is called pheed and Forbes thinks it might be

Think of it as twitter with a business plan and Facebook without all the noise.

Hit me up at:

VVUS Pharmaceuticals – their claim to fame has been a much hyped wight loss drug Qsvia.

Too bad it was just rejected for sale Europe

5:31PM Vivus receives formal decision from CHMP: the CHMP recommended against approval of Qsiva as expected (VVUS) 21.06 -1.24 : Co announced that is has received the formal opinion from the European Medicines Agency’s (EMA) Committee for Medicinal Products for Human Use (CHMP) following their October 15-18 meeting. As expected, the CHMP recommended against approval of the Marketing Authorization Application (MAA) for Qsiva (phentermine/topiramate ER) for the treatment of obesity in the European Union. The reasons for their decision were due to concerns over the potential cardiovascular and central nervous system effects associated with long-term use, teratogenic potential and use by patients for whom Qsiva is not indicated. The company currently intends to appeal this opinion and request a re-examination of the decision by the CHMP. “The lack of effective pharmacologic treatments for obesity remains a high medical need for many patients in Europe,” stated Peter Tam, VIVUS’ president. “We are committed to getting Qsiva approved in Europe and will work closely with the new rapporteur and co-rapporteur to make this happen.”

In after hours trading the stock is down to $20.55 on the bid / $20.95 on the ask. This is after declining 5.5% ($1.24) today

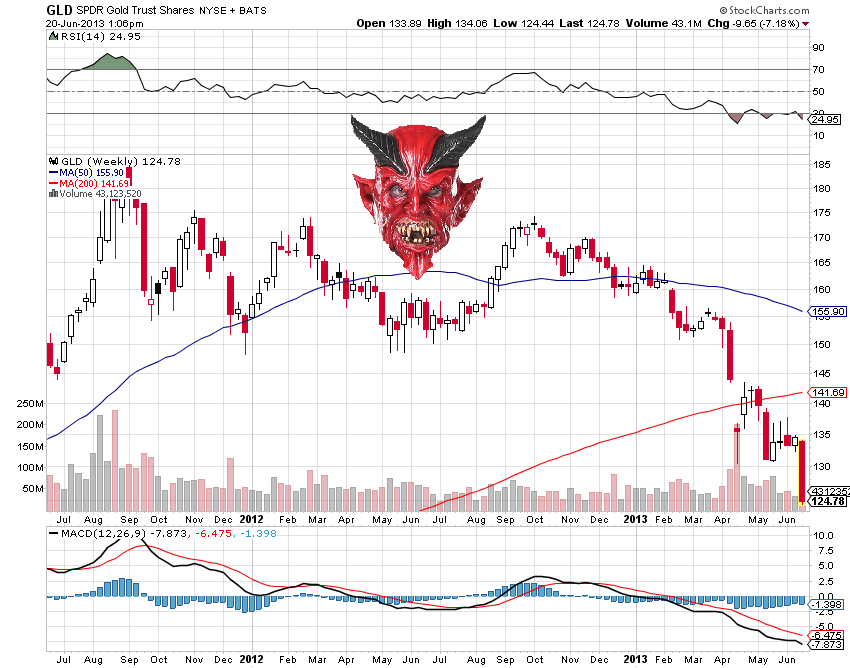

Looking at the chart you can see they are headed back to the pivot tomorrow and in high probablilty the recent swing low at $17.21. If that happens to break – it’s a long way down to fill the gap

Right here – Right now.

We wither break the trendline from the June 9 lows or we go higher.

RSI and MACD both say it’s headed south

Jack Welch was spot on regarding his skepticism of today’s jobs report.

What the report didn’t tell you was that 342,000 Americans dropped out of the workforce.

This article from UPI sums it up pretty well:

The Labor Department report said 12.1 million people were unemployed, a drop of 456,000 from the previous month.

That figure is critical because 342,000 more people dropped out of the workforce than gained employment in September. The September rate fell to 7.8 percent in part because it reflected an increase in the number of jobs initially reported in July and August.

Although the number is officially described as representing people who elected to care for a relative at home or return to school, many did so because they were simply too discouraged to continue looking for work.

So what is the ‘real” unemployment number for our country? It’s a guesstimate at best as there’s no way to measure all those who have run out of unemployment benefits and stopped looking for work all together. The Romney camp estimates the true number to be closer to 11%. They arrive at that figure by by applying the labor force participation rate from when Obama took office to today’s population:

“The labor force participation rate in January 2009 was 65.7 percent,” Williams said. Since then, the rate has fallen to 63.3 percent. “Had the rate remained the same, the labor force would be about 160,158,000. At that labor force level, the unemployment rate would be 10.7 percent.”

As noted in this article, though, it’s also impossible to guage the number of retirees during the recession. This was documented in this report by the Chicago branch of the Federal reserve.

What is clear is that this 7.8% number will be put out to the electorate as a sign of recovery. I’ll expect to hear it in the upcoming debates. The headlines and pundits have filled the web with it today

To that I’ll simply ask “then why didn’t the markets explode today?”

I’ve been neutral about the Presidential race up until now, as neither candidate represents what I’m looking for in a leader. I’ve also resisted most of the tin foil hat conspiracy theories and muck slinging.

But when something this blatant is put forth as this- it compels me to choose the lesser of two evils.

According to Cliff Frohlich, associate director and senior research scientist at the University of Texas at Austin’s Institute for Geophysics, the earthquakes that occured this past weekend near Dallas appear to be connected to the past disposal of wastewater from local hydraulic fracturing operations.

During hydraulic fracturing, or “fracking,” millions of gallons of high-pressure, chemical-laden water are pumped into an underground geologic formation (the Barnett Shale, in the case of northern Texas) to free up oil. But once fractures have been opened up in the rock and the water pressure is allowed to abate, internal pressure from the rock causes fracking fluids to rise back to the surface, becoming what the natural gas industry calls “flowback,” according to the Environmental Protection Agency.

“That’s dirty water you have to get rid of,” said Frohlich. “One way people do that is to pump it back into the ground.”

In a study he recently published in the journal Proceedings of the National Academy of Sciences, Frohlich analyzed 67 earthquakes recorded between November 2009 and September 2011 in a 43.5-mile (70 kilometers) grid covering northern Texas’ Barnett Shale formation. He found that all 24 of the earthquakes with the most reliably located epicenters originated within 2 miles (3.2 km) of one or more injection wells for wastewater disposal.

The injection well just south of DFW airport has been out of use since September 2011, according to Frohlich, but he says that doesn’t rule it out as a cause of the weekend’s quakes. He explained that, though water is no longer being added, lingering pressure differences from wastewater injection could still be contributing to the lubrication of long-stuck faults.

“Faults are everywhere. A lot of them are stuck, but if you pump water in there, it reduces friction and the fault slips a little,” Frohlich told Life’s Little Mysteries. “I can’t prove that that’s what happened, but it’s a plausible explanation.”

Heckmann Corporation (HEK) operates as a services-based company focused on total water and wastewater solutions for shale or unconventional oil and gas exploration and production. The company offers water delivery and disposal, trucking, fluids handling, treatment, temporary and permanent pipeline facilities, and water infrastructure services for oil and gas exploration and production companies. It operates multi-modal water disposal, treatment, trucking, and pipeline transportation operations in select shale areas in the United States, including the Eagle Ford, Haynesville, Marcellus, Utica, Barnett, and Tuscaloosa Marine Shale areas

If a definitve link between the Dallas earthquakes and fracking is established I see two possible outcomes. The first is a moratorium on fracking. This doesn’t seem likely given the strong push for energy independence and overall fragile state of the economy. The second scenario is regulation that the water used in the fracking process must be thoroughy cleaned and used at / or transported to ground level.

