Bill Hwang, CEO and founder Archegos Capital Management. Note: (Mrs. Doubtfire/Psy). Heaven and hell. How can the same coin encapsulate such a degree of dichotomy? God – heads, Lucifer – tails.

Bill (Sung Kook) Hwang (58) just experienced a post ides of March for the ages. Julian Robertson protégé, ex-founder of NY-based Tiger Asia Management ($8bln in AUM at its peak circa 2007 after a 40%+ return year) and one of the most under the radar, successful “Tiger cubs”, just got cancelled.

Archegos carcass was laid bare for the hyenas last week, due to margin calls (under ISDA/CSA see below), prompted by ruinous losses in Chinese burritos ($GSX, $DAO, $IQ, $TIGR, $TAL, and $DOYU) and USA media/sundry equities ($DISCA, $VIAC, $RAAS, $SAIC, $DM and $AMC), among other cannon fodder names.

Post insider trading charges (US-SEC), circa 2012, Bill Hwang was forbidden from managing money for 3rd parties going forward. By grace of God, net of the $44 million paid in fines/reparations (12-months of probation was duly served) Billy still had a grubstake of US$200 million to launch his family office, Archegos Capital Management . The name Archegos comes from the Greek, “one who leads the way”, sometimes to the path of damnation, it appears. Of the seven deadly sins only two appear evident in this sordid tale; namely pride and greed.

Over the ensuing period of 8 years, Hwang compounded his $200 million chit at a staggering 63% @ compounded return to enter 2021 with a gob-smacking $10bln in AUM.

Strategy. Equity long/short. Short, no view, ….. let’s go with the indices (S&P and NASDAQ). Longs; concentrated (10-15%+ mkt cap in some names), cash (margin) +synthetic (over-the-counter) derivative exposure. Documentation; trade – total return swaps (aka equity swaps where the underlying is stock). Documentation – Master agreement; ISDA (International Swap Dealers Association) including CSA (Credit Support Annex) schedule. Threshold $0. Daily mark-to-market. Acceptable collateral; USD fiat at 100%, US equities 70% margin credit, China ADRs 60% margin credit (blended). Rumors of re-hypothecation likely just that, rumors as the ISDA/CSA control groups within the investment banks run a tight ship .

