Symbol U, atomic #92, Uranium is Earth’s heaviest natural occurring element in the periodic table.

Earth is dominated by the following 4 elements; Oxygen #8, Magnesium #12, Silicon #14 and Iron #26. For reference Silver is #47 and Gold #79.

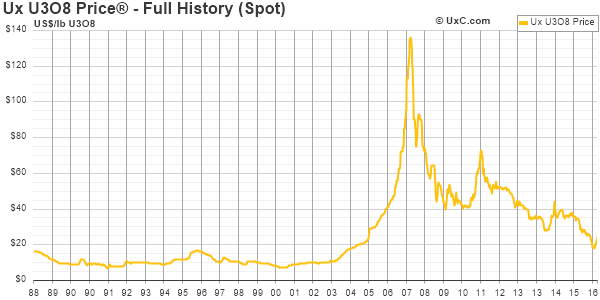

Uranium has garnered a lot of attention this far in 2017. Little wonder, as the uranium plays are up nearly 60% since the deemed pro-nuclear Trump was elected in November 16′. Using the largest uranium ETF, ticker URA – Globe X Uranium ETF as a proxy for the space, https://www.globalxfunds.com/content/files/Global-X-Uranium-ETF-1.pdf ,one can clearly see the pain inflicted over the last 5+ years;

2017 +27%, 2016 -1%, 2015 -37%, 2014 -23%, 2013 -21%, 2012 -19%, 2011 -60.%. From inception (11/4/2010), URA is down 79.5% cumulative.

U3O8 uranium currently trades as $25.31.lb. down 81.4% from the 2007 high of $136/lb.

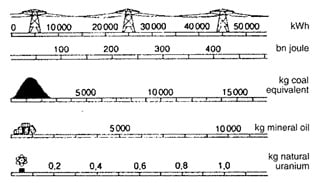

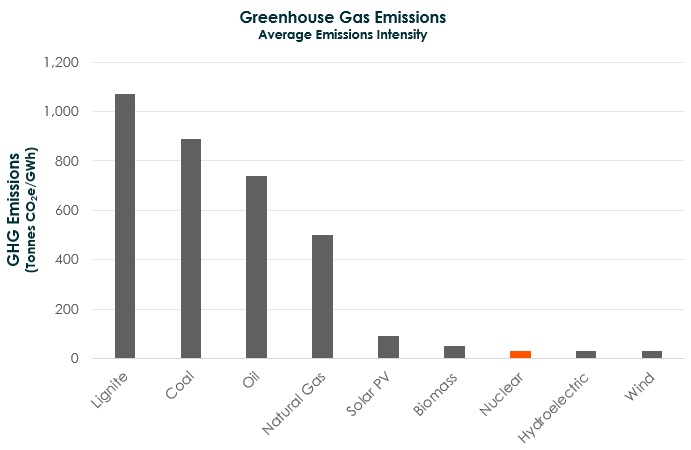

The merit of nuclear power on metrics of both energy security and a low-carbon future are beyond refute. Real facts;

1 kg. of uranium, post enrichment and used for power generation in light water reactors produces 45,000 kWh of electricity. From an output perspective 1 kg. of uranium is equivalent to almost 10,000 kg. of mineral oil and 14,000 kg. of coal.

The comparisons on emissions are as striking as on energy output;

Approximately 10% of current world energy supply comes from nuclear power. There are 447 operable nuclear reactors in the world at present, requiring 140 million lbs. of uranium per annum. Utility stocks are estimated at 478 million lbs., 3.4 year of demand. The largest 3 markets for nuclear power are France (58 reactors, 75% of overall power coming from nuclear), Japan (42 operable reactors, 40% of power pre-Fukushima disaster, only 3 have been brought online since all closed in 2011) and USA (99 reactors, 20% of overall power). A total of 60 reactors are under construction at present in China, India, South Korea, UAE and Russia . Twenty two of the nuclear plants under construction are in pollution ridden China, where 40% of growing electricity demand is still coal-powered, and the liveability of 25 of its largest cities hinge on nuclear power’s hockey stick growth projection. China is expected to have 40 nuclear reactors online by 2020 and to add 10 per annum thereafter. CNECC (China Nuclear Engineering and Construction Corporation) is the exclusive nuclear plant builder in China.

The USA only produces 4.3mm lbs. of uranium at present (2% of global output) versus an annual need of 56mm lbs., hence 93% of the uranium the US needs annually to operate existing nuclear plants is imported from places like Kazakhstan (39% of world uranium supply). Canada accounts for 22% of world supply and Australia 9%.

The World Nuclear Association (WNA) appear to have the best stats on the space. The top producer is Kazakhstan’s KazAtomProm at a 22% share. They recently announced a 10% production cut for 2017 (3% of world supply).

Canada’s Cameco is world #2 producer, not far behind KazAtomProm, at 18% of global production. The stock ticker is CCJ on the NYSE in US dollars and CCO on the TSX in dollarette’s (CAD). Despite all the seemingly good fundamental news on uranium, the price action has been nauseating. Cameco has some issues. Customer concentration is one, whereby almost 1/2 their long term sales contracts are with 5 key customers. Cameco received a termination notice last week from Japan’s TEPCO (Tokyo Electric Power, operator/clean upper of the crippled Fukushima plant) on a contract running through 2028 worth approx. $1bln. To give you an idea how offside TEPCO was on this long term uranium contract, 9.3mm lbs. spot is worth approx. $233,000,000 versus the $1bln contracted value, that is a $767mm potential hickey for Tepco. They have claimed “force majeure” in cancelling the Cameco contract, which might have had a shot of success if they had not accepted deliveries and paid for uranium 2014-2016. Sounds more like force manure to me, most expect Tepco will have to honor the contract via legal settlement. The news sent CCJ shares down 12.5% last week, although it remains above the 200-day moving average at $10.67.

The 2nd blemish to be addressed by potential longs is Cameco’s ongoing tax battle with the Canadian tax authorities, the venerable Canadian Revenue Agency (CRA). CRA are asking for C$2.2bln (US$1.7bln) in back taxes related to a purported tax dodge run by Cameco 2005-2015 where C$7.4bln of earnings were allegedly run through a low-tax Switzerland subsidiary. Most expect this case to be settled out of court in either 2017 or 2018, but the magnitude is unsettling to say the least. Plenty of press on the matter for those that would like to weight the merit of the case. The market cap of CCJ, as noted, the 2nd largest global uranium producer, is $4.15bln or 10% of TSLA ($40.4bln), as a point of reference.

There is a high degree of idiosyncratic risk in buying the listed equity of individual uranium companies. The largest ETF highlighted above, URA has enough daily turnover to be considered liquid, but it small at $250mm in AUM (MER 0.70%). The weighting of the ETF in Canadian uranium names is high at 60% (23% in Cameco alone). The Kazakhstan names do not have listed equity.

For those seeking modest allocations to the uranium space, I would recommend looking at URA for the diversification, but shorting CCJ to reduce the single name exposure. With the proceeds of the CCJ short I would buy smaller US producers (some better described as micro-caps) as they will likely have few headwinds under the current administration (i.e. permitting, production, and expansion). The smaller players are largely unhedged without long term supply contract hence they provide more leverage to the underlying uranium price.

A sustained recovery in uranium equities depends on uranium prices staging a recovery from the depressed levels we have seen over the last several years. We have smoke, we need fire. JCG

Note: Long CCJ (1% weighting), but looking to diversify near term to a broader grouping of uranium names.

Comments »