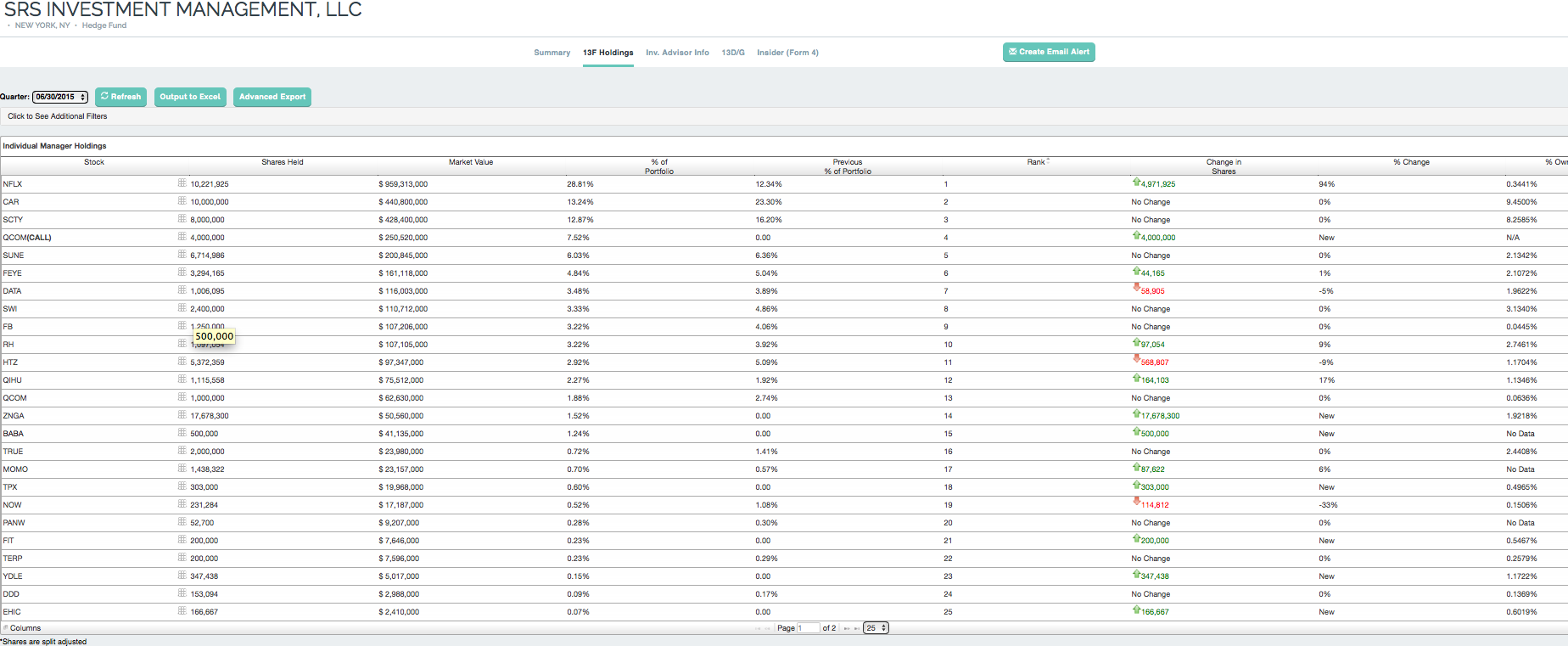

Based on 13F filings, a dated (6/15) view on the top holders of SUNE:

When we click on the holdings of top-15 holder SRS holdings, we see the following:

SUNE isn’t their only major holding that’s recently experienced a serious decline, for example, FEYE, SCTY & QCOM.

Even their winners, like DATA and PANW, have been weak recently. DATA just killed it on ER & PANW is destroying all comers in cyber security sales. I wonder how much of their recent weakness is due to the decline of say a SUNE or VRX? Hard to tell for sure. Both have high p/s ratios, AWS launched its QuickSight data analytics service, and I hear China is getting out of the corporate hacking game.

Hah-hah. That was fun. China, right. Ok, while there is a possibility these are the reasons, it doesn’t take very long to shoot them down. (I mean, have you seen QuickSight?) IMHO, there is a far greater probability that this weakness has more to do with weak hands. I’ll explain.

Although we don’t know how SRS is hedged or what kind of leverage they utilize, we do know, however, that many hedge funds stopped hedging as much as they once did. Hedging is expensive and hard to do effectively.

We also know that a hedge fund that’s scared of leverage is about as common as a dentist who’s scared of teeth.