Fly’s post this morning got me laughing so composed a little song to go along with it 🙂

Fly’s post this morning got me laughing so composed a little song to go along with it 🙂

Tax bucks for iphones

Dial for crack

From the unemployment line

Taxes grant your wish

Take if from the rich

All they can do is bitch

But now Romney in my way

Food Stamps you holding

Might include some clothing

Air Jordans blowing

Electing soon now baby

All kind of free stuff,

and it ain’t crazy

Start with a free phone

Vote for me maybe?

Get to the clinic

If you have scabies

And here’s a free phone,

Vote for me maybe?

We are a gullible culture. Whether it’s the internet telling you that vaccinating your children causes autism or commercials convincing you that Enzyte will turn you into John Holmes, no one has ever gone broke underestimating the intelligence of the American public.

Now the curtain has been pulled back on another steaming pile of bullshit designed to separate you from your money – organic foods. A study just published in the Annals of Internal Medicine concludes there is no evidence “organically grown” fruits, veggies or meat are any more nutritious than the regular stuff you get off the shelves at your local supermarket.

Organic Food is more expensive because you believe it is healthier. And when you believe that, you subconsciously will believe it tastes better. Even if you couldnt pick the organic product in a blind taste test:

Which brings me to Whole Foods (WFM) – the Wall Street growth darling that’s just off it’s 52 week and all time highs. WFM is typically 15%-30% higher than your local supermarket. Food prices are already skyrocketing due to the drought. Add in the sheer brilliance of using 40% of the corn crop to produce ethanol and I believe there is a perfect storm brewing on the horizon for Whole Foods.

It won’t happen overnight – the last big hit to WFM was during the 2008 recession when the stock dropped 77% . A good indicator their top is coming will be when same store sales growth starts to tank. Current guidance for Fiscal year 2012 sales growth is 15.6%-15.8%, while same store sales growth for 2012 is 8.6%-8.8% – so far they are hitting their targets.

For me the question is how long until their customer base wakes up and realizes they have been overpaying for a lie

Did anyone really think Austerity would work?

In this New York Times article US companies reveal contingency plans for the inevitable removal of Greece from the Eurozone

Even as Greece desperately tries to avoid defaulting on its debt, American companies are preparing for what was once unthinkable: that Greece could soon be forced to leave the euro zone.

Bank of America Merrill Lynch has looked into filling trucks with cash and sending them over the Greek border so clients can continue to pay local employees and suppliers in the event money is unavailable. Ford has configured its computer systems so they will be able to immediately handle a new Greek currency.

No one knows just how broad the shock waves from a Greek exit would be, but big American banks and consulting firms have also been doing a brisk business advising their corporate clients on how to prepare for a splintering of the euro zone.

That is a striking contrast to the assurances from European politicians that the crisis is manageable and that the currency union can be held together. On Thursday, the European Central Bank will consider measures that would ease pressure on Europe’s cash-starved countries.

JPMorgan Chase, though, is taking no chances. It has already created new accounts for a handful of American giants that are reserved for a new drachma in Greece or whatever currency might succeed the euro in other countries.

Stock markets around the world have rallied this summer on hopes that European leaders will solve the Continent’s debt problems, but the quickening tempo of preparations by big business for a potential Greek exit this summer suggests that investors may be unduly optimistic. Many executives are deeply skeptical that Greece will accede to the austere fiscal policies being demanded by Europe in return for financial assistance.

Greece’s abandonment of the euro would most likely create turmoil in global markets, which have experienced periodic sell-offs whenever Europe’s debt problems have flared up over the last two and a half years. It would also increase the pressure on Italy and Spain, much larger economic powers that are struggling with debt problems of their own.“It’s safe to say most companies are preparing,” said Paul Dennis, a program manager with Corporate Executive Board, a private advisory firm.

In a survey this summer, the firm found that 80 percent of clients polled expected Greece to leave the euro zone, and a fifth of those expected more countries to follow.

“Fifteen months ago when we started looking at this, we said it was unthinkable,” said Heiner Leisten, a partner with the Boston Consulting Group in Cologne, Germany, who heads up its global insurance practice. “It’s not impossible or unthinkable now.”

Mr. Leisten’s firm, as well as PricewaterhouseCoopers, has already considered the timing of a Greek withdrawal — for example, the news might hit on a Friday night, when global markets are closed.

A bank holiday could quickly follow, with the stock market and most local financial institutions shutting down, while new capital controls make it hard to move money in and out of the country.

“We’ve had conversations with several dozen companies and we’re doing work for a number of these,” said Peter Frank, who advises corporate treasurers as a principal at Pricewaterhouse. “Almost all of that has come in over the transom in the last 90 days.”

He added: “Companies are asking some very granular questions, like ‘If a news release comes out on a Friday night announcing that Greece has pulled out of the euro, what do we do?’ In some cases, companies have contingency plans in place, such as having someone take a train to Athens with 50,000 euros to pay employees.”

The recent wave of preparations by American companies for a Greek exit from the euro signals a stark switch from their stance in the past, said Carole Berndt, head of global transaction services in Europe, the Middle East and Africa for Bank of America Merrill Lynch.

“When we started giving advice, they came for the free sandwiches and chocolate cookies,” she said jokingly. “Now that has changed, and contingency planning is focused on three primary scenarios — a single-country exit, a multicountry exit and a breakup of the euro zone in its entirety.”

Banks and consulting firms are reluctant to name clients, and many big companies also declined to discuss their contingency plans, fearing it could anger customers in Europe if it became known they were contemplating the euro’s demise.

Central banks, as well as Germany’s finance ministry, have also been considering the implications of a Greek exit but have been even more secretive about specific plans.

But some corporations are beginning to acknowledge they are ready if Greece or even additional countries leave the euro zone, making sure systems can handle a quick transition to a new currency.

In Europe, the holding company for Iberia Airlines and British Airways has acknowledged it is preparing plans in the event of a euro exit by Spain.

“We’ve looked at many scenarios, including where one or more countries decides to redenominate,” said Roger Griffith, who oversees global settlement and customer risk for MasterCard. “We have defined operating steps and communications steps to take.” He added: “Practically, we could make a change in a day or two and be prepared in terms of our systems.”

In a statement, Visa said that it too would also be able to make “a swift transition to a new currency with the minimum possible disruption to consumers and retailers.”

Juniper Networks, a provider of networking technology based in California, created a “Euro Zone Crisis Assessment and Contingency Plan,” which company officials liken to the kind of business continuity plans they maintain in the event of an earthquake.

“It’s about having an awareness versus having to scramble,” said Catherine Portman, vice president for treasury at Juniper. The company has already begun moving funds in euro zone banks to accounts elsewhere more frequently, while making sure it has adequate money and liquidity in place so employees and suppliers are paid without disruption.

FMC, a chemical giant based in Philadelphia, is asking some Greek customers to pay in advance, rather than risk selling to them now and not getting paid later. It has also begun to avoid keeping any excess cash in Greek, Spanish or Italian bank accounts, while carefully monitoring the creditworthiness of customers in those countries.

“It’s been a very hot topic,” said Thomas C. Deas Jr., an FMC executive who serves as chairman of the National Association of Corporate Treasurers. Members of his group discussed the issue on a conference call last Tuesday, he added.

American companies have actually been more aggressive about seeking out advice than their European counterparts, according to John Gibbons, head of treasury services in Europe for JPMorgan Chase.

Mr. Gibbons said a handful of the largest American companies had requested the special accounts configured for a currency that did not yet exist.

“We’re planning against the extreme,” he said. “You don’t lose anything by doing it.”