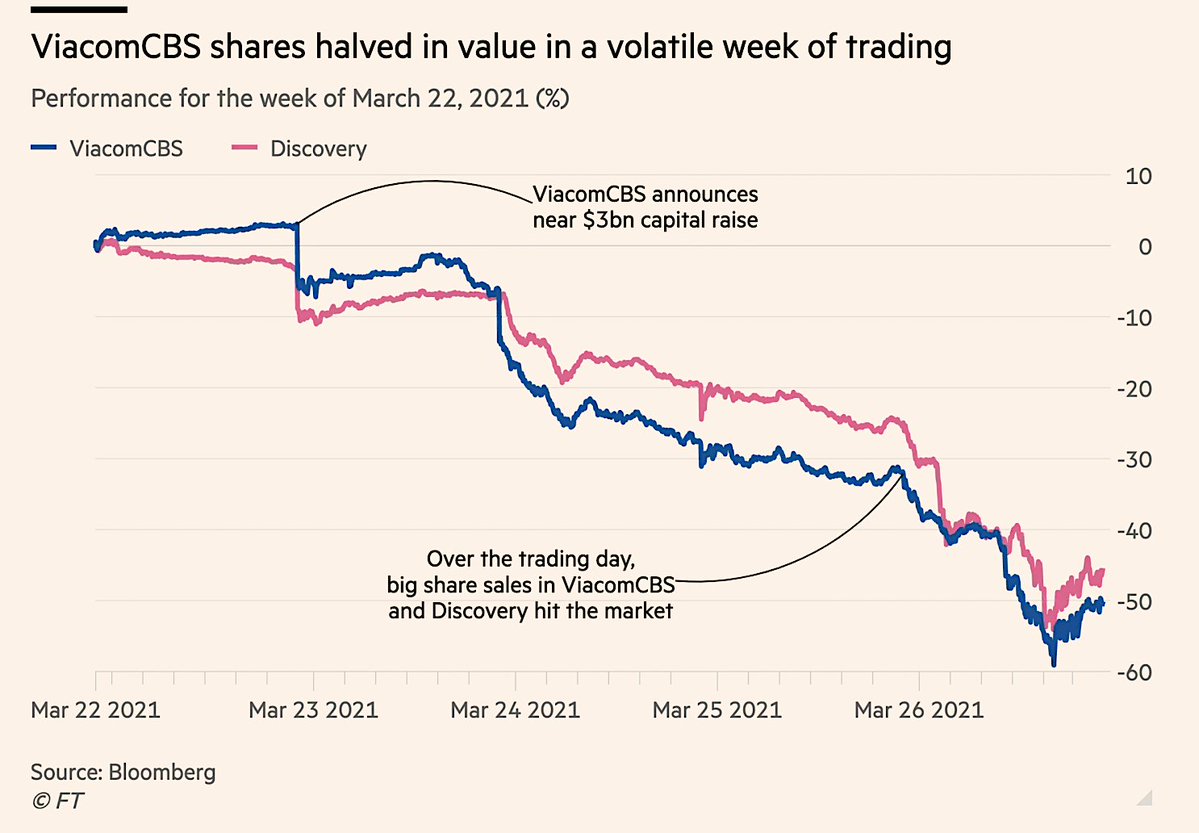

Possible portfolio scenario. Long $80bln (margin) single name equities China ADRs/US $3.2bln pledged to prime brokers (GS, MS, CS, Nomura, MUFG, sundry), short ES/NQ $30bln notional margin $2.4bln. Starting cash $10bln, margin pledged to date $5.6bln, with $4.4bln in reserve …. all-good, ATH ahead. Viacom announced $3bln secondary trades, trades off hard (graph below). China names also off hard to start the week on a “risk-off” move. ES/NQ short bleeding (smalls, < $1bln of margin), Longs -8%, margin call $6.4bln, shy $3bln +. PB’s liquidate TRS hedges (long underlying). GS sells $10.5bln underlying Friday Mar 26th, incl. 20mm share block of Viacom (GS hedged, no loss, “hold my beer”) MS sells $5bln in stock Friday, also via block trades …… CS and Nomura have a sleepless weekend. Square positions post carnage of 26th block trades to crystalize mtm losses of prior week.

Mr. Hwang is abstentious, a devoted Christian. Sung Kook Hwang is Korean-American, son of a Korean Pastor father and a Catholic Missionary mother who primarily worked in Mexico. If CRISPR babies were a thing in the early 60’s Sung Kook might have been patient zero.

No drink. No smoke. Married, 1 child (22, NYC), residence, Tenafly, NJ. (pop. 15,000, 15% Korean-American, 2008 house cost $3.5mm, a “modest house” for someone with a net worth in the billions), ride; Hyundai, Genesis (the same chariot T Woods almost off’d himself in pre-breakfast), joking aside Bill does have a Mercedes as well.

Charitable foundation; Grace & Mercy Foundation ($590mm AUM) but with some ties/exposure to Archegos prior to Archegos being zero’d Mar 26, 2021. $20mm $AMZN stock donated in 2020. G&M distributed $50-70mm per annum reportedly, a goodly portion to various Korean charity organizations. Online bibles seems to be one of Bill’s giving niches. Like many, I think Bezos has us covered on that front. The Bible has #1 best seller title by a country mile, 3.9bln copies read (Mao Tse-Tung #2 at 830mm and Harry Potter 3rd at 400mm).

Only 2/7 deadly sins, but clearly that was enough. Pride. Greed.

A deeper dive on God vs. VaR; (in Korean, with subtitles).

https://www.youtube.com/watch?v=VcO5QVVtYiQ&ab_channel=TheGraceandMercy

I fought the VaR and the VaR won. At $10bln (unlevered), Bill Hwang had already amassed generational wealth for his compact family unit and broader Christian flock. The second of his vices, greed, clearly took hold in this instance.

Netflix is a lock for Margin Call II. A Parasite sequel can clearly not be ruled out.

The inter-web has Bill Hwang’s purported portfolio listed already.

Not cool to dance on anyone’s grave, but Billy cost regular folks real money in this facade. Partnered with other cubs, with whom he shared bath-water, they cornered upwards of 70% of the float in names like $GSX, GSX Techedu, investigated by the SEC in 2020 for allegations of fraud (i.e. fake clients/bots) has a 52-week range of $33-$149, near that lower bound after the post Hwang margin driven drubbing. $GSX, almost 70% down in a week, still sports a market cap of US$8bln! There is a reason shorts are at near record lows. There are reasons margin debt is at/near all time highs (US$800bln +). None of this aids in the C-19 recovery. It increased market fragility, as CPI prints benign and the VIX floats south through 20. The ruling class check their 7 and in some cases 8 figure account statements, while the working poor sip stone soup. This is not God’s Work Mr. Hwang.

Nomura disclosed losses of US$2bln related to the Archegos wind-down as Japan’s fiscal year end of Mar 31st approached (also pulled a $3bln bond issue priced days prior). Nomura should have been genki with the Nikkei finishing up the fiscal year up > 50%, best innings since 1972. Nomura credit rating has been placed on negative watch (Baa1/BBB+ presently). Nomura stock traded limit down in Tokyo trade and is set to finish down > 15% on the week. Credit Suisse, on the heels of a $1bln hickey on supply chain manager Grensill have not tightened their band of pain yet and peg the Archegos tally at -$3-5bln. MUFG made a late week disclosure that they also rubbed up against Archegos with -US$300 million their estimated tithe. CS stock is down 18% on the week with rumors of an equity raise swirling. Deutsche Bank miraculously side-stepped the potential $4bln goring due with timely collateral dispositions/hedging. Early action by Goldman (vampire squid) and Morgan Stanley on Friday to flatten their risk seem to have been successful.

Hedge funds manage $3.8 trillion at present. They have been leap-frogged by 7,100 family offices which manage $5.9 trillion. Less 2 sigma events (on balance) and restrictive regulations have prompted many hedge funds to convert to family office structures (return 3rd party money and manage funds for sponsors and staff only). In the hedge fund space, the big get bigger; Millenium 277b/42b net AUM for 6.6x leverage. Citadel 234b/29bln net AUM 8.1x leverage.

Follow me on Twitter @firehorsecaper

Caleb Gibbons, CFA, FRM, SCR

If you enjoy the content at iBankCoin, please follow us on Twitter

Good read, thanks.

CCJ has doubled in price since last April!