And we know hedge funds have a tendency to cluster. Research is hard to do well and it’s also quite expensive. It’s attractive to “buy the mind” of someone who has a history of doing good research, like an Einhorn, Loeb or Ackman, and follow them into a trade. It can be a pretty smart strategy, but there are times when doing so is going to bring with it high volatility (shallow risk) and in some cases, deep risk. (Permanent loss of capital.)

The net result is when unhedged funds –with low conviction– follow others into leveraged trades, it’s a recipe for tears volatility.

When we see a drawdown in a common hedge fund favorite, much like we’ve seen in SUNE, VRX, SCTY, etc…the probability is high they’re going to be forced to sell something, and most often their low-conviction buys & recent winners are the first to go.

Here’s the most important thing, volatility can be a two-edged sword. Handled improperly, it can destroy you. Handled correctly, it can be your best friend.

Unless it’s say, a horribly overpriced growth stock that is no longer growing, or a stock that’s going to zero due to things like fraud or insolvency, then forced selling is an opportunity for unforced buyers. “Buy when the cannons are firing, and sell when the trumpets are blowing” as Nathan Rothschild is rumored to have said.

I’ve made more scaled purchases of SUNE today. Still small, average price of $5.50. Started picking up TERP as well. Both continued to be pummeled over the Vivint Solar acquisition and more specifically, concerns over SUNE’s debt. ($11.7b sounds like a big number, but this figure is the consolidated total of SUNE’s DevCo, along with SUNE’s retained projects, and both TERP and GLBL debt. Most importantly, counter party risk is low, suggesting it’s most likely a great deal of this selling has been due to a combination of leverage, margin-induced forced selling and a lack of conviction.)

I’ll build this up to 2% position. But if I’m wrong, and it goes to zero, position size will serve as primary risk management.

Cheap can always get cheaper.* Here’s to hoping it does.

*It’s the reason why most people are better off not trying to catch a falling knife.

SUNE has plunged to new multi-year lows after announcing mixed earnings (met revenue expectations; created a loss per share of -91 cents vs -70 cents expected), cutting its full-year cash available for distribution guidance, and narrowing its full-year project delivery guidance from 4.5GW to 3.3GW-3.7GW.

The entire solar sector is selling off hard. At present, TAN SCTY SLTD SPWR ENPH FSLR TERP JASO TSL SEDF are down between -3 to -20%.

Here’s the full section on SUNE from Greenlight Capital’s 3Q shareholder letter:

For the first part of the year SUNE was by far the fund’s biggest winner. The shares rallied from $19.51 to a peak of $32.13 on June 23 before collapsing to $7.18 by September 30. SUNE’s business is to develop solar and wind projects for major utilities and commercial customers that agree to buy the power over a very long term, often 20 years. These projects have purchase contracts from highly creditworthy counterparties and produce an average unlevered return on capital of 10% and 13% in developed and emerging markets, respectively. SUNE makes money by selling the projects at a premium to investors seeking safe, long-term income.

Given the low-rate environment, SUNE thought it could make even more money if it created its own related yield vehicles to buy the projects and dividend the income to shareholders. It created TerraForm Power (TERP) for its developed markets projects and TerraForm Global (GLBL) for its emerging markets projects. Initially this worked very well, and in July 2014, SUNE successfully brought TERP public. This July it brought GLBL public with much less success.

In the weeks before the GLBL initial public offering, SUNE was at its highs and we contemplated trimming the position. Since we expected the IPO would trigger a further advance in the shares, we decided against it. Around this same time, oil and gas prices renewed their declines, causing the values of energy master limited partnerships to justifiably fall. We believed that TERP and GLBL would not be impacted, as neither is subject to commodity risk. We were wrong. Because the SUNE yield vehicles were relatively new to investors, the market did not distinguish them from other energy dividend flow-through structures. In mid-July, TERP began falling along with the rest of the sector, taking SUNE with it. GLBL IPO’d at a big discount a week later and traded poorly in the aftermarket.

SUNE investors should note the following:

As GLBL and TERP continued to fall they effectively lost access to the capital markets, and SUNE collapsed as the market became worried that SUNE would not be able to sell its projects and could even run out of money. Ironically, the market judged SUNE’s rapidly growing and massive backlog of attractive projects to be a liability.

SUNE’s hard-to-decipher financial statements fed the stock collapse. SUNE consolidates both TERP and GLBL on its GAAP statements. The complicating result is two-fold: First, when SUNE sells a project to TERP or GLBL it bears the operating costs but doesn’t get to book the revenue from the sale. The result is the appearance of an operating loss. Second, TERP and GLBL use non-recourse project finance debt to fund the purchases and the debt appears on SUNE’s balance sheet. The result is that SUNE appears to be heavily levered and losing money. From a GAAP perspective that’s true, but from an economic perspective it is not. Nonetheless, this hasn’t stopped some wise guys from dubbing it “SunEnron”.