WASHINGTON (MarketWatch) — The following is the text of Federal Reserve Chairman Ben Bernanke’s speech at Jackson Hole, as prepared for delivery:

“When we convened in Jackson Hole in August 2007, the Federal Open Market Committee’s (FOMC) target for the federal funds rate was 5-1/4 percent. Sixteen months later, with the financial crisis in full swing, the FOMC had lowered the target for the federal funds rate to nearly zero, thereby entering the unfamiliar territory of having to conduct monetary policy with the policy interest rate at its effective lower bound. The unusual severity of the recession and ongoing strains in financial markets made the challenges facing monetary policymakers all the greater.

Today I will review the evolution of U.S. monetary policy since late 2007. My focus will be the Federal Reserve’s experience with nontraditional policy tools, notably those based on the management of the Federal Reserve’s balance sheet and on its public communications. I’ll discuss what we have learned about the efficacy and drawbacks of these less familiar forms of monetary policy, and I’ll talk about the implications for the Federal Reserve’s ongoing efforts to promote a return to maximum employment in a context of price stability.

Monetary Policy in 2007 and 2008

When significant financial stresses first emerged, in August 2007, the FOMC responded quickly, first through liquidity actions–cutting the discount rate and extending term loans to banks–and then, in September, by lowering the target for the federal funds rate by 50 basis points. 1 As further indications of economic weakness appeared over subsequent months, the Committee reduced its target for the federal funds rate by a cumulative 325 basis points, leaving the target at 2 percent by the spring of 2008.

The Committee held rates constant over the summer as it monitored economic and financial conditions. When the crisis intensified markedly in the fall, the Committee responded by cutting the target for the federal funds rate by 100 basis points in October, with half of this easing coming as part of an unprecedented coordinated interest rate cut by six major central banks. Then, in December 2008, as evidence of a dramatic slowdown mounted, the Committee reduced its target to a range of 0 to 25 basis points, effectively its lower bound. That target range remains in place today.

Despite the easing of monetary policy, dysfunction in credit markets continued to worsen. As you know, in the latter part of 2008 and early 2009, the Federal Reserve took extraordinary steps to provide liquidity and support credit market functioning, including the establishment of a number of emergency lending facilities and the creation or extension of currency swap agreements with 14 central banks around the world.2 In its role as banking regulator, the Federal Reserve also led stress tests of the largest U.S. bank holding companies, setting the stage for the companies to raise capital. These actions–along with a host of interventions by other policymakers in the United States and throughout the world–helped stabilize global financial markets, which in turn served to check the deterioration in the real economy and the emergence of deflationary pressures.

Unfortunately, although it is likely that even worse outcomes had been averted, the damage to the economy was severe. The unemployment rate in the United States rose from about 6 percent in September 2008 to nearly 9 percent by April 2009–it would peak at 10 percent in October–while inflation declined sharply. As the crisis crested, and with the federal funds rate at its effective lower bound, the FOMC turned to nontraditional policy approaches to support the recovery.

As the Committee embarked on this path, we were guided by some general principles and some insightful academic work but–with the important exception of the Japanese case–limited historical experience. As a result, central bankers in the United States, and those in other advanced economies facing similar problems, have been in the process of learning by doing. I will discuss some of what we have learned, beginning with our experience conducting policy using the Federal Reserve’s balance sheet, then turn to our use of communications tools.

Balance Sheet Tools

In using the Federal Reserve’s balance sheet as a tool for achieving its mandated objectives of maximum employment and price stability, the FOMC has focused on the acquisition of longer-term securities–specifically, Treasury and agency securities, which are the principal types of securities that the Federal Reserve is permitted to buy under the Federal Reserve Act.3 One mechanism through which such purchases are believed to affect the economy is the so-called portfolio balance channel, which is based on the ideas of a number of well-known monetary economists, including James Tobin, Milton Friedman, Franco Modigliani, Karl Brunner, and Allan Meltzer. The key premise underlying this channel is that, for a variety of reasons, different classes of financial assets are not perfect substitutes in investors’ portfolios.4 For example, some institutional investors face regulatory restrictions on the types of securities they can hold, retail investors may be reluctant to hold certain types of assets because of high transactions or information costs, and some assets have risk characteristics that are difficult or costly to hedge.

Imperfect substitutability of assets implies that changes in the supplies of various assets available to private investors may affect the prices and yields of those assets. Thus, Federal Reserve purchases of mortgage-backed securities (MBS), for example, should raise the prices and lower the yields of those securities; moreover, as investors rebalance their portfolios by replacing the MBS sold to the Federal Reserve with other assets, the prices of the assets they buy should rise and their yields decline as well. Declining yields and rising asset prices ease overall financial conditions and stimulate economic activity through channels similar to those for conventional monetary policy. Following this logic, Tobin suggested that purchases of longer-term securities by the Federal Reserve during the Great Depression could have helped the U.S. economy recover despite the fact that short-term rates were close to zero, and Friedman argued for large-scale purchases of long-term bonds by the Bank of Japan to help overcome Japan’s deflationary trap.5

Large-scale asset purchases can influence financial conditions and the broader economy through other channels as well. For instance, they can signal that the central bank intends to pursue a persistently more accommodative policy stance than previously thought, thereby lowering investors’ expectations for the future path of the federal funds rate and putting additional downward pressure on long-term interest rates, particularly in real terms. Such signaling can also increase household and business confidence by helping to diminish concerns about “tail” risks such as deflation. During stressful periods, asset purchases may also improve the functioning of financial markets, thereby easing credit conditions in some sectors.

With the space for further cuts in the target for the federal funds rate increasingly limited, in late 2008 the Federal Reserve initiated a series of large-scale asset purchases (LSAPs). In November, the FOMC announced a program to purchase a total of $600 billion in agency MBS and agency debt.6 In March 2009, the FOMC expanded this purchase program substantially, announcing that it would purchase up to $1.25 trillion of agency MBS, up to $200 billion of agency debt, and up to $300 billion of longer-term Treasury debt.7 These purchases were completed, with minor adjustments, in early 2010.8 In November 2010, the FOMC announced that it would further expand the Federal Reserve’s security holdings by purchasing an additional $600 billion of longer-term Treasury securities over a period ending in mid-2011.9

About a year ago, the FOMC introduced a variation on its earlier purchase programs, known as the maturity extension program (MEP), under which the Federal Reserve would purchase $400 billion of long-term Treasury securities and sell an equivalent amount of shorter-term Treasury securities over the period ending in June 2012.10 The FOMC subsequently extended the MEP through the end of this year.11 By reducing the average maturity of the securities held by the public, the MEP puts additional downward pressure on longer-term interest rates and further eases overall financial conditions.

How effective are balance sheet policies? After nearly four years of experience with large-scale asset purchases, a substantial body of empirical work on their effects has emerged. Generally, this research finds that the Federal Reserve’s large-scale purchases have significantly lowered long-term Treasury yields. For example, studies have found that the $1.7 trillion in purchases of Treasury and agency securities under the first LSAP program reduced the yield on 10-year Treasury securities by between 40 and 110 basis points. The $600 billion in Treasury purchases under the second LSAP program has been credited with lowering 10-year yields by an additional 15 to 45 basis points.12 Three studies considering the cumulative influence of all the Federal Reserve’s asset purchases, including those made under the MEP, found total effects between 80 and 120 basis points on the 10-year Treasury yield.13 These effects are economically meaningful.

Importantly, the effects of LSAPs do not appear to be confined to longer-term Treasury yields. Notably, LSAPs have been found to be associated with significant declines in the yields on both corporate bonds and MBS.14 The first purchase program, in particular, has been linked to substantial reductions in MBS yields and retail mortgage rates. LSAPs also appear to have boosted stock prices, presumably both by lowering discount rates and by improving the economic outlook; it is probably not a coincidence that the sustained recovery in U.S. equity prices began in March 2009, shortly after the FOMC’s decision to greatly expand securities purchases. This effect is potentially important because stock values affect both consumption and investment decisions.

