August was a horrible month for equities while PDS mostly dodged the downturn.

A note about how the report is generated. The monthly statistics, %P/L and %CAR are calculated from January 4th (first trading day of 2010) to the present, NOT starting from August 2nd to August 31st. The difference is that the system may have been holding open positions going into August that affect that months performance where if one started trading the system on August 2nd (first trading day of August), there wouldn’t have been any already opened positions.

The rest of the statistics, W/L%, Avg.Trade, and Trades are calculated from August 2nd to August 31st in order to give an accurate account of one month’s performance.

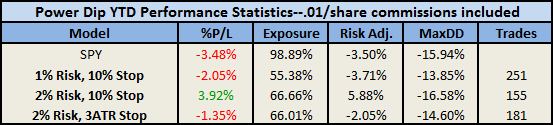

Year-To-Date Performance as of 9/1/10:

YTD PDS is outperforming, but not by a wide margin. As the S&P500 has spent about half of 2010 beneath the 50 day moving average, this market is challenging for a long-only system. Furthermore, PDS requires stocks be in an uptrend in order to be considered. There simply haven’t been many stocks in an uptrend due to the market weakness, which means less opportunity for the system to profit (note the exposure percentages which show that the system has spent a lot of the year with cash not invested).

For those not familiar with the system, the different models (1% Risk, 10% Stop) do not represent different rules for the system but rather different methods for betting on its stock picks.

The system closed its last open position today (for a win) and is awaiting a pullback in the broader markets to generate some dips.

{kind=link}

Here are all of my trades that closed in Aug:

1.56%,1.17%,1.07%,0.94%,-2.24%,-5.09%,-0.55%,1.27%,-4.05%,0.68%,-0.58%,1.30%,0.47%,1.93%,1.16%,

7.10%,-1.57%,4.52%,-0.41%,-3.11%

In case this is helpful, my net gain for Aug. was 1.246% of the port.

And most of these were at 2% risk 3xATR stop, although, I believe a couple were 1% risk 3xATR stop.

Since I’m currently only using half of my port for these trades, I ran out of cash and couldn’t trade all of the picks.

Also, I purposely refrained from trading a pick twice although some of the picks came up more than once.

Finally, because I raised my risk from 1% in July to 2% in August, my profit for August was 60% of what it was for July, which was indeed a better month.

Did it help that I missed some trades in Aug? I’m not sure, because lot of the ones I missed seemed to turn out as winners.

Also, I sold some positions early before the 3:30 exit time, which turned out better than waiting and some that turned out much worse. Also, I remember one that was $9 dollars away from an exit with a substantial profit that I waiting for only to take a considerable loss much later.

So for anyone interested in this system, the above should serve as the anecdotal report of one traders month, which I’m feeling pretty good about.

But the math and science of it I leave to Wood!

Thanks Hawaii! Seriously, it makes me very happy to see others profiting from the system. To see you make over 1% during the worst month for stocks in almost 10 years makes me very happy.

Some points- kudos to you for allocating your entire account to one system, ideology, etc.

Secondly, the realization of biases which usually lead to losses but at the time seem the right thing to do is very crucial. The system serves as an objective measure of performance by which biases can be exposed.

Thirdly, with the trade that was very close to meeting its exit objective but turned into a large loss, you held on, and followed the rules. This particular instance, you lost, but you adhered to the rules which over time leads to success.