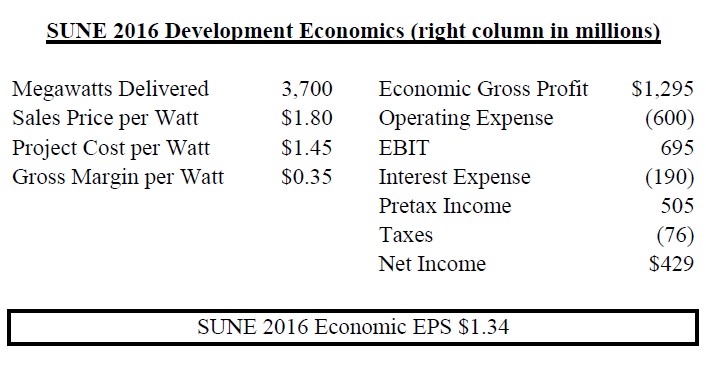

SUNE responded to the deteriorating environment by raising additional equity, finding third parties to buy its projects, and slowing its development pipeline. All of these actions have marginally lowered the company’s value, but have stabilized the situation. Taking into account the more conservative business plan, when we look through the complicated financials we believe that SUNE’s development business is poised to have economic earnings in 2016 of about $1.34 per share, assuming that TERP and GLBL ***do not regain access*** to the capital markets.

At 315M shares and a $1.8B market cap, SUNE is trading at about 4.3x $1.34 of “economic earnings” in the worst case where yield co’s don’t regain access to capital markets. Look, SUNE can always get cheaper, but that’s not a bad place to start buying given what we know is on the immediate horizon as it relates to the future of energy.

SUNE has additional value from its ownership of TERP and GLBL shares. During the panic, the market has fixated on the question of whether TERP and GLBL can access money cheaply enough to buy projects and grow their dividends. This is relevant insofar as it will determine whether they can be long-term buyers of SUNE’s projects, but we believe the market’s focus is too narrow.

The better question is: Do TERP and GLBL have the opportunity to buy projects at returns that exceed the risk? If they do, the capital markets would be wise to fund them. We believe the answer is a resounding “Yes.” A power plant with a long-term power purchase agreement is roughly equivalent to a secured lender. As the customers are strong credits, the ability to buy a portfolio of these projects at a 7% unlevered yield in developed markets and a 10% yield in emerging markets should be very attractive in the current income-starved environment, where 7-year A-rated corporate bonds yield less than 3.5%. We believe that once the market sorts through the mess, TERP and GLBL should recover and regain access to the capital markets. This would allow SUNE to realize substantial additional value.

The most important thing for SUNE bulls is whether SUNE and its yield vehicles TERP and GLBL can get access to funding, or whether there’s going to be a leverage-induced collapse. From Bronte Capital’s John Hempton, when he announced on October 2 they’d taken a position in SUNE:

Non-bank financials “blow up” for one of three reasons, (i) credit risk, (ii) duration mismatches and (iii) and unstable funding. If you want to assess TerraForm Power (Sun Edison’s yield co) you need to assess whether the credit risk on the projects (the counter-party) is okay, how the contract and funding is (eg floating/fixed etc) and all the ways in which project development funding is able to roll into long-dated funding.

A friend put this to a yieldco and the management balked at providing that level of project detail. My friend’s response: “well, are you Northern Rock?”

And that is the guts of the issue and the market fear. We have gone to considerable effort to convince ourselves Sun Edison is not Northern Rock with solar panels. We have talked to several people who have organised funding for these things and it seems okay to us. Specifically all construction finance automatically can be termed out as project finance (over the life of the project and linked to the project) when the construction is done.

If this is true the market fear for this company cannot cause insolvency. Given that the company is priced as if insolvency is likely this stock should produce a good return from here.

Alas we could be wrong here. We can’t see all the funding (the disclosure is complex) but the bits we have seen have this character. We checked through several sources and we don’t think the company can have a “run on the bank”. The Northern Rock outcome is unlikely.

Now of course we have not seen and understood all of the finance deals. Only the ones we can find. But that is sufficient to know we are probably right. And that is the case for buying. The old projects are good and they should run off at an attractive clip.

You should read the whole post. Hempton goes on to call for the head of SunEdison CEO Ahmad Chatila to roll.

He has not done very much that is wrong except create a business which he personally is a woefully inadequate CEO for. For this he should be rewarded: as recognition of (a) what he has truly created and (b) for going quietly and constructively.

Calculate his payout, add thirty percent and fire him.

There is a core criteria on picking the new CEO.

They need to be boring and from a control culture. The idea CEO would be someone from (say) the risk management department of Goldman Sachs. What you want is a dull suit occupied by someone whose job it is to pull wings off butterflies. Someone whose job it is to ensure – and be seen to ensure – that bad projects are not funded.