While there is substantial evidence that the Federal Reserve’s asset purchases have lowered longer-term yields and eased broader financial conditions, obtaining precise estimates of the effects of these operations on the broader economy is inherently difficult, as the counterfactual–how the economy would have performed in the absence of the Federal Reserve’s actions–cannot be directly observed. If we are willing to take as a working assumption that the effects of easier financial conditions on the economy are similar to those observed historically, then econometric models can be used to estimate the effects of LSAPs on the economy. Model simulations conducted at the Federal Reserve generally find that the securities purchase programs have provided significant help for the economy. For example, a study using the Board’s FRB/US model of the economy found that, as of 2012, the first two rounds of LSAPs may have raised the level of output by almost 3 percent and increased private payroll employment by more than 2 million jobs, relative to what otherwise would have occurred.15 The Bank of England has used LSAPs in a manner similar to that of the Federal Reserve, so it is of interest that researchers have found the financial and macroeconomic effects of the British programs to be qualitatively similar to those in the United States.16

To be sure, these estimates of the macroeconomic effects of LSAPs should be treated with caution. It is likely that the crisis and the recession have attenuated some of the normal transmission channels of monetary policy relative to what is assumed in the models; for example, restrictive mortgage underwriting standards have reduced the effects of lower mortgage rates. Further, the estimated macroeconomic effects depend on uncertain estimates of the persistence of the effects of LSAPs on financial conditions.17 Overall, however, a balanced reading of the evidence supports the conclusion that central bank securities purchases have provided meaningful support to the economic recovery while mitigating deflationary risks.

Now I will turn to our use of communications tools.

Communication Tools

Clear communication is always important in central banking, but it can be especially important when economic conditions call for further policy stimulus but the policy rate is already at its effective lower bound. In particular, forward guidance that lowers private-sector expectations regarding future short-term rates should cause longer-term interest rates to decline, leading to more accommodative financial conditions.18

The Federal Reserve has made considerable use of forward guidance as a policy tool.19 From March 2009 through June 2011, the FOMC’s postmeeting statement noted that economic conditions “are likely to warrant exceptionally low levels of the federal funds rate for an extended period.”20 At the August 2011 meeting, the Committee made its guidance more precise by stating that economic conditions would likely warrant that the federal funds rate remain exceptionally low “at least through mid-2013.”21 At the beginning of this year, the FOMC extended the anticipated period of exceptionally low rates further, to “at least through late 2014,” guidance that has been reaffirmed at subsequent meetings.22 As the language indicates, this guidance is not an unconditional promise; rather, it is a statement about the FOMC’s collective judgment regarding the path of policy that is likely to prove appropriate, given the Committee’s objectives and its outlook for the economy.

The views of Committee members regarding the likely timing of policy firming represent a balance of many factors, but the current forward guidance is broadly consistent with prescriptions coming from a range of standard benchmarks, including simple policy rules and optimal control methods.23 Some of the policy rules informing the forward guidance relate policy interest rates to familiar determinants, such as inflation and the output gap. But a number of considerations also argue for planning to keep rates low for a longer time than implied by policy rules developed during more normal periods. These considerations include the need to take out insurance against the realization of downside risks, which are particularly difficult to manage when rates are close to their effective lower bound; the possibility that, because of various unusual headwinds slowing the recovery, the economy needs more policy support than usual at this stage of the cycle; and the need to compensate for limits to policy accommodation resulting from the lower bound on rates.24

Has the forward guidance been effective? It is certainly true that, over time, both investors and private forecasters have pushed out considerably the date at which they expect the federal funds rate to begin to rise; moreover, current policy expectations appear to align well with the FOMC’s forward guidance. To be sure, the changes over time in when the private sector expects the federal funds rate to begin firming resulted in part from the same deterioration of the economic outlook that led the FOMC to introduce and then extend its forward guidance. But the private sector’s revised outlook for the policy rate also appears to reflect a growing appreciation of how forceful the FOMC intends to be in supporting a sustainable recovery. For example, since 2009, forecasters participating in the Blue Chip survey have repeatedly marked down their projections of the unemployment rate they expect to prevail at the time that the FOMC begins to lift the target for the federal funds rate away from zero. Thus, the Committee’s forward guidance may have conveyed a greater willingness to maintain accommodation than private forecasters had previously believed.25 The behavior of financial market prices in periods around changes in the forward guidance is also consistent with the view that the guidance has affected policy expectations.26

Making Policy with Nontraditional Tools: A Cost-Benefit Framework

Making monetary policy with nontraditional tools is challenging. In particular, our experience with these tools remains limited. In this context, the FOMC carefully compares the expected benefits and costs of proposed policy actions.

The potential benefit of policy action, of course, is the possibility of better economic outcomes–outcomes more consistent with the FOMC’s dual mandate. In light of the evidence I discussed, it appears reasonable to conclude that nontraditional policy tools have been and can continue to be effective in providing financial accommodation, though we are less certain about the magnitude and persistence of these effects than we are about those of more-traditional policies.

The possible benefits of an action, however, must be considered alongside its potential costs. I will focus now on the potential costs of LSAPs.

One possible cost of conducting additional LSAPs is that these operations could impair the functioning of securities markets. As I noted, the Federal Reserve is limited by law mainly to the purchase of Treasury and agency securities; the supply of those securities is large but finite, and not all of the supply is actively traded. Conceivably, if the Federal Reserve became too dominant a buyer in certain segments of these markets, trading among private agents could dry up, degrading liquidity and price discovery. As the global financial system depends on deep and liquid markets for U.S. Treasury securities, significant impairment of those markets would be costly, and, in particular, could impede the transmission of monetary policy. For example, market disruptions could lead to higher liquidity premiums on Treasury securities, which would run counter to the policy goal of reducing Treasury yields. However, although market capacity could ultimately become an issue, to this point we have seen few if any problems in the markets for Treasury or agency securities, private-sector holdings of securities remain large, and trading among private market participants remains robust.

A second potential cost of additional securities purchases is that substantial further expansions of the balance sheet could reduce public confidence in the Fed’s ability to exit smoothly from its accommodative policies at the appropriate time. Even if unjustified, such a reduction in confidence might increase the risk of a costly unanchoring of inflation expectations, leading in turn to financial and economic instability. It is noteworthy, however, that the expansion of the balance sheet to date has not materially affected inflation expectations, likely in part because of the great emphasis the Federal Reserve has placed on developing tools to ensure that we can normalize monetary policy when appropriate, even if our securities holdings remain large. In particular, the FOMC will be able to put upward pressure on short-term interest rates by raising the interest rate it pays banks for reserves they hold at the Fed. Upward pressure on rates can also be achieved by using reserve-draining tools or by selling securities from the Federal Reserve’s portfolio, thus reversing the effects achieved by LSAPs. The FOMC has spent considerable effort planning and testing our exit strategy and will act decisively to execute it at the appropriate time.

A third cost to be weighed is that of risks to financial stability. For example, some observers have raised concerns that, by driving longer-term yields lower, nontraditional policies could induce an imprudent reach for yield by some investors and thereby threaten financial stability. Of course, one objective of both traditional and nontraditional policy during recoveries is to promote a return to productive risk-taking; as always, the goal is to strike the appropriate balance. Moreover, a stronger recovery is itself clearly helpful for financial stability. In assessing this risk, it is important to note that the Federal Reserve, both on its own and in collaboration with other members of the Financial Stability Oversight Council, has substantially expanded its monitoring of the financial system and modified its supervisory approach to take a more systemic perspective. We have seen little evidence thus far of unsafe buildups of risk or leverage, but we will continue both our careful oversight and the implementation of financial regulatory reforms aimed at reducing systemic risk.

