It has been almost a year since iBC opened PDS for subscription. You learn a lot about yourself when trading a system, and many of the subscribers have shared with me what they have learned. These discussions have been very helpful as I prepare for the system’s second year in subscription.

Without a doubt, the hardest part of system trading is trading the system. Because of this fact, it is important to make the trading part of it as simple as possible. All rules and methodology should be very clear and easily implementable. The psychology part of system trading is hard enough. We don’t want complex rules or order entry requirements to make things even harder.

To that end, I am making some changes in how I recommend subscribers trade the system. These changes will be reflected in PDS site literature over the next week or so, but I am going to outline them here.

- All models will use all available cash, any given day, assuming there are enough picks to use the cash. Previous rules limited new buys to 5 per day in the 1% risk models and 3 per day in the 2% risk models. Limiting new buys per day was done to decrease the drawdowns. This decrease was slight, and I’m inclined to believe that the inconsistency that may result from being unclear exactly how to trade the system may hurt performance more than the expected reduction in drawdowns can improve it.

- With the exception of the 1% risk models, the system will no longer be allowed to take multiple positions in the same security. While I have always advocated not taking multiple positions in the same security, I continued to allow the system to do so, for a variety of reasons (high win % being the primary reason). Then came ALKS. Having 2 positions in ALKS using a 2% risk model would have been devastating. I will continue to allow the 1% risk models to take multiple positions in the same stock, as two positions at 1% risk equal one position at 2% risk.

These changes should simplify the mechanical aspect of trading the system: Buy as many stocks as you have cash to purchase, and don’t take multiple positions in the same stock unless you are trading at 1% risk.

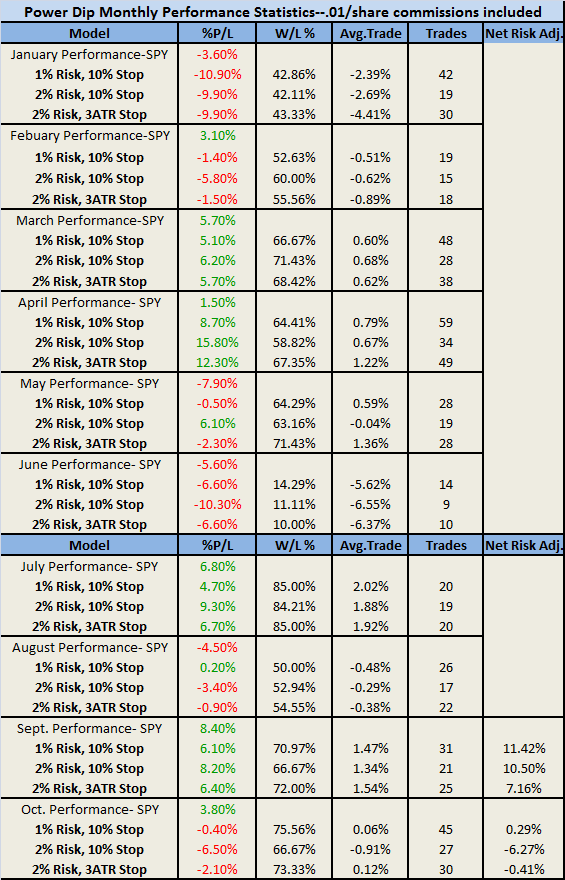

Year-To-Date Results:

Summary of Results:

The top part of the graph with the gray background reflects the results as I’ve been tabulating them since inception. The ALKS trade knocked the system backwards so that it is not currently beating the benchmark. The silver lining for me is that the 2% Risk, 3ATR model is less than 1% shy of its benchmark, even after suffering a large loss with ALKS.

To be clear, the YTD results start calculating at the open of the first trading day of the year.

The lower part of the graph with the white background reflects the historical results with some added “what ifs,” which include the changes that I discussed earlier.

My favorite “what if” is what if the system wouldn’t have traded ALKS? Had it not bought ALKS, PDS would be near doubling the performance of the benchmark, at 15.81% YTD. Even better, what if we figured no ALKS and .005/share for commission (consistent with Interactive Broker’s commission costs)? Now we are at 21.15% YTD.

The bottom three rows demonstrate YTD performance with the simplified rules of no multiple entries and no limit on new buys per day. While these changes improved performance so far this year, during previous years these factors have slightly reduced performance. Again, I think the added simplicity, leading to greater consistency, is what is important.

Looking Back and Looking Ahead…

Despite the recent setback, I am satisfied that real-time PDS performance is consistent with what I expected from historical backtesting. November 18th marks the year anniversary, and I am very excited to see this system moving into its 2nd year of subscription.

Comments »

{kind=link}