The market wants someone who will get on an earnings call and talk about asset liability matching, FX risk mitigation and basically sounds like the CEO of a mortgage REIT, not a semiconductor visionary.

You want risk aversion above all other things.

This company has got to become dull and predictable and it has to get there fast. Anything short of dull and predictable will end badly.

Here’s what SUNE’s CEO said on the call:

Right now I want the company to become more boring, Boring, and cash-flow generating.

Someone appears to be listening.

In a yield starved world, where the climate cops are pushing to zero carbon emissions in the next few decades, I see things much like Einhorn and Hempton. However –and pay attention to this– there still remains a possibility there could be a run on SUNE, and today we’re seeing investors panic because the company soothed no one when they said that “there are no assurances that we will be able to raise the $6.5 billion-$8.8 billion needed to fund the construction of renewable energy assets through 2016.”

So don’t mortgage the house and back up the truck, even here, and for the love of mike, pick up a long dated hedge.

But understand, this sort of panic is required for the much ballyhooed “blood on the street” conditions you’re looking to buy. Just don’t blow up buying it.

And as I said yesterday, nearly all of this is a self-inflicted gunshot wound. They can fix a lot of this.

I’ve only had a few orders hit thus far. I’m still very small and my average cost is $6.12. I would imagine, however, that the margin clerks are just about ready to start their work. Look for signs of capitulation starting around 2pm EST into the close.

Mon Nov 9, 2015 5:10pm ESTComments Off on $MSFT $VRNS Microsoft buys Unstructured Data Security Company Secure Islands

Secure Islands’ software automatically classifies, controls access to, and encrypts unstructured data. They are a competitor of Varonis.

Microsoft acquired SI today, and this is a good thing for Varonis.

Our recent 3-part series concluded that the most important thing for VRNS longs would be how quickly the company could simplify and scale what has been a difficult, evangelical sales process.

“This acquisition accelerates our ability to help customers secure their business data no matter where it is stored – across on-premises systems, Microsoft cloud services like Azure and Office 365, third-party services, and any Windows, iOS or Android device.”

Yes, Varonis now has Microsoft as a competitor. But as the leader in the unstructured data security space, Varonis will win their share.

Equally as important, if Microsoft’s competitors, who are the biggest names in IT, want to match this move, there just aren’t that many unstructured-data security properties available.

M&A comparables for technology acquisitions in the security space cluster near ~ 10x sales. Pulling out their cash, Varonis trades at only 3x sales. This is intriguing.

Most importantly, Microsoft just reinforced and validated the Varonis value proposition to global CISOs. Softie gets it. Companies need to secure unstructured data everywhere it resides.

This growing momentum is likely going to benefit Varonis in terms of making their sales cycle less evangelical and more scalable, and any sales growth acceleration is going to drive up the stock in a big way.

155 countries have submitted plans so far for the COP21 climate summit to be held by the United Nations in Paris this December. These already cover 88pc of global CO2 emissions and include the submissions of China and India. Taken together, they commit the world to a reduction in fossil fuel demand by 30pc to 40pc over the next 20 years, and this is just the start of a revolutionary shift to net zero emissions by 2080 or thereabouts. “It is unstoppable. No amount of lobbying at this point is going to change the direction,” said Christiana Figueres, the UN’s top climate official.

The IEA says China invested $80bn in renewable energy last year, as much as the US and the EU combined. It is blanketing chunks of the Gobi Desert with solar panels, necessary to absorb the massive surplus production of its own solar companies. The party’s Energy Research Institute has floated the idea of raising the renewable share of electricity to 86pc by 2050.

It is patently obvious that China is not about to sabotage a climate deal. Its submission to the COP21 summit aims for peak greenhouse emissions by 2030, if not before. It plans 200 gigawatts (GW) of wind and 100GW of solar by then, and a reduction in coal use from 2020 onwards. There will be a carbon emissions trading scheme as soon as 2017.

I have a series of extended hours (GTC) orders in place in an attempt to build a position on possible volatility when they report tonight tomorrow before the market opens.

I’ve been observing the Valeant train wreck saga from the sidelines these last two months. As a spectator, I find it remarkable –and, as an investor, humbling– on many different levels.

Is Valeant going to be Ackman’s Waterloo? What about the “un-hedged” funds who followed him into the trade? Is Valeant a fraud? Will they survive? What are the 2nd derivative impacts? Apparently the rumor going around today is that Pfizer might be interested in buying them. We’ll see.

I haven’t had any positions –I have no edge here, other than to have realized when the story started developing that deep, two-way risk existed– but my thoughts go out to all the people that have been deeply hurt by this affair.

