTY 11.31 481,540,000

308 CWTR 11.30 115,860,000

309 WBS 11.30 1,280,000,000

310 ARRY 11.30 111,190,000

311 RNET 11.29 224,220,000

312 LCRY 11.29 112,580,000

313 EXAM 11.28 292,070,000

314 IPCC 11.28 641,460,000

315 FST 11.25 1,610,000,000

316 SMA 11.25 264,790,000

317 HURC 11.23 129,960,000

318 FOR 11.22 382,450,000

319 SFNC 11.21 355,980,000

320 BHE 11.21 775,300,000

321 CPLA 11.20 431,520,000

322 DM 11.18 270,990,000

323 INDB 11.17 466,630,000

324 BPOP 11.16 1,540,000,000

325 RECN 11.16 445,240,000

326 TBBK 11.15 217,430,000

327 FPO 11.15 624,210,000

328 CX 11.15 3,290,000,000

329 MTW 11.15 885,060,000

330 BGG 11.14 683,440,000

331 AYI 11.13 1,530,000,000

332 ICFI 11.13 371,690,000

333 ZAGG 11.13 274,550,000

334 PVTB 11.13 539,970,000

335 SSI 11.12 408,490,000

336 QTM 11.11 419,740,000

337 TCBI 11.09 817,900,000

338 GPK 11.08 1,340,000,000

339 BXS 11.03 733,020,000

340 FARO 11.02 524,230,000

341 ROLL 11.01 745,600,000

342 AAON 10.97 388,410,000

343 DDD 10.96 705,710,000

344 PJC 10.95 284,480,000

345 DY 10.93 512,410,000

346 MRCY 10.93 348,780,000

347 FIBK 10.93 424,480,000

348 TWI 10.92 582,490,000

349 HEES 10.88 286,990,000

350 QRE 10.88 656,740,000

No. Ticker % Change Market Cap

351 OSIS 10.86 657,030,000

352 GEOI 10.86 453,130,000

353 TRMK 10.85 1,100,000,000

354 HWKN 10.82 307,460,000

355 AMCC 10.81 345,680,000

356 AIR 10.81 647,810,000

357 HF 10.81 306,000,000

358 VIVO 10.81 611,660,000

359 ARX 10.80 771,580,000

360 COLB 10.78 565,580,000

361 MSFG 10.78 176,100,000

362 BBOX 10.76 385,180,000

363 MDCA 10.76 404,900,000

364 GLF 10.74 953,740,000

365 JOUT 10.74 150,400,000

366 SYUT 10.74 272,180,000

367 CYMI 10.73 1,130,000,000

368 CRIS 10.73 241,880,000

369 FORM 10.72 316,790,000

370 RBN 10.71 1,590,000,000

371 PLXS 10.71 801,470,000

372 WMS 10.71 921,200,000

373 ABMD 10.70 415,520,000

374 HSOL 10.70 202,220,000

375 SURG 10.69 130,820,000

376 HPP 10.69 364,260,000

377 WNR 10.68 1,050,000,000

378 DATE 10.68 178,750,000

379 MS 10.67 26,050,000,000

380 CLF 10.66 7,470,000,000

381 CHOP 10.64 137,820,000

382 SEAC 10.63 236,360,000

383 EBIX 10.62 507,520,000

384 AFCE 10.59 288,470,000

385 GBCI 10.56 673,840,000

386 WASH 10.55 304,090,000

387 HAYN 10.55 524,790,000

388 TGH 10.54 965,700,000

389 CAB 10.53 1,420,000,000

390 RMBS 10.52 1,530,000,000

391 ACO 10.52 759,210,000

392 UBNK 10.51 203,010,000

393 UFPI 10.51 451,610,000

394 SUP 10.51 400,540,000

395 CAP 10.51 226,140,000

396 STL 10.49 206,260,000

397 PCBK 10.47 121,470,000

398 ENTG 10.47 861,300,000

399 ARIA 10.46 1,170,000,000

400 ARO 10.45 872,760,000

No. Ticker % Change Market Cap

401 NFP 10.44 468,190,000

402 ENV 10.42 304,730,000

403 FFIN 10.41 822,760,000

404 ABCB 10.41 207,000,000

405 LNDC 10.40 140,470,000

406 SNHY 10.40 498,400,000

407 PRTS 10.39 142,710,000

408 VNDA 10.37 135,460,000

409 PLCM 10.35 3,250,000,000

410 AVL 10.33 227,730,000

411 WAL 10.31 415,670,000

412 UTEK 10.30 413,690,000

413 AKAM 10.29 3,670,000,000

414 LSE 10.28 245,680,000

415 MSA 10.27 987,440,000

416 MCHX 10.26 284,940,000

417 UEC 10.25 173,420,000

418 AEIS 10.24 376,110,000

419 TMH 10.23 1,070,000,000

420 PRGS 10.23 1,170,000,000

421 FFIV 10.22 5,740,000,000

422 BID 10.22 1,860,000,000

423 WIRE 10.22 471,660,000

424 IIIN 10.21 177,380,000

425 FTEK 10.19 141,620,000

426 CPWM 10.18 140,620,000

427 SBNY 10.17 2,200,000,000

428 CODI 10.17 569,100,000

429 BMTC 10.15 214,560,000

430 TITN 10.15 319,120,000

431 ARB 10.15 900,370,000

432 WWWW 10.12 182,690,000

433 EXAR 10.11 255,510,000

434 FMER 10.08 1,240,000,000

435 MSCC 10.07 1,390,000,000

436 ASCA 10.07 523,890,000

437 GCO 10.06 1,250,000,000

438 ONB 10.06 883,080,000

439 CUB 10.06 1,040,000,000

440 OUTD 10.04 142,220,000

441 AUDC 10.04 129,820,000

442 SMSC 10.04 425,090,000

443 HLIT 10.03 492,890,000

