I had planned to exhaust the long-side studies of the historical performance of RSI2 before tackling the short-side, but since Thursday’s SPY RSI2 closed just above 80, I decided it would be interesting to jump ahead and take a look at the short-side historical performance.

While a RSI2 reading above 80 is not extreme, 80 is an often used RSI2 boundary marker. Let’s look at the historical performance of shorting SPY at the close anytime RSI2 closed above 80. The short will be covered at the close 5 days later.

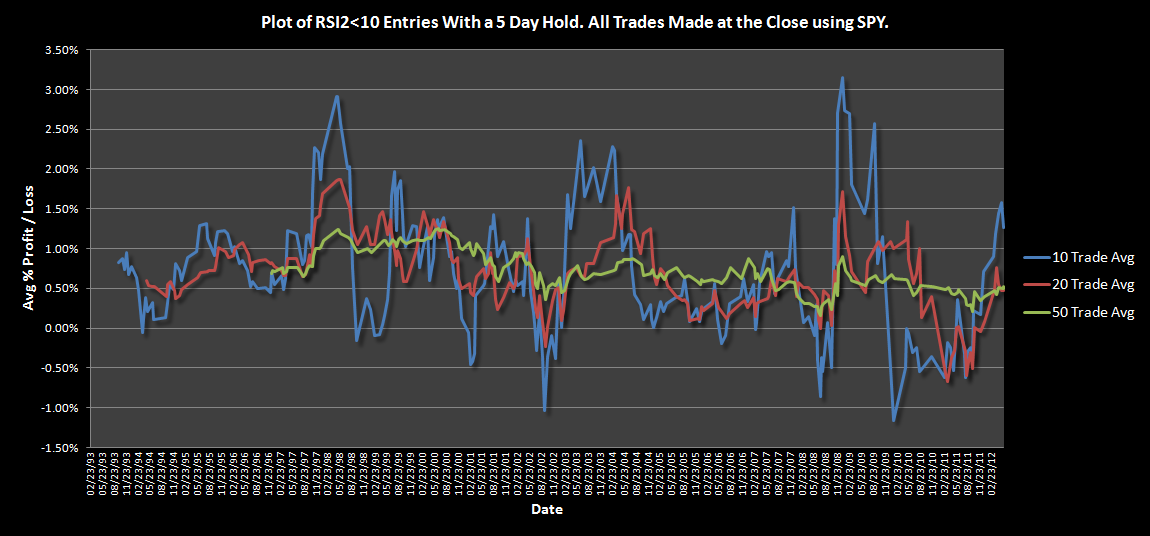

Click on the graph to enlarge…

What I think when I look at that graph is there is not enough meat on the bone to make me want to short SPY only because the RSI2 is greater than 80. The 20 and 50 trade averages have oscillated around 0.0% with some lengthy dips into negative territory. Unless timing was impeccable, it would be almost impossible to consistently make money using this setup and a 5 day exit.

Some observations…During the bear market of 2007-2009, RSI2>80 did not provide out-sized gains, as one might expect it would have. During the low volatility bull market of 2003-2007, the historical performance slowly deteriorated.

I have a strong feeling that adding a filter such as only shorting when SPY is beneath the 50 day average would improve historical performance.

An important caveat is that the exit strategy may not be a great match. We’ll see the effect of the exit in later studies.

Final note: Based on the 10 trade average, it appears that shorting SPY with a RSI2>80 might soon be in for a string of losing trades.

Comments »

{kind=link}