The ramifications of what likely comes next for the Valeant players brings a story to mind from the days of the .com collapse. This story involves a fellow by the name of Charlie Thomas. Charlie was the CEO of a company called Net2000, who had a collection of data networking businesses. They started in network cabling, installing T1’s for thousand-dollar a month, 1.5Mb internet connections (I now receive 45Mbs from AT&T for $50, talk about deflation!) and reselling network services from Bell Atlantic (now Verizon). Soon, they evolved to building their own data network. As the stock price of anything internet related was going to the moon, they IPO’d. You know the rest. The stock did a moonshot, then collapsed. Investors lost their shirts.

I met Charlie briefly at a mutual friend’s home some years ago, shortly after he had written a book about his Net2000 experience. One of the vivid recollections I have from the book was his retelling of the emotional roller coaster of being immediately made paper-wealthy, and then watching helplessly as it all slipped away, followed by his feelings of depression and regret.

He explained the handcuffs that large shareholders have in terms of selling, hedging and diversifying their concentrated equity holdings. Someone can be worth a billion on paper, but if they can’t sell any stock due to insider restrictions, they might be struggling to make the monthly rent. To address the issue, underwriting banks will offer loans against these holdings, allowing these folks to get access to funds without having to actually sell their stock.

If your mental warning light just went off, good for you. This is nothing more than a loan on margin. And when the stock goes down, as NET2000’s did, the banks call in the loan. If you can’t put up additional collateral, they’ll sell your holdings for you, often at the worst possible time. (Aubrey McClendon of Chesapeake made this a relatively common occurrence. Most boards do not allow the practice. When a board does, it often can be an indicator of poor corporate controls.)

On Thursday, the fine people at Goldman Sachs called in a $100M loan to Mike Pearson, CEO (at least as of today) of Valeant. 1.3M shares, or about 10% of his total holdings, were bid at the ask, and helped contribute to yesterday’s 14% fall in VRX. Mr. Pearson, based on his 10.1M shares, has lost about $1.9B in the last two months, about 70% of his net worth, assuming all of his wealth is tied up in Valeant.

Pearson’s remaining shares are still worth about $830M, but 70% is a tough drawdown, I don’t care how much you have left. And it’s not clear how much of that he’ll get to bank, or how much his life as he knew it is about to change. There may be other shareholders or who are experiencing these calls and darkened futures as well.

I don’t know if Valeant is involved in fraud. Their formal business model, as they presented it, seemed morally questionable, but legal. The Philidor business, however, appears unsavory on every level. The probabilities suggest that something bad happened, and someone is likely going to be in a great deal of trouble.

On their last corporate earnings call, Valeant radically changed their business model. They will now embrace the inefficient R&D they used to be against, they’re going to stop rolling up companies with debt. This reversal means even if they escape the current federal investigations unscathed, Valeant is unlikely to be worth anything near what Ackman thinks thought it was a few months ago, when he presented it as the next Berkshire Hathaway. And unlike what Citron claims, it’s possible, but highly improbable that the shares will be going to zero. All of this will get resolved eventually — including what Pearson knew and how much he or other Valeant officers were involved in any wrong doing, if any. It will all come out.

We haven’t heard much from Pearson, and that is not helping his public image. But the probability exists the guy is completely overwhelmed, and not at all equipped to now reap the whirlwind he may, or may not have personally sown.

I have two immediate reactions from all this.

When I read about Goldman’s margin call, it made me think about the magnitude of what Pearson has been carrying the last few weeks. Innocent or guilty of wrong doing, the most likely path forward is he’ll soon lose his job. Worst case, he may possibly lose a huge portion of what he’s worked so hard his entire life to attain. If the latter occurs, he’s in for one of the toughest emotional tests life can throw at person. It’s one thing to have never had great wealth. It’s another thing entirely to have lost it all. If the worst happens over the next few years, Mike Pearson is going to learn an awful lot about who he really is, who his real friends are, and what really matters in life. It’s hard not to feel something on a deep level for a person that’s staring into that existential abyss, I don’t care what they’ve done.

What I recall most from the book Charlie Thomas wrote, was my impression of his sincere regret. Not for himself, but for the traumatic experience his investors and shareholders went through. Net2000 wasn’t a fraud, and let’s be clear we still don’t know what Valeant is, or what Pearson’s feelings are, but Charlie felt he had let everyone down. I wasn’t a shareholder in NET2000, but I’ve lost big money in other companies on more than one occasion, and Charlie’s sentiment meant something to me. I empathize with the personal guilt he clearly carried and the responsibility he felt for those that had been hurt by something he was personally involved in.

