A summary is below the sheet.

Click on spreadsheet to enlarge…

November will mark the one year anniversary of the inception of PDS subscription service. As we approach the beginning of the second year, I am in the process of reviewing the system in order to make any necessary changes for implementation the 2nd year. I’m not anticipating any changes to the original algorithm; rather, the changes will likely involve an adaptive position-sizing method, or at the least, refining the original methods.

The tests represented above attempt to answer two questions:

1. Would adding an additional uptrend requirement and trading only low or high volatility stocks improve the system?

2. Does ATR position-sizing or fixed-stop position-sizing work better during bear markets?

Reading the Sheet:

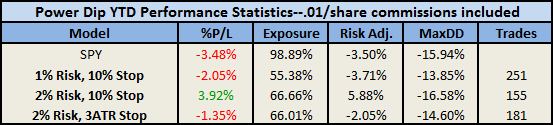

All tests include .01/share for commissions and were run over de-listed data from Premium Data.

- The top half of the sheet (above the blue horizontal line) shows the results of testing from 7/1/2007 – 9/4/2010. I consider this period to encompass the current bear market (which includes the bull run of 2009).

- The bottom half of the sheet (below the blue horizontal line) shows the results of testing from 4/1/2000 – 6/1/2003. This period represents the bear market that followed the tech crash.

- The white columns show the fixed-stop results (1% Risk, 10% Stop) with the uptrend requirement (U) and either low (L) or high (H) volatility stocks.

- The gray columns show the same tests with ATR position-sizing using 1% Risk.

Interpreting the Results:

For this type of system, opportunity is everything. I cannot emphasize that enough.

- While the U_H (uptrend and high volatility) models have a significantly higher average trade during the 2000 bear market period than the baseline models, opportunity is limited to the extent that they under perform in terms of net percentage gain. However, the higher average trade is encouraging and it may mean that we flag those higher volatility picks so that subscribers can adjust position-sizing in an attempt to capture a larger gain. The data show other added benefits to the U_H and U_L picks.

- During bear markets, ATR position-sizing appears to under perform fixed-stop position-sizing. This is contrary to my own intuition. While I need to run similar tests during bull markets to be sure, I’m fairly sure that ATR position-sizing is most beneficial when volatility is low (as we would expect during bull markets) as it requires taking larger positions than we would with fixed-stop sizing. Excluding net percentage gain, the data show that there are other benefits to using ATR position-sizing rather than fixed-stop.

More Testing Ahead…

I am currently working on an adaptive model which will change both risked amount and position-sizing models based on the market environment. Also, I have combined ATR position-sizing with fixed-stops, and the results are encouraging. I will publish the results as soon as they are available.

Comments »

{kind=link}