A fourth potential cost of balance sheet policies is the possibility that the Federal Reserve could incur financial losses should interest rates rise to an unexpected extent. Extensive analyses suggest that, from a purely fiscal perspective, the odds are strong that the Fed’s asset purchases will make money for the taxpayers, reducing the federal deficit and debt.27 And, of course, to the extent that monetary policy helps strengthen the economy and raise incomes, the benefits for the U.S. fiscal position would be substantial. In any case, this purely fiscal perspective is too narrow: Because Americans are workers and consumers as well as taxpayers, monetary policy can achieve the most for the country by focusing generally on improving economic performance rather than narrowly on possible gains or losses on the Federal Reserve’s balance sheet.

In sum, both the benefits and costs of nontraditional monetary policies are uncertain; in all likelihood, they will also vary over time, depending on factors such as the state of the economy and financial markets and the extent of prior Federal Reserve asset purchases. Moreover, nontraditional policies have potential costs that may be less relevant for traditional policies. For these reasons, the hurdle for using nontraditional policies should be higher than for traditional policies. At the same time, the costs of nontraditional policies, when considered carefully, appear manageable, implying that we should not rule out the further use of such policies if economic conditions warrant.

Economic Prospects

The accommodative monetary policies I have reviewed today, both traditional and nontraditional, have provided important support to the economic recovery while helping to maintain price stability. As of July, the unemployment rate had fallen to 8.3 percent from its cyclical peak of 10 percent and payrolls had risen by 4 million jobs from their low point. And despite periodic concerns about deflation risks, on the one hand, and repeated warnings that excessive policy accommodation would ignite inflation, on the other hand, inflation (except for temporary deviations caused primarily by swings in commodity prices) has remained near the Committee’s 2 percent objective and inflation expectations have remained stable. Key sectors such as manufacturing, housing, and international trade have strengthened, firms’ investment in equipment and software has rebounded, and conditions in financial and credit markets have improved.

Notwithstanding these positive signs, the economic situation is obviously far from satisfactory. The unemployment rate remains more than 2 percentage points above what most FOMC participants see as its longer-run normal value, and other indicators–such as the labor force participation rate and the number of people working part time for economic reasons–confirm that labor force utilization remains at very low levels. Further, the rate of improvement in the labor market has been painfully slow. I have noted on other occasions that the declines in unemployment we have seen would likely continue only if economic growth picked up to a rate above its longer-term trend.28 In fact, growth in recent quarters has been tepid, and so, not surprisingly, we have seen no net improvement in the unemployment rate since January. Unless the economy begins to grow more quickly than it has recently, the unemployment rate is likely to remain far above levels consistent with maximum employment for some time.

In light of the policy actions the FOMC has taken to date, as well as the economy’s natural recovery mechanisms, we might have hoped for greater progress by now in returning to maximum employment. Some have taken the lack of progress as evidence that the financial crisis caused structural damage to the economy, rendering the current levels of unemployment impervious to additional monetary accommodation. The literature on this issue is extensive, and I cannot fully review it today.29 However, following every previous U.S. recession since World War II, the unemployment rate has returned close to its pre-recession level, and, although the recent recession was unusually deep, I see little evidence of substantial structural change in recent years.

Rather than attributing the slow recovery to longer-term structural factors, I see growth being held back currently by a number of headwinds. First, although the housing sector has shown signs of improvement, housing activity remains at low levels and is contributing much less to the recovery than would normally be expected at this stage of the cycle.

Second, fiscal policy, at both the federal and state and local levels, has become an important headwind for the pace of economic growth. Notwithstanding some recent improvement in tax revenues, state and local governments still face tight budget situations and continue to cut real spending and employment. Real purchases are also declining at the federal level. Uncertainties about fiscal policy, notably about the resolution of the so-called fiscal cliff and the lifting of the debt ceiling, are probably also restraining activity, although the magnitudes of these effects are hard to judge.30 It is critical that fiscal policymakers put in place a credible plan that sets the federal budget on a sustainable trajectory in the medium and longer runs. However, policymakers should take care to avoid a sharp near-term fiscal contraction that could endanger the recovery.

Third, stresses in credit and financial markets continue to restrain the economy. Earlier in the recovery, limited credit availability was an important factor holding back growth, and tight borrowing conditions for some potential homebuyers and small businesses remain a problem today. More recently, however, a major source of financial strains has been uncertainty about developments in Europe. These strains are most problematic for the Europeans, of course, but through global trade and financial linkages, the effects of the European situation on the U.S. economy are significant as well. Some recent policy proposals in Europe have been quite constructive, in my view, and I urge our European colleagues to press ahead with policy initiatives to resolve the crisis.

Conclusion

Early in my tenure as a member of the Board of Governors, I gave a speech that considered options for monetary policy when the short-term policy interest rate is close to its effective lower bound.31 I was reacting to common assertions at the time that monetary policymakers would be “out of ammunition” as the federal funds rate came closer to zero. I argued that, to the contrary, policy could still be effective near the lower bound. Now, with several years of experience with nontraditional policies both in the United States and in other advanced economies, we know more about how such policies work. It seems clear, based on this experience, that such policies can be effective, and that, in their absence, the 2007-09 recession would have been deeper and the current recovery would have been slower than has actually occurred.

As I have discussed today, it is also true that nontraditional policies are relatively more difficult to apply, at least given the present state of our knowledge. Estimates of the effects of nontraditional policies on economic activity and inflation are uncertain, and the use of nontraditional policies involves costs beyond those generally associated with more-standard policies. Consequently, the bar for the use of nontraditional policies is higher than for traditional policies. In addition, in the present context, nontraditional policies share the limitations of monetary policy more generally: Monetary policy cannot achieve by itself what a broader and more balanced set of economic policies might achieve; in particular, it cannot neutralize the fiscal and financial risks that the country faces. It certainly cannot fine-tune economic outcomes.

As we assess the benefits and costs of alternative policy approaches, though, we must not lose sight of the daunting economic challenges that confront our nation. The stagnation of the labor market in particular is a grave concern not only because of the enormous suffering and waste of human talent it entails, but also because persistently high levels of unemployment will wreak structural damage on our economy that could last for many years.

Over the past five years, the Federal Reserve has acted to support economic growth and foster job creation, and it is important to achieve further progress, particularly in the labor market. Taking due account of the uncertainties and limits of its policy tools, the Federal Reserve will provide additional policy accommodation as needed to promote a stronger economic recovery and sustained improvement in labor market conditions in a context of price stability.”

is called pheed and Forbes thinks it might be

Think of it as twitter with a business plan and Facebook without all the noise.

Hit me up at:

VVUS Pharmaceuticals – their claim to fame has been a much hyped wight loss drug Qsvia.

Too bad it was just rejected for sale Europe

5:31PM Vivus receives formal decision from CHMP: the CHMP recommended against approval of Qsiva as expected (VVUS) 21.06 -1.24 : Co announced that is has received the formal opinion from the European Medicines Agency’s (EMA) Committee for Medicinal Products for Human Use (CHMP) following their October 15-18 meeting. As expected, the CHMP recommended against approval of the Marketing Authorization Application (MAA) for Qsiva (phentermine/topiramate ER) for the treatment of obesity in the European Union. The reasons for their decision were due to concerns over the potential cardiovascular and central nervous system effects associated with long-term use, teratogenic potential and use by patients for whom Qsiva is not indicated. The company currently intends to appeal this opinion and request a re-examination of the decision by the CHMP. “The lack of effective pharmacologic treatments for obesity remains a high medical need for many patients in Europe,” stated Peter Tam, VIVUS’ president. “We are committed to getting Qsiva approved in Europe and will work closely with the new rapporteur and co-rapporteur to make this happen.”

In after hours trading the stock is down to $20.55 on the bid / $20.95 on the ask. This is after declining 5.5% ($1.24) today

Looking at the chart you can see they are headed back to the pivot tomorrow and in high probablilty the recent swing low at $17.21. If that happens to break – it’s a long way down to fill the gap

Right here – Right now.