Human beings make bad decisions, that’s who we are. When we –flawed to the core, each and every one of us– can feel regret and seek forgiveness for mistakes we’ve made that have hurt others; and from the flip side, when we who have been hurt –perhaps seriously– can empathize with, and forgive those who are now dealing with the consequences of their decisions; well, from my perch it’s this two-way interaction that represents the very best of what we are as a species.

That we are capable of regret, empathy and forgiveness gives me hope that –much like we navigated the last 100 years of financial turmoil, nuclear threats and world wars– we’re going to successfully thread the needle of the next 50 years, despite the momentous change that may lie just ahead. Markets and people do adapt.

Just like Mike Pearson and Valeant, and quite possibly Elizabeth Holmes and Theranos, Charley Thomas’ net worth in NET2000 took a terrible hit, along with that of his investors and shareholders. Googling Charlie today, 15 years later, however, he appears to have very much recovered from what has to be one of the darker periods of his life. I’m glad. I also hope that Pearson and others neck deep in the Valeant nightmare can focus longterm, even as they go through the painful sausage grinder that’s immediately ahead.

There is a light at the end of the tunnel, and although it looks like it may be a freight train now, in 15 years, you may look back with a different perspective. Accept that things as you know them today are likely going to change, and may never go back to the way they were — but you can recover. And it may just turn out that where you end up is a far better place then the path on which you were headed.

My second takeaway is risk management truly matters.

There is a reason many of the great investors list their most important rule as “don’t ever lose money.” Shallow risk is your average volatility. Stocks go up, stocks go down. Odds are, the price and your money are mostly coming back.

Like I said, we don’t know if fraud occurred at Valeant. Regardless, investors have lost 70% in two months. Events like Valeant, Theranos, Madoff, Enron, and Worldcom are truly terrifying. Along with political instability, bankruptcy, war and hyperinflation, fraud and margin represent deep risk, as in “there is no possibility of your capital ever returning, it is gone.” Far, far more intelligent and sophisticated investors than I were caught in Valeant. Hopefully, they know what they’re doing when they make the decision to concentrate further in the position.

I run a concentrated portfolio myself, and if I want to survive over the long term, risk management has to be more than a daily aphorism. So when a drawdown on the scale of a Valeant occurs, with accusations of fraud being floated, I start thinking about each of my holdings, and what I need to do manage risk; constantly questioning the validity of a thesis, monitoring for change, position sizing, margin, dollar cost averaging, cutting bait. These are far easier to speak of than they are to effectively do, but an investor’s survival hangs in the balance. For the individual investor, managing risk is “the most important thing.”

I found that writing about these complicated topics was rather difficult to do…hopefully, it reads like it was intended.

Robots will take over 45pc of all jobs in manufacturing and shave $9 trillion off labour costs within a decade, leaving great swathes of the global society on the historical scrap heap.

BofA Merrill Lynch now predicts in its new 300 page research tome that as soon as 2025, robots and AI will up-end the global economy in a $30 trillion per year whirlwind of “creative disruption.”

According to Oxford University, this could leave up to 47% US workers at risk of being displaced by technology over the next 20 years, with job losses likely to be concentrated in healthcare, food service, agriculture, shipping and eldercare – or in other words, the majority of the manual, low-paying jobs that have been created in the recovery years since the global financial crisis.

Not that white collar workers should feel left out. If you’re one of the +25M presently employed in law, finance, sales or medicine (really?), apparently the Bobs will want to be scheduling time with you folks as well.

Of course, this won’t apply to oil, gas and coal workers. (Who should be well established within their new careers as financial bloggers by that point.)

Not to channel Picketty on you and such, but BofA’s robot uprising, should it occur, will not exactly reverse growing inequality trends…

In fact, (if you lean GOP, now’s the time to cover your eyes…) it likely ensures Universal Basic Income as the only version of this where the 99% don’t end up in some 2050 version of Elysium-meets-Gangs-of-New York hell-on-earth.

Eternal deflation and the end of economics itself may be nigh upon us.

More on all that later.

-g

For more on the robot jobocalypse, go here and here

Fri Nov 6, 2015 12:05am ESTComments Off on $XOM $XLE $SPY – So It Begins

In the question of the citizens of the world –and their politically ambitious Attorney Generals– v. the fossil fuel industry over the smallish matter known as The Global Climate Change, we present People’s Exhibit A:

The New York attorney general has begun an investigation of Exxon Mobil to determine whether the company lied to the public about the risks of climate change or to investors about how such risks might hurt the oil business.

According to people with knowledge of the investigation, Attorney General Eric T. Schneiderman issued a subpoena Wednesday evening to Exxon Mobil, demanding extensive financial records, emails and other documents.

The investigation focuses on whether statements the company made to investors about climate risks as recently as this year were consistent with the company’s own long-running scientific research.

