Let’s run through some refiner estimates, shall we?

I am venturing into the unknown here. This is way out of my comfy space. I will assume my ideas are sound and apply equally well to refiners but I also expect to have my nose swatted if I get something wrong (that’s right, talkin’ to you, Po Pimp…).

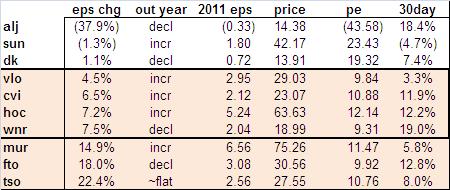

Below is a chart of 30day revisions and price action in refiners. My list of refiners comes from the “related companies” section in Google Finance under VLO and WNR. There are probably others, but I am guessing this captures the bulk of the group.

First off, I am applying an EPS sort here when EV/EBITDA is probably more relevant given how much debt these guys carry. Whatever, PE gets us in the right neighborhood.

We can quickly filter out ALJ, SUN and DK as problem children. This is not to say they really are damaged, just pointing out that Consensus is probably calling them damaged simply by looking at valuation in relation to peers. Next we look at EPS revisions made in the last 30days and see that the remaining folks can be split into two once again – those 7.5% and less, and those 15% or higher. There is a big gap in there, so we can assume the smaller numbers represent some form of sobriety. Again, not saying that estimates don’t need to be revised much higher or that they are not going to be raised much higher once earnings are announced. Just saying that if we are to look for sobriety in Consensus estimates, we probably want to screen out MUR, FTO and TSO.

This leaves us with VLO, CVI, HOC and WNR.

WNR is the famous one, of course. It’s problem is that the damn thing is up 19% in the past month. This actually concerns people, even though WNR is still the least expensive in this remaining group despite such a big rise. Notably, WNR is the only one of these four with declining EPS estaimtes into 2012 and 2013. Even with the 19% rise, it seems WNR is the black sheep of this quartet.

The other notable on here is VLO. It has not seen the estimate love, the stock is the second worst performer of the entire original group, and it is the second cheapest after WNR.

In conclusion, while I am very happy that our Good Man The Fly has focused us (…me…) on WNR and did the Good Work for us, I think I need to gander at VLO now. I need to do this by Monday since VLO reports either Monday night or Tuesday morning. Then again, maybe the past estimate/price action in VLO is trying to tell me something. I think will just let it ride and know that both estimates and stock price lag terribly in this piggy, and that if all is good then I should have plenty of time to scalp a penny or two on the report.

Yes, the latter seems the most sensible plan since WNR is already represented in my Vegas Hooker Portfolio.

One Response to “A little comp’ing”

Po Pimp

I don’t know shit about refiners and always considered them some of the most retarded companies out there. But Fly said WNR was going to be awesome so I bought it. It’s up 10% since I re-bought after banking an 8% gain earlier.

One of my goals for 2011 was to try and simplify things. Following people that know what they’re doing is part of that strategy. It’s working great so far.