The fed decision to test the waters with a taper while I was away did surprise me, somewhat. Yet it did not phase me much and so I elected to remain on vacation, silent on the issue.

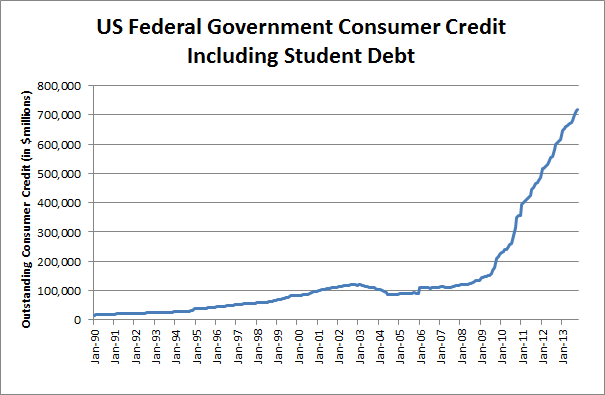

I would state now in hindsight that a $5B per month taper (with as much as another $5-10B in the works) would still put the Federal Reserve on path to add another ~$800B to its balance sheet in 2014. This remains colossal and would have the Fed assets outstanding at just under $5 Trillion by 2015.

They may very well have tapered by $5B/month just because they were running out of things to buy…(laughter)

If I were to state things that concern me as potential impediments to the US economy and growth, they would list (1) consumer slowdown from budget impacts (pension, healthcare costs, rents/mortgage, increased retirement contributions, etc), (2) foreign existential shocks (EU breakup, Asian crisis, similar collapse that disrupts foreign trade) – where exactly did the EU government debt go and why is it now suddenly not an issue? Who is buying it (ECB, Fed, banking scheme, inter-government trade imbalances, etc)? And what stops non-payment concerns from popping up again in the future? and (3) the election of a Republican majority

But banking solvency just isn’t on that list right now. Neither is inflation, really, although long term prospects of an uncontrollable outbreak of inflation remains a viable possibility. With credit expansion in this country limited to growth of government balance sheets, deflationary pressure is set to commence…until it doesn’t. In the meantime, another ~$1 Trillion of free money to those closest to the trough will keep a major disruption of financial assets here at home as a low probability outcome. Of course, this bodes ill for the “wealth equality” lot, but they’re too dumb to call the system out on that, so we maintain the course.

Concerns aside, I am optimistic. Recessions don’t last forever, and my concerns are outweighed by hope in outlook. I am very long (no margin) and prepared to reap the rewards of economic growth. It’s been almost six years; the system has been on a hyperactive outlook for problems which greatly reduces the likelihood that a real “Black Swan” manages to crop up. It could still happen of course, but with hundreds of thousands of financial professionals calling bubbles as quickly as problems crop up, and a full time central banking staff armed with an unlimited supply of money attacking them at first sight, how exactly is a crisis supposed to materialize from all of this?

The only room for crisis in the US is rampant commodity/asset appreciation, which remains benign. That or an elsewise major shock to the consumer. Financial assets and liquidity issues are covered.

Now, that being said, historically we haven’t had a period longer than 10 years without a recession since at least 1789 (and probably not since long before that either – I just lack records to verify a more robust claim). I’d say the expectation of a correction since the Great Depression is 5-10 years with occasional 1-3 year shocks intermittently. We’re past the small shocks phase, which would put the expectation at right about where we’re at.

These times are unprecedented and the support the Fed is willing to lend the markets (unlike any time in recorded history) makes me think we blow through the averages. I want to say this ship will have the wind to sail to years seven, eight or nine, uninterrupted. We may even match the record holder of 10 or above.

However, it would be foolhardy to doubt another recession will most likely crop up before 2020. The ever growing levels of margin debt to buy equities may well be the first sign of the beginning of the final run before that. Of course it could be nothing.

My belief then is that a long commitment remains the way to go. I have been positively surprised by recent developments that have overridden prior comments on wanting to have a larger cash position by about this time (end of 2013) that I made late last year. However, as gains are taken, a portion should begun to be set aside, starting sometime mid 2014 to early 2015. This should create a reserve build-up of steadily marching intervals (10-20%, with a 1-2% increase every month topping out at around 40-50% of ones account value) sometime around late 2015 to early 2016.

At such time, a second hard look should be had. Earlier and exceptional strength should trigger a reassessment of these statements. Casual to quality growth does not necessarily change them. A major weakness (such as a shock of a GOP majority and fear of monetary policy interference) of course may necessitate a sudden course change.

My most hated places to invest are land/real estate (excluding multifamily or renting derived), oil companies (excluding natural gas predominated), and retail (excluding facilitation to the ultra-rich).

My favorite places center around natural gas production expansion, uranium, coal, multifamily REITs, and I remain interested in holding physical precious metals in a full position in the event an inflation shock from significant expansion in credit hits the economy.

I’m indifferent to the insurance market – especially health insurance. It could swing either way; they crawled into bed with the devil so it’s all political at this point. On the one hand, the entire market is shifting in wild and unpredictable ways. On the other, the feds are rigging the game in the insurance companies favor. Just stay away.

Comments »