444 FFG 10.03 777,930,000

445 RGR 10.03 491,260,000

446 CCBG 10.02 172,880,000

447 MPW 10.01 999,770,000

FLASH: Moody’s Downgrades Italy, Outlook Negative

Via Moody’s

Prime-1 ratings affirmed

Frankfurt am Main, October 04, 2011 — Moody’s Investors Service has today downgraded Italy’s government bond ratings to A2 with a negative outlook from Aa2, while affirming its short-term ratings at Prime-1. The rating action concludes the review for downgrade initiated by Moody’s on 17 June, 2011.

The main drivers that prompted the rating downgrade are:

(1) The material increase in long-term funding risks for euro area sovereigns with high levels of public debt, such as Italy, as a result of the sustained and non-cyclical erosion of confidence in the wholesale finance environment for euro sovereigns, due to the current sovereign debt crisis.

(2) The increased downside risks to economic growth due to macroeconomic structural weaknesses and a weakening global outlook.

(3) The implementation risks and time needed to achieve the government’s fiscal consolidation targets to reverse the adverse trend observed in the public debt, due to economic and political uncertainties.

The downgrade reflects the weight of these growing risks relative to some positive credit attributes. These include a lack of significant imbalances in the economy or severe pressure on private financial and non-financial sector balance sheets, as well as the actions undertaken by the government over the summer. Moody’s notes that the size of the rating action is largely driven by the sustained increase in the country’s susceptibility to financial shocks due to a structural shift in market sentiment regarding euro-area countries with high debt burdens. A country’s susceptibility to shocks is a key factor under Moody’s sovereign methodology.

The negative outlook reflects ongoing economic and financial risks in Italy and in the euro area. The uncertain market environment and the risk of further deterioration in investor sentiment could constrain the country’s access to the public debt markets. If such risks were to materialise and the long-term availability of external sources of liquidity support were to remain uncertain, the country’s rating could transition to substantially lower rating levels.

RATIONALE FOR DOWNGRADE

The downgrade stems from three closely related drivers:

1) The fragile market sentiment that continues to surround euro area sovereigns with high levels of debt implies materially increased financing costs and funding risks for Italy. The country is a frequent issuer with refinancing needs of more than EUR200 billion in 2012. Although future policy actions within the euro area could reduce investors’ concerns and stabilise funding markets, the opposite is also increasingly possible. Even if policy actions were to succeed in the short term in returning some degree of normality to euro area sovereign debt markets, the underlying fragility and loss of confidence is deep and likely to be sustained. As indicated by the A2 rating, the risk of default by Italy remains remote. Nonetheless, Moody’s believes that the structural shift in sentiment in the euro area funding market implies increased vulnerability of this country to loss of market access at affordable rates that is incompatible with a ‘Aa’ rating. Moreover, the preponderance of downside risks and the potential for rapid rating transition which those risks imply are not compatible with a rating at the top end of the ‘A’ range. The repositioning of Italy’s government bond rating to A2 reflects Moody’s judgment of the balance of long-term risks facing the Italian sovereign. It is consistent with Moody’s broader reassessment of sovereign risk in the euro area, focusing on member countries that are more susceptible to confidence-related shocks due to high public debt exposure and/or large fiscal imbalances.