The people said the inquiry would include a period of at least a decade during which Exxon Mobil funded outside groups that sought to undermine climate science, even as its in-house scientists were outlining the potential consequences — and uncertainties — to company executives. Continue reading the main story

Thu Nov 5, 2015 5:23pm ESTComments Off on Scoreboard check

After I posted the VRNS series – Part IPart IIPart III – the stock dropped to $14.6 during the regular session where I was able to add to a medium sized position. The stock is trading up 18% in the AH on a mild beat, but let’s see what it does tomorrow. (I don’t advise chasing it, instead, wait to see if it comes in off of the jobs numbers. It also may be a good idea not to buy the whole position at once.)

Volatility can be your friend, but I find I have to deeply understand something in order to have conviction –to know when the probabilities and risk/reward might be lining up– to buy it when its down, or, conversely, cut bait and run when the “most important thing” has changed. Truly understanding risk/reward takes time, hence the three novella-sized posts describing the VRNS background. Investing just may be the hardest –and potentially, most rewarding– game there is. But it will take everything you’ve got. (Speaking for myself, though, its the best job I ever had.)

In other news, Disney beat expectations but the stock is trading down slightly. (Hint: Valuations always matter, it’s just a question of when, not if, the market will pay attention. That said, I am likely to exit tomorrow as I think we see higher levels up to the movie release.)

I’ve also started small positions in BLUE ($69) and FEYE ($21.9). I had a chance late last night to read the latter’s call transcript, which actually fell beneath $21.75 at one point during the day, and there were good things and bad things. We’ll break them down in an upcoming post. For now, the progress they’re making on endpoint is enough to take a speculative stake, even though I still think we’ve yet to see a near term bottom.

As for BLUE, the bloom is off the rose, at least based on today’s price action. BLUE may be one of the most exciting names in the world once you have a sense of what they’re doing. That said, the awe of having a cure for everyone may be fading, but the data in the abstract looked pretty good:

In Bluebird’s case, the good news was this: Six of the nine patients who received the company’s so-called Lentiglobin gene therapy treatment haven’t needed blood transfusions since treatment. The length of time since treatment varies from six to 18 months.

But the bad news was that three other patients, who all have a more severe form of the disease called Cooley’s anemia, have needed some blood transfusions since treatment. The level of treatment is still less than the once-a-month transfusions they would have required otherwise.

To recap: two-thirds of the patients appear to be cured. The rest are being significantly helped. But because all of the patients haven’t been cured, investors drove down bluebird’s stock by 22 percent as of 1:15 p.m. to its lowest point in almost a year. Where as of June, bluebird was worth $5.4 billion it is now valued at less than half that, or slightly less than the Chicago-based retailer, Sears.

As the VRNS series took a bit longer than expected, I wasn’t able to post on ANET and DATA. I grabbed small long positions at the close, the latter of which jumped +20% in the AH. I’ll give you a breakdown of ANET’s legal situation with Cisco tomorrow. DATA will be the subject of a future post. (You already know this, but no chasing in the AH please.)

My impression is Varonis is an incredibly difficult sale. Last quarter, the CEO sounded frustrated. They hired a bunch of new sales reps earlier in the year, but the funnel isn’t filling –or closing– as quickly as they want.

Execution remains the primary obstacle, and its not an easy fix. IMHO, it’s asking a lot for a ‘security’ sales person to have the depth (technology), scope (across organizations and sectors), credibility (compliance regs, governance standards) and positioning (multi C- and SVP-level) to span across a distributed organization, create the budget and support necessary to essentially change how enterprises create and access information. (Contrast this with security sales people who are invited to RFPs with the benefit of a specific compliance driver!) It sounds to me like Varonis needs very special, very expensive people with a number of skills that are hard to find in a single package. The ideal candidate would be a former CISO/CIO with healthy BD skills, willing to give up 3/4 their salary for a high-pressure sales quota/commission. That’s a tall order. Can they get those people at the volume they need? Will every sale remain an evangelical one? And if not, when will it change?

And they have competition. Although there may not be someone that lines up *exactly* with what Varonis does, Palantir and likely Autonomy, Titus and Siemens Teamcenter are just a few examples of competition driving from different directions towards the similar end-goal of unstructured data protection. Additionally, Symantec, McAfee, IBM and others offer broadly labeled data security solutions, each doing different things and carrying different TCO price-tags.

While they had a large head start, the industry is aware that legacy controls aren’t doing a great job of protecting what really matters, data. Competitors aren’t sitting still.

My interpretation of the VRNS price action (and the downgrade a few months ago from their lead underwriter) is the market is resetting the probabilities of whether Varonis can achieve scale on its own.