We wither break the trendline from the June 9 lows or we go higher.

RSI and MACD both say it’s headed south

Jack Welch was spot on regarding his skepticism of today’s jobs report.

What the report didn’t tell you was that 342,000 Americans dropped out of the workforce.

This article from UPI sums it up pretty well:

The Labor Department report said 12.1 million people were unemployed, a drop of 456,000 from the previous month.

That figure is critical because 342,000 more people dropped out of the workforce than gained employment in September. The September rate fell to 7.8 percent in part because it reflected an increase in the number of jobs initially reported in July and August.

Although the number is officially described as representing people who elected to care for a relative at home or return to school, many did so because they were simply too discouraged to continue looking for work.

So what is the ‘real” unemployment number for our country? It’s a guesstimate at best as there’s no way to measure all those who have run out of unemployment benefits and stopped looking for work all together. The Romney camp estimates the true number to be closer to 11%. They arrive at that figure by by applying the labor force participation rate from when Obama took office to today’s population:

“The labor force participation rate in January 2009 was 65.7 percent,” Williams said. Since then, the rate has fallen to 63.3 percent. “Had the rate remained the same, the labor force would be about 160,158,000. At that labor force level, the unemployment rate would be 10.7 percent.”

As noted in this article, though, it’s also impossible to guage the number of retirees during the recession. This was documented in this report by the Chicago branch of the Federal reserve.

What is clear is that this 7.8% number will be put out to the electorate as a sign of recovery. I’ll expect to hear it in the upcoming debates. The headlines and pundits have filled the web with it today

To that I’ll simply ask “then why didn’t the markets explode today?”

I’ve been neutral about the Presidential race up until now, as neither candidate represents what I’m looking for in a leader. I’ve also resisted most of the tin foil hat conspiracy theories and muck slinging.

But when something this blatant is put forth as this- it compels me to choose the lesser of two evils.

According to Cliff Frohlich, associate director and senior research scientist at the University of Texas at Austin’s Institute for Geophysics, the earthquakes that occured this past weekend near Dallas appear to be connected to the past disposal of wastewater from local hydraulic fracturing operations.

During hydraulic fracturing, or “fracking,” millions of gallons of high-pressure, chemical-laden water are pumped into an underground geologic formation (the Barnett Shale, in the case of northern Texas) to free up oil. But once fractures have been opened up in the rock and the water pressure is allowed to abate, internal pressure from the rock causes fracking fluids to rise back to the surface, becoming what the natural gas industry calls “flowback,” according to the Environmental Protection Agency.

“That’s dirty water you have to get rid of,” said Frohlich. “One way people do that is to pump it back into the ground.”

In a study he recently published in the journal Proceedings of the National Academy of Sciences, Frohlich analyzed 67 earthquakes recorded between November 2009 and September 2011 in a 43.5-mile (70 kilometers) grid covering northern Texas’ Barnett Shale formation. He found that all 24 of the earthquakes with the most reliably located epicenters originated within 2 miles (3.2 km) of one or more injection wells for wastewater disposal.

The injection well just south of DFW airport has been out of use since September 2011, according to Frohlich, but he says that doesn’t rule it out as a cause of the weekend’s quakes. He explained that, though water is no longer being added, lingering pressure differences from wastewater injection could still be contributing to the lubrication of long-stuck faults.

“Faults are everywhere. A lot of them are stuck, but if you pump water in there, it reduces friction and the fault slips a little,” Frohlich told Life’s Little Mysteries. “I can’t prove that that’s what happened, but it’s a plausible explanation.”

Heckmann Corporation (HEK) operates as a services-based company focused on total water and wastewater solutions for shale or unconventional oil and gas exploration and production. The company offers water delivery and disposal, trucking, fluids handling, treatment, temporary and permanent pipeline facilities, and water infrastructure services for oil and gas exploration and production companies. It operates multi-modal water disposal, treatment, trucking, and pipeline transportation operations in select shale areas in the United States, including the Eagle Ford, Haynesville, Marcellus, Utica, Barnett, and Tuscaloosa Marine Shale areas

If a definitve link between the Dallas earthquakes and fracking is established I see two possible outcomes. The first is a moratorium on fracking. This doesn’t seem likely given the strong push for energy independence and overall fragile state of the economy. The second scenario is regulation that the water used in the fracking process must be thoroughy cleaned and used at / or transported to ground level.

Fly’s post this morning got me laughing so composed a little song to go along with it 🙂

Tax bucks for iphones

Dial for crack

From the unemployment line

Taxes grant your wish

Take if from the rich

All they can do is bitch

But now Romney in my way

Food Stamps you holding

Might include some clothing

Air Jordans blowing

Electing soon now baby

All kind of free stuff,

and it ain’t crazy

Start with a free phone

Vote for me maybe?

Get to the clinic

If you have scabies

And here’s a free phone,

Vote for me maybe?

We are a gullible culture. Whether it’s the internet telling you that vaccinating your children causes autism or commercials convincing you that Enzyte will turn you into John Holmes, no one has ever gone broke underestimating the intelligence of the American public.

Now the curtain has been pulled back on another steaming pile of bullshit designed to separate you from your money – organic foods. A study just published in the Annals of Internal Medicine concludes there is no evidence “organically grown” fruits, veggies or meat are any more nutritious than the regular stuff you get off the shelves at your local supermarket.

Organic Food is more expensive because you believe it is healthier. And when you believe that, you subconsciously will believe it tastes better. Even if you couldnt pick the organic product in a blind taste test:

Which brings me to Whole Foods (WFM) – the Wall Street growth darling that’s just off it’s 52 week and all time highs. WFM is typically 15%-30% higher than your local supermarket. Food prices are already skyrocketing due to the drought. Add in the sheer brilliance of using 40% of the corn crop to produce ethanol and I believe there is a perfect storm brewing on the horizon for Whole Foods.

It won’t happen overnight – the last big hit to WFM was during the 2008 recession when the stock dropped 77% . A good indicator their top is coming will be when same store sales growth starts to tank. Current guidance for Fiscal year 2012 sales growth is 15.6%-15.8%, while same store sales growth for 2012 is 8.6%-8.8% – so far they are hitting their targets.

For me the question is how long until their customer base wakes up and realizes they have been overpaying for a lie

Did anyone really think Austerity would work?

In this New York Times article US companies reveal contingency plans for the inevitable removal of Greece from the Eurozone

Even as Greece desperately tries to avoid defaulting on its debt, American companies are preparing for what was once unthinkable: that Greece could soon be forced to leave the euro zone.

Bank of America Merrill Lynch has looked into filling trucks with cash and sending them over the Greek border so clients can continue to pay local employees and suppliers in the event money is unavailable. Ford has configured its computer systems so they will be able to immediately handle a new Greek currency.

No one knows just how broad the shock waves from a Greek exit would be, but big American banks and consulting firms have also been doing a brisk business advising their corporate clients on how to prepare for a splintering of the euro zone.

That is a striking contrast to the assurances from European politicians that the crisis is manageable and that the currency union can be held together. On Thursday, the European Central Bank will consider measures that would ease pressure on Europe’s cash-starved countries.

JPMorgan Chase, though, is taking no chances. It has already created new accounts for a handful of American giants that are reserved for a new drachma in Greece or whatever currency might succeed the euro in other countries.

Stock markets around the world have rallied this summer on hopes that European leaders will solve the Continent’s debt problems, but the quickening tempo of preparations by big business for a potential Greek exit this summer suggests that investors may be unduly optimistic. Many executives are deeply skeptical that Greece will accede to the austere fiscal policies being demanded by Europe in return for financial assistance.