2) The Italian economy continues to face significant challenges due to structural economic weaknesses. These problems — mainly low productivity and important labour and product market rigidities — have been an impediment to the achievement of higher potential growth rates over the past decade and continue to hinder the economy’s recovery from the severe recession it experienced in 2009. These structural impediments to economic growth cannot be removed quickly. The government’s reform plans have only just started to address some of these structural challenges, and they need to be implemented efficiently. Moreover, moderate medium-term growth prospects for the Italian economy have been further revised downwards due to potential adverse effects of a weakening European and global growth outlook. Economic growth will be a crucial factor determining the government’s revenues, the achievement of fiscal consolidation targets and, ultimately, its debt trajectory.

3) Finally, there is increasing uncertainty for the government to achieve fiscal consolidation targets. Since more than half of the consolidation measures are based on government revenue growth, the plans are vulnerable to the high level of uncertainty around economic growth in Italy and elsewhere in the EU. Moreover, political consensus on additional expenditure cuts can be difficult to achieve. As a consequence, the government may find it challenging to generate the primary surpluses that are needed to place the public debt-to-GDP ratio and the interest burden on a solid downward trend. Moody’s expects Italy’s public debt-to-GDP ratio to reach 120% at the end of this year, up from 104% at the start of the global crisis. As well as posing a risk to Italy’s financial strength, which is a key consideration under Moody’s sovereign methodology, failure to achieve fiscal and debt targets could increase the country’s susceptibility to financial market shocks.

PRINCIPAL METHODOLOGY

The principal methodology used in this rating was Sovereign Bond Ratings published in September 2008. Please see the Credit Policy page on www.moodys.com for a copy of this methodology.

REGULATORY DISCLOSURES

For ratings issued on a program, series or category/class of debt, this announcement provides relevant regulatory disclosures in relation to each rating of a subsequently issued bond or note of the same series or category/class of debt or pursuant to a program for which the ratings are derived exclusively from existing ratings in accordance with Moody’s rating practices. For ratings issued on a support provider, this announcement provides relevant regulatory disclosures in relation to the rating action on the support provider and in relation to each particular rating action for securities that derive their credit ratings from the support provider’s credit rating. For provisional ratings, this announcement provides relevant regulatory disclosures in relation to the provisional rating assigned, and in relation to a definitive rating that may be assigned subsequent to the final issuance of the debt, in each case where the transaction structure and terms have not changed prior to the assignment of the definitive rating in a manner that would have affected the rating. For further information please see the ratings tab on the issuer/entity page for the respective issuer on www.moodys.com.

This rating was initiated by Moody’s and was not requested by the rated entity.

This rated entity or its agent(s) participated in the rating process. The rated entity or its agent(s) provided Moody’s access to the books, records and other relevant internal documents of the rated entity.

The rating has been disclosed to the rated entity or its designated agent(s) and issued with no amendment resulting from that disclosure.

Information sources used to prepare the rating are the following : parties involved in the ratings, parties not involved in the ratings and public information.

Moody’s considers the quality of information available on the rated entity, obligation or credit satisfactory for the purposes of issuing a rating.

Moody’s adopts all necessary measures so that the information it uses in assigning a rating is of sufficient quality and from sources Moody’s considers to be reliable including, when appropriate, independent third-party sources. However, Moody’s is not an auditor and cannot in every instance independently verify or validate information received in the rating process.

Moody’s Investors Service may have provided Ancillary or Other Permissible Service(s) to the rated entity or its related third parties within the three years preceding the credit rating action. Please see the special report “Ancillary or other permissible services provided to entities rated by MIS’s EU credit rating agencies” on the ratings disclosure page on our website www.moodys.com for further information.

