Good article from Business Insider where Ethan Harris of BOA says he’s very concerned about the market due to the on going Eurozone problems and the pending fiscal cliff in Q4

In our view, the markets have been lulled to sleep by a temporary remission in negative macro news.We remain very concerned about the outlook. In our view, the markets have been lulled to sleep by a temporary remission in negative macro news. The better US data probably reflects a combination of the usual random variation and weather distortions. Mild weather boosted the winter statistics, there was a payback in the spring and now the data are settling into a weak trend…

We believe the Euro zone crisis is far from over. At this stage the policy pattern for Europe is well established: (1) A funding problem in one of the peripheral countries arises; (2) policy makers engage in brinkmanship with the core demanding austerity and the periphery demanding bailout; (3) the markets start to melt down; (4) policy makers do just enough to satisfy the markets, but not cure the underlying problem. There is nothing merry about this go around. Over time it undercuts the foundations of the Euro zone. The economy steadily slides into recession, populist parties grow in strength and the markets become increasingly fragile. For the US and the rest of the world this means ongoing collateral damage, primarily through confidence and Capital Markets.

The worst of the US fiscal crisis also lies ahead. Note that in the uncertainty shock literature, the impact of the shock grows exponentially as the day of reckoning approaches. The cliff is slowly working its way into corporate thinking. The real test will come in the fourth quarter when the cliff will be just months away and the incentive to delay spending and investment decisions will peak. The timing is tough, but we would expect some weakening in the September data and very soft numbers in the October to January period. We are keeping a close eye on corporate commentary, confidence surveys, indicators of hiring and capital goods orders.

Economist Michael Hanson points out an interesting circular relationship between the stock market and Fed policy:

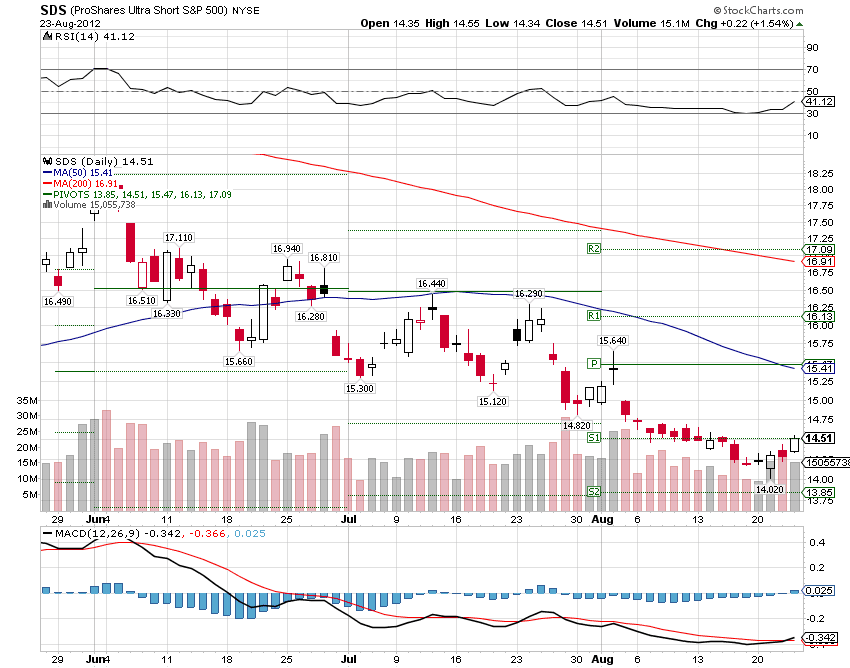

Risk of a sell-off is high

Economist Michael Hanson points out an interesting circular relationship between the stock market and Fed policy. There are some who believe the Fed will not launch QE3 so long as stock prices remain high, yet the stock market is high because it anticipates QE3. Should the Fed disappoint at the September 12-13 FOMC meeting, the risk of a stock sell-off is high. S&P 500 support on a correction is in the 1360-1325 area. Additional support is at 1300-1250. Attention will be on the Jackson Hole symposium next week to get a feel for the Fed’s tone

Our strategists see an unusually high number of macro catalysts over the next 3-6 months that could take markets lower. We expect economic growth to disappoint in the second half of the year in anticipation of the fiscal cliff. This would exacerbate any slowdown from the deepening recession in Europe and decelerating growth in emerging markets. There is also the ongoing tension in the Middle East, the potential for a US credit downgrade and accelerating downward analyst estimate revisions. To top it off, September is seasonally the weakest month of the year for stock price returns.

The BofA strategists conclude that with the VIX at record low levels, those looking to hedge against a correction should buy put options on stocks while they are cheap, echoing a message several Wall Street analysts have relayed on television and in client notes over the past week.

David Kostin Goldman Sachs Chief U.S. Equity Srategist ,writes to clients that “portfolio managers have been swayed by”hope over experience”

A look at the 2011 trading pattern of the S&P 500 explains the reason for our belief that the market has an asymmetric risk profile and offers more downside than upside. Last year the deadline for Congress to raise the federal debt ceiling was known months in advance. Nevertheless, Congress was unable to reach an agreement that satisfied all factions. Investors were stunned and the S&P 500 plunged 11% in 10 trading days (and more than 17% from the level one month prior to the deadline). Eventually Congress reached a compromise on raising the debt ceiling.

We believe the uncertainty is greater this year than it was 12 months ago…Political realities and last year’s precedent suggest the potential that Congress fails to reach agreement in addressing the “fiscal cliff” is greater than what most market participants seem to believe based on our client conversations. In our opinion, equity investors seem unduly complacent on this issue. Portfolio managers have been swayed by hope over experience.

Assigning a P/E multiple to various ‘fiscal cliff’ and earnings scenarios is difficult because ultimately we expect Congress will address the situation. But investors must confront the risk they may not act until the final hour. Exhibit 4 contains a matrix of potential year-end 2012 S&P 500 index levels based on different ‘fiscal cliff’ resolutions and multiples. Our 1250 target reflects our ‘fiscal cliff’ assumption and a P/E slightly below 12x. Full expiration with P/E of 12x equals 1120 (-21%). A 14x P/E and full extension implies 1540 (+9%), but the two outcomes are not equally likely in our view.