Money is power, and in that government which pays all the public officers of the states will all political power be substantially concentrated. — Andrew Jackson

What a great day for the Jacksonian Portfolio, no? I felt like the Great Man re-born, breaching the lines of villainous (shorting) Redcoats with my trusty white charger, cutlass slashing down upon their ridiculous feathered bonnets, calling for my Horsed Kentucky Rifleman Sharpshooters to release another volley of musket upon their pasty-pale visages. Triumph!

And what’s more it’s a triumph over fear, as well, for with our solid Jacksonian Core Portfolio, we know that these wins are not only for today, but will be substantiated again tomorrow. For when the fickle winds of Washington change course again, and blow against our frail banking system’s walking corpse, rather than hold it aloft as it has, we will be prepared. Hard money and assets will be our stores of value, no matter what our increasingly Zimbabwean central government shall make of our paper printed with the General’s startled masque.

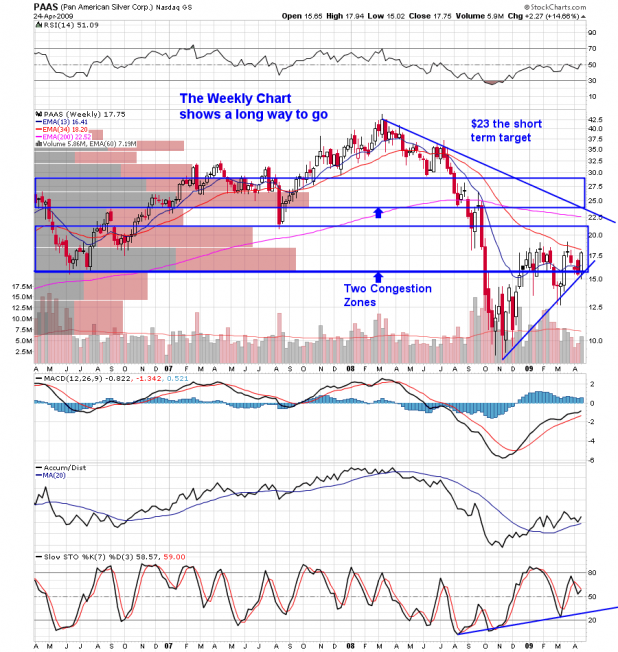

Today’s “core” wins — “early” wins, I call them — include PAAS (+6.82%), GDX (+5.97%), SLW (+ 3.03%) RGLD (+3.93%%), NRP (+3.68%), SLV (+2.89%) GLD (+1.46%) and newcomer to the Core Portfolio: SSRI (+6.62).

Of the Core that was involved in earnings tonight, we have TSO giving back strong wins from today (currently – 1.52% @ $17.53 in AH) and Mr. Anderson — ANDE — up large after hours (currently +13.95% @ $20.10 in AH). You will recall that I sold the $17.50 June calls on TSO two days back, as I felt it was getting overextended. I will likely close that position tomorrow, at profit. I still retain my unhedged position in ANDE. Other Core holdings that were down slightly today include MON (-0.88%) which needed a breather, and TC (-0.91%), whose 7 cent pullback today was also not unexpected after many days of gains.

Other non-core silver and gold plays I am currently invested in include EGO (+3.69), ANV (+3.82%), and EXK (+4.85%). Last, recent recommendation ATHR (-1.16%) was also off a bit. On the oil front, I bailed on all but a stub of my triple earl ERX (+10.71%) at just under $34.00, as that was where a significant fibonacci line lay, and I’ve learned to respect the fibs on these fast moving triple ETF’s.

I am still bullish on our friend Earl, however, as I have been since Fly cursed his name. My two “core holdings” — which may soon be nominated to the Jacksonian Core — are PBR (+2.93%) and OXY (6.66%) , the best of two nations, in my humblest opinions.

I must admit to revelling in some of Fly, RC and CA’s crazy picks today (among them SONS, and FLOW), and I even jumped into one of my own (ABK) — it is fun to make hay while the SONS is shining, after all. But make no mistake, these discretionary picks are a tiny portion of my portfolio. For like the leaves of summer, these high flyers will soon fade, as will our newly reinvigorated “saved” banks. We must always be girded with our Jacksonian Core to withstand the coming tsunami, and we will continue to build on that foundation as we jog onward. My best to you all, and keep building!

Important: Hat tip and my thanks to Trader Caddy and to Chanci for the suggestions on SSRI and EXK, respectively.

Aside: If I could tell you to get into one sector in the coming weeks, my friends, silver would lessen my worries for you and yours.

________________

UPDATE: I decided it would be almost hypocritical of me to urge silver on my blogreaders w/out taking at least a small position in AGQ (Proshares Double Silver) .

Or that could just be me rationalizing my inner Yukon Cornelius.

You make the call. That said, I’m picking up some AGQ here @ $42.87.

UPDATE: Picked up a little more at $ 43.55

Caveat: VERY VERY VOLATILE! If you buy any of this crazy stuff, there’s a 73% probability you will be drafted to become intergalactic Herald to a very large planet eating sub-god, with little sense of humor, and you may lose your pension.

_____

Comments »