Please see Moody’s Rating Symbols and Definitions on the Rating Process page on www.moodys.com for further information on the meaning of each rating category and the definition of default and recovery.

Please see ratings tab on the issuer/entity page on www.moodys.com for the last rating action and the rating history.

The date on which some ratings were first released goes back to a time before Moody’s ratings were fully digitized and accurate data may not be available. Consequently, Moody’s provides a date that it believes is the most reliable and accurate based on the information that is available to it. Please see the ratings disclosure page on our website www.moodys.com for further information.

Please see www.moodys.com for any updates on changes to the lead rating analyst and to the Moody’s legal entity that has issued the rating.

Alexander Kockerbeck

VP – Senior Credit Officer

Sovereign Risk Group

Moody’s Deutschland GmbH

An der Welle 5

Frankfurt am Main 60322

Germany

JOURNALISTS: 44 20 7772 5456

SUBSCRIBERS: 44 20 7772 5454

Bart Oosterveld

MD – Sovereign Risk

Sovereign Risk Group

JOURNALISTS: 212-553-0376

SUBSCRIBERS: 212-553-1653

Releasing Office:

Moody’s Deutschland GmbH

An der Welle 5

Frankfurt am Main 60322

Germany

JOURNALISTS: 44 20 7772 5456

SUBSCRIBERS: 44 20 7772 5454

FLASH: Dexia to be Bailed Out

Belgium Confirms Creation Of A ‘Bad Bank’ For Risky Assets

Comments »FLASH: Acme Packet Destroyed on EPS Warning

-30%

Co issues downside Q3 guidance and Co also reaffirmed 2011 EPS of $1.14-1.18 vs. $1.13 Capital IQ Consensus Estimate; reaffirms revs of $315-320 mln vs. $325.2 mln consensus. Co said, “While we remain confident in our second half growth plans, our Q3 results were adversely impacted by a very large opportunity at one of the two largest service providers in North America. We now expect this opportunity to close in the first half of Q4 and we remain confident in our ability to execute on our full year business outlook. I continue to believe we are well positioned to leverage the broad, multi-year, secular growth drivers associated with the global transition from TDM to IP for real time communications like voice and video. The co was recently selected as the session border controller supplier for a major universal voice platform at this Tier-1 service provider in the United States. This platform is initially designed to support the existing customer’s “over-the-top” and wireline service offerings and will become a key infrastructure component to their Voice over Long Term Evolution offering. This platform is expected to become one of the largest such deployments in North America, supporting over 100 million subscribers. The initial deployment, which the co estimates will support ~5 mln subscribers, was expected to close in Q3 of 2011. However, during the final stage of Q3, the orders associated with this initial deployment were delayed to Q4. Accordingly, the co now expects this opportunity to close in the first half of Q4 of 2011.

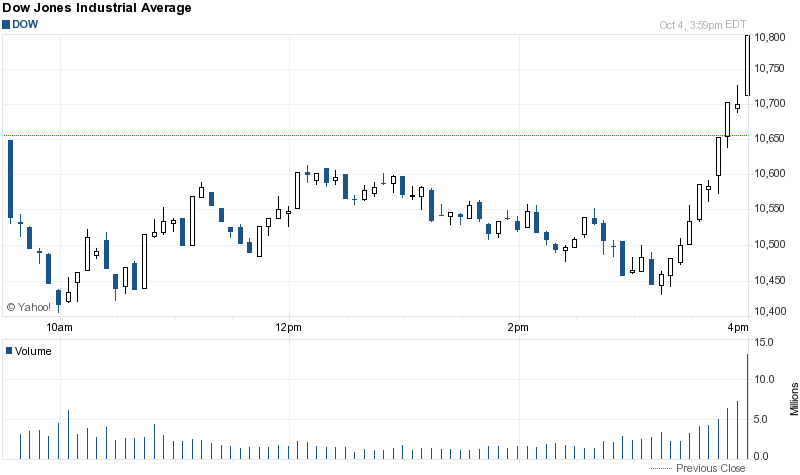

Comments »FLASH: The Market Stages an Incredible Late Day Rally

So You Want Little Government; Be Careful What You Kill

Not that i’m for big government or a fan of the FDA, but if you want to dismantle it and make it smaller please remember to beef up important aspects for citizen protection….

Comments »