Greece’s abandonment of the euro would most likely create turmoil in global markets, which have experienced periodic sell-offs whenever Europe’s debt problems have flared up over the last two and a half years. It would also increase the pressure on Italy and Spain, much larger economic powers that are struggling with debt problems of their own.“It’s safe to say most companies are preparing,” said Paul Dennis, a program manager with Corporate Executive Board, a private advisory firm.

In a survey this summer, the firm found that 80 percent of clients polled expected Greece to leave the euro zone, and a fifth of those expected more countries to follow.

“Fifteen months ago when we started looking at this, we said it was unthinkable,” said Heiner Leisten, a partner with the Boston Consulting Group in Cologne, Germany, who heads up its global insurance practice. “It’s not impossible or unthinkable now.”

Mr. Leisten’s firm, as well as PricewaterhouseCoopers, has already considered the timing of a Greek withdrawal — for example, the news might hit on a Friday night, when global markets are closed.

A bank holiday could quickly follow, with the stock market and most local financial institutions shutting down, while new capital controls make it hard to move money in and out of the country.

“We’ve had conversations with several dozen companies and we’re doing work for a number of these,” said Peter Frank, who advises corporate treasurers as a principal at Pricewaterhouse. “Almost all of that has come in over the transom in the last 90 days.”

He added: “Companies are asking some very granular questions, like ‘If a news release comes out on a Friday night announcing that Greece has pulled out of the euro, what do we do?’ In some cases, companies have contingency plans in place, such as having someone take a train to Athens with 50,000 euros to pay employees.”

The recent wave of preparations by American companies for a Greek exit from the euro signals a stark switch from their stance in the past, said Carole Berndt, head of global transaction services in Europe, the Middle East and Africa for Bank of America Merrill Lynch.

“When we started giving advice, they came for the free sandwiches and chocolate cookies,” she said jokingly. “Now that has changed, and contingency planning is focused on three primary scenarios — a single-country exit, a multicountry exit and a breakup of the euro zone in its entirety.”

Banks and consulting firms are reluctant to name clients, and many big companies also declined to discuss their contingency plans, fearing it could anger customers in Europe if it became known they were contemplating the euro’s demise.

Central banks, as well as Germany’s finance ministry, have also been considering the implications of a Greek exit but have been even more secretive about specific plans.

But some corporations are beginning to acknowledge they are ready if Greece or even additional countries leave the euro zone, making sure systems can handle a quick transition to a new currency.

In Europe, the holding company for Iberia Airlines and British Airways has acknowledged it is preparing plans in the event of a euro exit by Spain.

“We’ve looked at many scenarios, including where one or more countries decides to redenominate,” said Roger Griffith, who oversees global settlement and customer risk for MasterCard. “We have defined operating steps and communications steps to take.” He added: “Practically, we could make a change in a day or two and be prepared in terms of our systems.”

In a statement, Visa said that it too would also be able to make “a swift transition to a new currency with the minimum possible disruption to consumers and retailers.”

Juniper Networks, a provider of networking technology based in California, created a “Euro Zone Crisis Assessment and Contingency Plan,” which company officials liken to the kind of business continuity plans they maintain in the event of an earthquake.

“It’s about having an awareness versus having to scramble,” said Catherine Portman, vice president for treasury at Juniper. The company has already begun moving funds in euro zone banks to accounts elsewhere more frequently, while making sure it has adequate money and liquidity in place so employees and suppliers are paid without disruption.

FMC, a chemical giant based in Philadelphia, is asking some Greek customers to pay in advance, rather than risk selling to them now and not getting paid later. It has also begun to avoid keeping any excess cash in Greek, Spanish or Italian bank accounts, while carefully monitoring the creditworthiness of customers in those countries.

“It’s been a very hot topic,” said Thomas C. Deas Jr., an FMC executive who serves as chairman of the National Association of Corporate Treasurers. Members of his group discussed the issue on a conference call last Tuesday, he added.

American companies have actually been more aggressive about seeking out advice than their European counterparts, according to John Gibbons, head of treasury services in Europe for JPMorgan Chase.

Mr. Gibbons said a handful of the largest American companies had requested the special accounts configured for a currency that did not yet exist.

“We’re planning against the extreme,” he said. “You don’t lose anything by doing it.”

WASHINGTON (MarketWatch) — The following is the text of Federal Reserve Chairman Ben Bernanke’s speech at Jackson Hole, as prepared for delivery:

“When we convened in Jackson Hole in August 2007, the Federal Open Market Committee’s (FOMC) target for the federal funds rate was 5-1/4 percent. Sixteen months later, with the financial crisis in full swing, the FOMC had lowered the target for the federal funds rate to nearly zero, thereby entering the unfamiliar territory of having to conduct monetary policy with the policy interest rate at its effective lower bound. The unusual severity of the recession and ongoing strains in financial markets made the challenges facing monetary policymakers all the greater.

Today I will review the evolution of U.S. monetary policy since late 2007. My focus will be the Federal Reserve’s experience with nontraditional policy tools, notably those based on the management of the Federal Reserve’s balance sheet and on its public communications. I’ll discuss what we have learned about the efficacy and drawbacks of these less familiar forms of monetary policy, and I’ll talk about the implications for the Federal Reserve’s ongoing efforts to promote a return to maximum employment in a context of price stability.

Monetary Policy in 2007 and 2008

When significant financial stresses first emerged, in August 2007, the FOMC responded quickly, first through liquidity actions–cutting the discount rate and extending term loans to banks–and then, in September, by lowering the target for the federal funds rate by 50 basis points. 1 As further indications of economic weakness appeared over subsequent months, the Committee reduced its target for the federal funds rate by a cumulative 325 basis points, leaving the target at 2 percent by the spring of 2008.

The Committee held rates constant over the summer as it monitored economic and financial conditions. When the crisis intensified markedly in the fall, the Committee responded by cutting the target for the federal funds rate by 100 basis points in October, with half of this easing coming as part of an unprecedented coordinated interest rate cut by six major central banks. Then, in December 2008, as evidence of a dramatic slowdown mounted, the Committee reduced its target to a range of 0 to 25 basis points, effectively its lower bound. That target range remains in place today.

Despite the easing of monetary policy, dysfunction in credit markets continued to worsen. As you know, in the latter part of 2008 and early 2009, the Federal Reserve took extraordinary steps to provide liquidity and support credit market functioning, including the establishment of a number of emergency lending facilities and the creation or extension of currency swap agreements with 14 central banks around the world.2 In its role as banking regulator, the Federal Reserve also led stress tests of the largest U.S. bank holding companies, setting the stage for the companies to raise capital. These actions–along with a host of interventions by other policymakers in the United States and throughout the world–helped stabilize global financial markets, which in turn served to check the deterioration in the real economy and the emergence of deflationary pressures.

Unfortunately, although it is likely that even worse outcomes had been averted, the damage to the economy was severe. The unemployment rate in the United States rose from about 6 percent in September 2008 to nearly 9 percent by April 2009–it would peak at 10 percent in October–while inflation declined sharply. As the crisis crested, and with the federal funds rate at its effective lower bound, the FOMC turned to nontraditional policy approaches to support the recovery.

As the Committee embarked on this path, we were guided by some general principles and some insightful academic work but–with the important exception of the Japanese case–limited historical experience. As a result, central bankers in the United States, and those in other advanced economies facing similar problems, have been in the process of learning by doing. I will discuss some of what we have learned, beginning with our experience conducting policy using the Federal Reserve’s balance sheet, then turn to our use of communications tools.