Without the resources of a Cisco channel or an HP, or EMC/RSA-level (now Dell) salesforce, the odds are not with Varonis getting to the promised land on its own. The most probable scenario is it gets cheaper over an extended period as evangelical-mode sales growth levels decline until they finally start seeking strategic alternatives. The best outcome for investors may be that management accepts the end game, embraces reality, and seeks acquisition alternatives sooner rather than later. Or, they make it less of an evangelical sale. They’ve recently integrated with SIEM vendors to get closer to traditional breach monitoring and forensics IR teams. The more of this they do, the better.

Alternatively, VRNS could do a major reset to pivot towards the channel and partner with the Tatas, Accentures, Wipros, PWCs, HPs, Cognizants, etc… These are the companies who have the relationships, ability and interest to deploy this sort of organzational-encompassing solution.

But this would require enabling 3rd party pro-services, something they’ve actively resisted in the past.

Its a difficult task to build and support a services channel, and the thinking to date has been to keep the PS revenue and margin for themselves. But the tradeoff is scale and timeframe. As the growth rate slows, they will quickly start running out of options. (And competitors like Palantir, EMC, Cisco, Siemens and HP are not sitting still.)

Ultimately, what may be needed is new leadership and vision. Is current management up to the task? Maybe they’ll surprise us. Tonight will go a ways towards helping us understand where they are in turning it around.

If they can show signs of progress on this call, I’ll rapidly increase what is, for now, a highly speculative long position. They’re not executing as quickly as the market wants and their head start may rapidly be fading. The stock has been killed since its IPO, losing nearly 72% from its all-time high, trading just 8% or so above its all time low. Sentiment is terrible, expectations are low. Perhaps rightfully so. However, they’re in the right space and there is value in their solution. I can see M&A as a likely possibility.

My conclusion: I’m aware of the risk but the reward is far better here at 3x EV/Rev than it was in the $30’s. (An M&A takeout should be closer to the 10x sales level.) With 29% of the shares held short, it could be in the mid-20’s quickly with a good report.

I’m taking a swing here at $15.64, right after I hit post to the final blog. I’ll let you know how it works out. (This is thinly traded stock, just FYI.)

It’s hard to find the appropriate balance between the need to share and protect sensitive information. Too much control makes life miserable and kills business agility, whereas too little control creates risk. This conundrum is at the heart of the “shadow IT” dilemma – where users want “consumerized” SaaS solutions like gmail and dropbox that are easy to use and “just-work” – and internal IT has the opposing mandate to control data access in order to comply with regulatory requirements and manage business risk.

It’s hard to derive context from the volumes of unstructured data scattered across large user populations. Unstructured data includes Office documents, PDFs, cad-cam engineering specs, you name it, anything that’s human-generated. Most existing solutions require manual marking and self-categorization by the authors. This is cumbersome, and subjectivity & interpretation bias creates chaotic results. Building data security policies, standards & guidelines, automating compliance, implementing fast alerting & response to violations; this is where the bleeding-edge early adopters are.

Information security budgets mirror compliance regimes & governance frameworks. These regimes are only now starting to evolve, thanks to firms like Gartner, IDC & Forrester, from legacy controls that have questionable efficacy for modern threats, to data- and people- oriented frameworks.

Enter Varonis (VRNS). Up until now, unstructured data solutions have been a difficult sale into most organizations. VRNS is trailblazing a new market opportunity for focusing protection on what matters, the data.

VRNS is tackling a problem that’s so traditionally difficult, most firms frankly don’t even know where to begin. Lacking a proper toolset, IT teams do their best to lock down network access, but for all but the most conservative environments, this is mission impossible. (Lock it down so much and you kill user efficiency; ease up and you’re susceptible to APT and insider mis-use.) Once access is obtained to the network, its often a free for all. IT teams not only lack context about the data –is it important? what’s the risk?– they don’t have any visibility at all of who is accessing data, what they’ve done and whether or not it’s okay. And this environment is dynamic – across all forms of devices, clouds, folders – making it nearly impossible to monitor/enforce policy on unstructured in real time as its being created and shared. So the best of them end up buying very expensive full packet capture tech for post-breach forensics like EMC netwitness and pumping logs into SIEMs or Splunk.

I’ve worked with companies at the forefront of being fined heavily for data violations. Some are exploring combinations of tools like Teamcenter, Titus, Netwitness, Lancope, ArcSight and Splunk, but with mixed results given how manual, inflexible and limited these things are. My perspective is that VRNS looks a lot more powerful in terms of automation and scale. After 60 days, they can give IT teams enough context to find who the biz data owner and enable them to make decisions on how to lock down – and proactively monitor – high-risk data.

But the company –and its stock–have struggled mightily. Are they going to be able to turn things around?

Stay tuned for Part III and we’ll work through their challenges when it comes to execution, and the probable risk/reward in owning the stock.