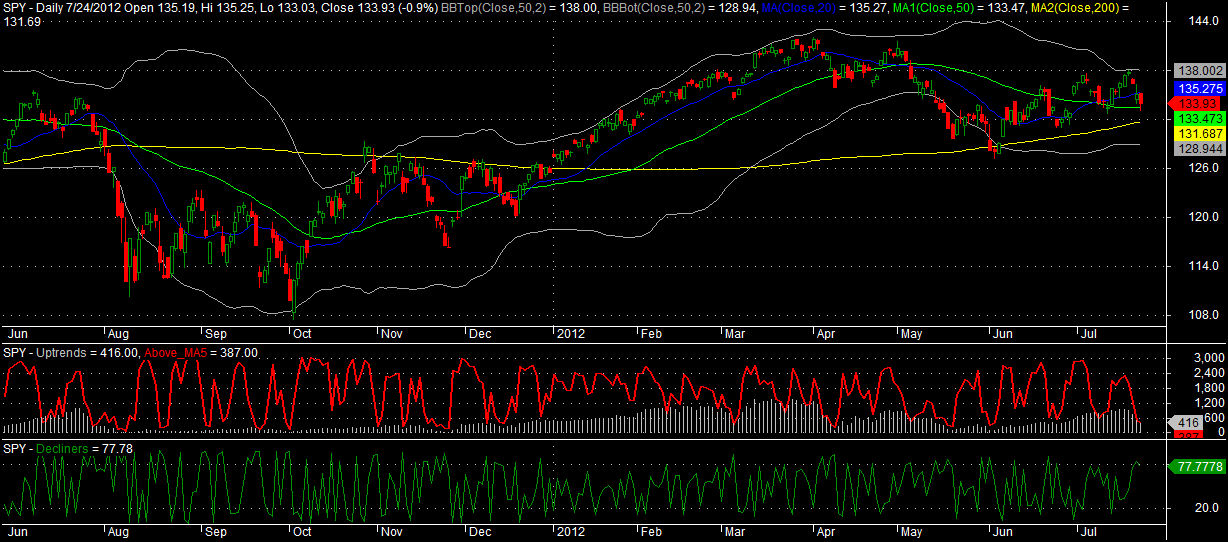

These short-term breadth indicators are at levels which typically signify that a bounce is near.

The red line is the number of major exchange listed stocks trading above their 5 day moving averages. Levels below 600 are good for a bounce that may last several days.

The green line is the number of declining issues ranked against the previous days of declining issues over the last year. Long story short, anything over 80 is good for a quick one or two day bounce (or sometimes just a stabilization). It is not quite at 80, but it is close enough to give it due consideration.

While we’re at it, let’s take a look at the percentage of stocks trading above their 20, 50, and 200 day moving averages.

I’m giving the most weight to the green line, which is the percentage of stocks above their 20 day moving averages. It is getting close to a level which may lead to a bounce that can be sustained for a week or more. As a this recent post demonstrated, when the green line dips under 20, sustained bounces often occur.

My best guess is that a quick 1-3 day bounce will occur within a day or two. Beyond the very near-term, I don’t have enough evidence to make a call with any conviction.

Comments »