Balance Sheet Tools

In using the Federal Reserve’s balance sheet as a tool for achieving its mandated objectives of maximum employment and price stability, the FOMC has focused on the acquisition of longer-term securities–specifically, Treasury and agency securities, which are the principal types of securities that the Federal Reserve is permitted to buy under the Federal Reserve Act.3 One mechanism through which such purchases are believed to affect the economy is the so-called portfolio balance channel, which is based on the ideas of a number of well-known monetary economists, including James Tobin, Milton Friedman, Franco Modigliani, Karl Brunner, and Allan Meltzer. The key premise underlying this channel is that, for a variety of reasons, different classes of financial assets are not perfect substitutes in investors’ portfolios.4 For example, some institutional investors face regulatory restrictions on the types of securities they can hold, retail investors may be reluctant to hold certain types of assets because of high transactions or information costs, and some assets have risk characteristics that are difficult or costly to hedge.

Imperfect substitutability of assets implies that changes in the supplies of various assets available to private investors may affect the prices and yields of those assets. Thus, Federal Reserve purchases of mortgage-backed securities (MBS), for example, should raise the prices and lower the yields of those securities; moreover, as investors rebalance their portfolios by replacing the MBS sold to the Federal Reserve with other assets, the prices of the assets they buy should rise and their yields decline as well. Declining yields and rising asset prices ease overall financial conditions and stimulate economic activity through channels similar to those for conventional monetary policy. Following this logic, Tobin suggested that purchases of longer-term securities by the Federal Reserve during the Great Depression could have helped the U.S. economy recover despite the fact that short-term rates were close to zero, and Friedman argued for large-scale purchases of long-term bonds by the Bank of Japan to help overcome Japan’s deflationary trap.5

Large-scale asset purchases can influence financial conditions and the broader economy through other channels as well. For instance, they can signal that the central bank intends to pursue a persistently more accommodative policy stance than previously thought, thereby lowering investors’ expectations for the future path of the federal funds rate and putting additional downward pressure on long-term interest rates, particularly in real terms. Such signaling can also increase household and business confidence by helping to diminish concerns about “tail” risks such as deflation. During stressful periods, asset purchases may also improve the functioning of financial markets, thereby easing credit conditions in some sectors.

With the space for further cuts in the target for the federal funds rate increasingly limited, in late 2008 the Federal Reserve initiated a series of large-scale asset purchases (LSAPs). In November, the FOMC announced a program to purchase a total of $600 billion in agency MBS and agency debt.6 In March 2009, the FOMC expanded this purchase program substantially, announcing that it would purchase up to $1.25 trillion of agency MBS, up to $200 billion of agency debt, and up to $300 billion of longer-term Treasury debt.7 These purchases were completed, with minor adjustments, in early 2010.8 In November 2010, the FOMC announced that it would further expand the Federal Reserve’s security holdings by purchasing an additional $600 billion of longer-term Treasury securities over a period ending in mid-2011.9

About a year ago, the FOMC introduced a variation on its earlier purchase programs, known as the maturity extension program (MEP), under which the Federal Reserve would purchase $400 billion of long-term Treasury securities and sell an equivalent amount of shorter-term Treasury securities over the period ending in June 2012.10 The FOMC subsequently extended the MEP through the end of this year.11 By reducing the average maturity of the securities held by the public, the MEP puts additional downward pressure on longer-term interest rates and further eases overall financial conditions.

How effective are balance sheet policies? After nearly four years of experience with large-scale asset purchases, a substantial body of empirical work on their effects has emerged. Generally, this research finds that the Federal Reserve’s large-scale purchases have significantly lowered long-term Treasury yields. For example, studies have found that the $1.7 trillion in purchases of Treasury and agency securities under the first LSAP program reduced the yield on 10-year Treasury securities by between 40 and 110 basis points. The $600 billion in Treasury purchases under the second LSAP program has been credited with lowering 10-year yields by an additional 15 to 45 basis points.12 Three studies considering the cumulative influence of all the Federal Reserve’s asset purchases, including those made under the MEP, found total effects between 80 and 120 basis points on the 10-year Treasury yield.13 These effects are economically meaningful.

Importantly, the effects of LSAPs do not appear to be confined to longer-term Treasury yields. Notably, LSAPs have been found to be associated with significant declines in the yields on both corporate bonds and MBS.14 The first purchase program, in particular, has been linked to substantial reductions in MBS yields and retail mortgage rates. LSAPs also appear to have boosted stock prices, presumably both by lowering discount rates and by improving the economic outlook; it is probably not a coincidence that the sustained recovery in U.S. equity prices began in March 2009, shortly after the FOMC’s decision to greatly expand securities purchases. This effect is potentially important because stock values affect both consumption and investment decisions.

While there is substantial evidence that the Federal Reserve’s asset purchases have lowered longer-term yields and eased broader financial conditions, obtaining precise estimates of the effects of these operations on the broader economy is inherently difficult, as the counterfactual–how the economy would have performed in the absence of the Federal Reserve’s actions–cannot be directly observed. If we are willing to take as a working assumption that the effects of easier financial conditions on the economy are similar to those observed historically, then econometric models can be used to estimate the effects of LSAPs on the economy. Model simulations conducted at the Federal Reserve generally find that the securities purchase programs have provided significant help for the economy. For example, a study using the Board’s FRB/US model of the economy found that, as of 2012, the first two rounds of LSAPs may have raised the level of output by almost 3 percent and increased private payroll employment by more than 2 million jobs, relative to what otherwise would have occurred.15 The Bank of England has used LSAPs in a manner similar to that of the Federal Reserve, so it is of interest that researchers have found the financial and macroeconomic effects of the British programs to be qualitatively similar to those in the United States.16

To be sure, these estimates of the macroeconomic effects of LSAPs should be treated with caution. It is likely that the crisis and the recession have attenuated some of the normal transmission channels of monetary policy relative to what is assumed in the models; for example, restrictive mortgage underwriting standards have reduced the effects of lower mortgage rates. Further, the estimated macroeconomic effects depend on uncertain estimates of the persistence of the effects of LSAPs on financial conditions.17 Overall, however, a balanced reading of the evidence supports the conclusion that central bank securities purchases have provided meaningful support to the economic recovery while mitigating deflationary risks.

Now I will turn to our use of communications tools.

Communication Tools

Clear communication is always important in central banking, but it can be especially important when economic conditions call for further policy stimulus but the policy rate is already at its effective lower bound. In particular, forward guidance that lowers private-sector expectations regarding future short-term rates should cause longer-term interest rates to decline, leading to more accommodative financial conditions.18

The Federal Reserve has made considerable use of forward guidance as a policy tool.19 From March 2009 through June 2011, the FOMC’s postmeeting statement noted that economic conditions “are likely to warrant exceptionally low levels of the federal funds rate for an extended period.”20 At the August 2011 meeting, the Committee made its guidance more precise by stating that economic conditions would likely warrant that the federal funds rate remain exceptionally low “at least through mid-2013.”21 At the beginning of this year, the FOMC extended the anticipated period of exceptionally low rates further, to “at least through late 2014,” guidance that has been reaffirmed at subsequent meetings.22 As the language indicates, this guidance is not an unconditional promise; rather, it is a statement about the FOMC’s collective judgment regarding the path of policy that is likely to prove appropriate, given the Committee’s objectives and its outlook for the economy.

The views of Committee members regarding the likely timing of policy firming represent a balance of many factors, but the current forward guidance is broadly consistent with prescriptions coming from a range of standard benchmarks, including simple policy rules and optimal control methods.23 Some of the policy rules informing the forward guidance relate policy interest rates to familiar determinants, such as inflation and the output gap. But a number of considerations also argue for planning to keep rates low for a longer time than implied by policy rules developed during more normal periods. These considerations include the need to take out insurance against the realization of downside risks, which are particularly difficult to manage when rates are close to their effective lower bound; the possibility that, because of various unusual headwinds slowing the recovery, the economy needs more policy support than usual at this stage of the cycle; and the need to compensate for limits to policy accommodation resulting from the lower bound on rates.24