Link to Part 1

There may have been some confusion on the hold time before rotation. The system will hold each ETF a minimum of one month before re-ranking them and either rotating out and into a different ETF at the close of the month or holding the existing position(s) for another month.

Let’s Make it Better

At the conclusion of Part 1, I alluded to two additional factors that improve the performance of the system. The two factors are including a return on cash and implementing a moving average filter.

The return on cash code for Amibroker is available for free over at AmibrokerU. Simply register and then follow the links through the Free Library. These tests will show the result of using either $SHY (i-Shares Barclays 1-3 Years Treasury Bond ETF) or $TLT (i-Shares Barclays 20+ Years Treasury Bond ETF).

The moving average filter has the system rotate out of a position if the monthly close is beneath a monthly moving average. The results below will show a 4 month moving average. The 4 month is optimum, but the next best monthly moving average periods to use are 5, 3, 6, 7, 8, 9, and 2, respectively. What this demonstrates is there is a fairly generous range of monthly moving average periods to use. While 4 is optimum over the test period, it may still prove to be robust going forward. One my choose to err on the safe side and choose a 5 or even 6 month moving average period.

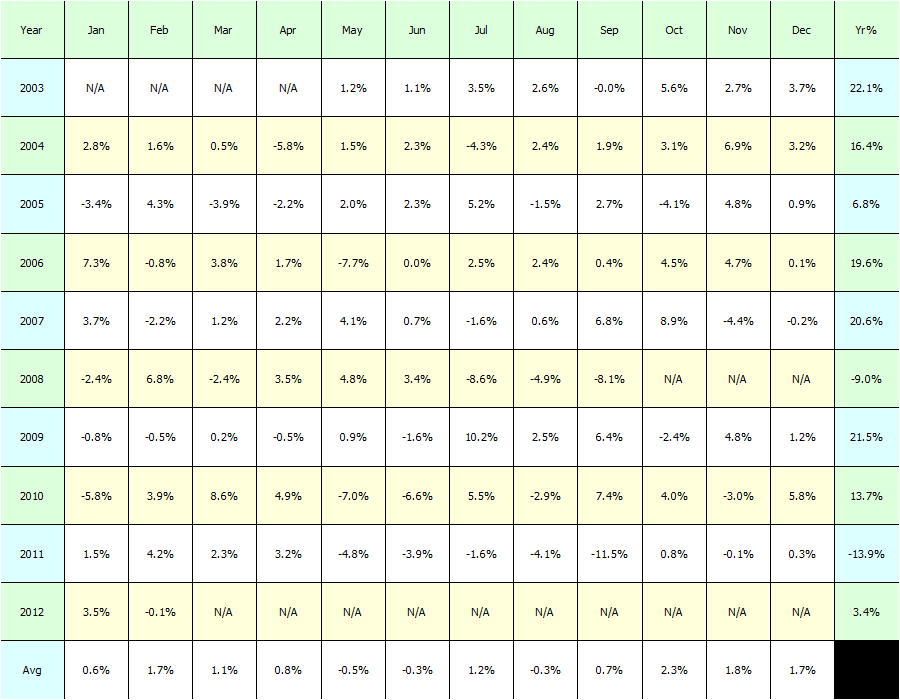

Results:

We see all metrics have improved over the model in Part 1, especially the maximum system % drawdown.

For fun, let’s use $TLT rather than $SHY for our return on cash.

These results with $TLT may not be generalizable since $TLT has been a standout performer due to the recent market environment.

The following charts/graphs were generated using $TLT for the return on cash.

Equity Curve:

Note how $TLT allowed the system to gain ground when it would have been in cash (green areas), especially in 2003 and the end of 2008.

Historical Profits:

Thoughts:

All the caveats noted in Part 1 still apply.

For fun, I added in commissions of $7.95/trade, and they lowered the annual return to 16.36%. Using an Interactive Broker’s commission of .005/share lowered the annual return to 17.41%, or a reduction of -0.05%.

Some helpful comments with suggestions for improving performance were left in Part 1. Based on those suggestions, I’m going to make some tweaks to the system and report results. If you have any ideas, feel free to leave them in the comments section.

Comments »