Every rally needs a “tell”. Apple and Disney are fine but if you want to check the Animal Spirits of the market look to the beaten down crap.

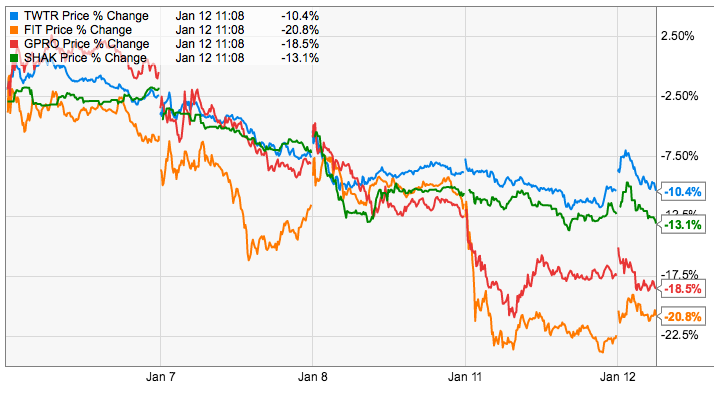

Here’s a chart of Twitter, FitBit, GoPro and Shake Shack over the last 5 days. Don’t enlarge it in front of the children unless you want them to have night terrors for 60 years.

Basket full of misery… 30 day change

4 stocks that lived and are now dying by hope. In a screaming, stupid, straight-up 10% face-ripping rally you’d want to own at least a few of these.

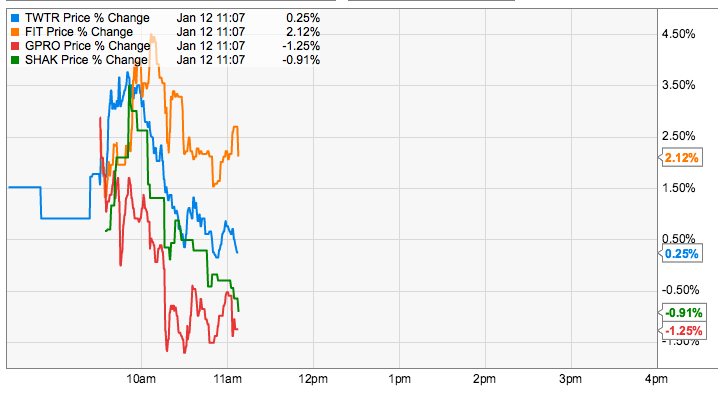

Here’s those same 4-stocks as of 8:14 hippie-time:

Hit the bid!

All way off where they opened. GoPro is a rat-infested pit of despair. You couldn’t sell enough GoPro to bid for the Silence of the Lambs house without dropping GoPro 10%. there is no demand.

That’s both rational and a warning sign for this bounce. Don’t be piggy.

McDonald’s is under attack in Europe. An Italian-based labor group is accusing the chain is abusing market power to charge excessive rents to franchisees. The group claims these higher costs are passed along to the consumer.

Via BBC: “‘McDonald’s abuse of its dominant market position hurts everyone: franchisees, consumers, and workers. We strongly urge the European Commission to investigate the charges and to use all of its powers to hold McDonald’s accountable,’ said SEIU organising director, Scott Courtney.”

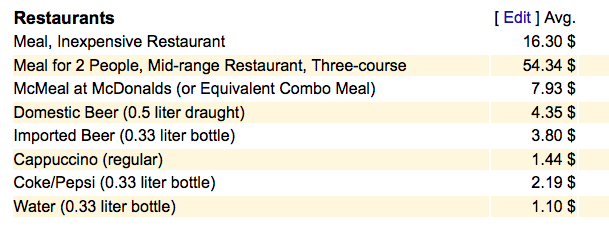

Since I’m long MCD my inclination is to dismiss the issue as fascist whining. To double check I ran a quick search. An Italian combo meal costs roughly half as much as a meal at an “inexpensive restaurant” and 1/8th as much as dinner for 2 at a mid-range eatery.

McDonald’s prices in Italy: Does this look like gouging?

It comes down to wages. Labor groups want to attack McDonald’s corporate for the same reason Willy Sutton robbed banks, “because that’s where the money is”. Unfortunately for those who prefer their solutions to societal inequality super simple, McDonald’s doesn’t set wages at a store level. Franchisees set wages at the going market rate in each location.

McDonald’s has a wage problem. That’s one of the reasons McDonald’s plans to “refranchise” (read: sell) 3,500 units. By 2018 the company will be 90% franchised in the US. Currently 3/4 of the chain is franchised in Europe, which is MCD largest market because the world loves us. McDonald’s charges franchisees a lot because running a McDonald’s is much more profitable than operating a generic pizza stand. Franchising isn’t as lucrative as it once was but it’s still a hell of a deal.

McDonald’s is much bigger than its rivals but suggesting it has monopoly powers is a reach, even by European standards.

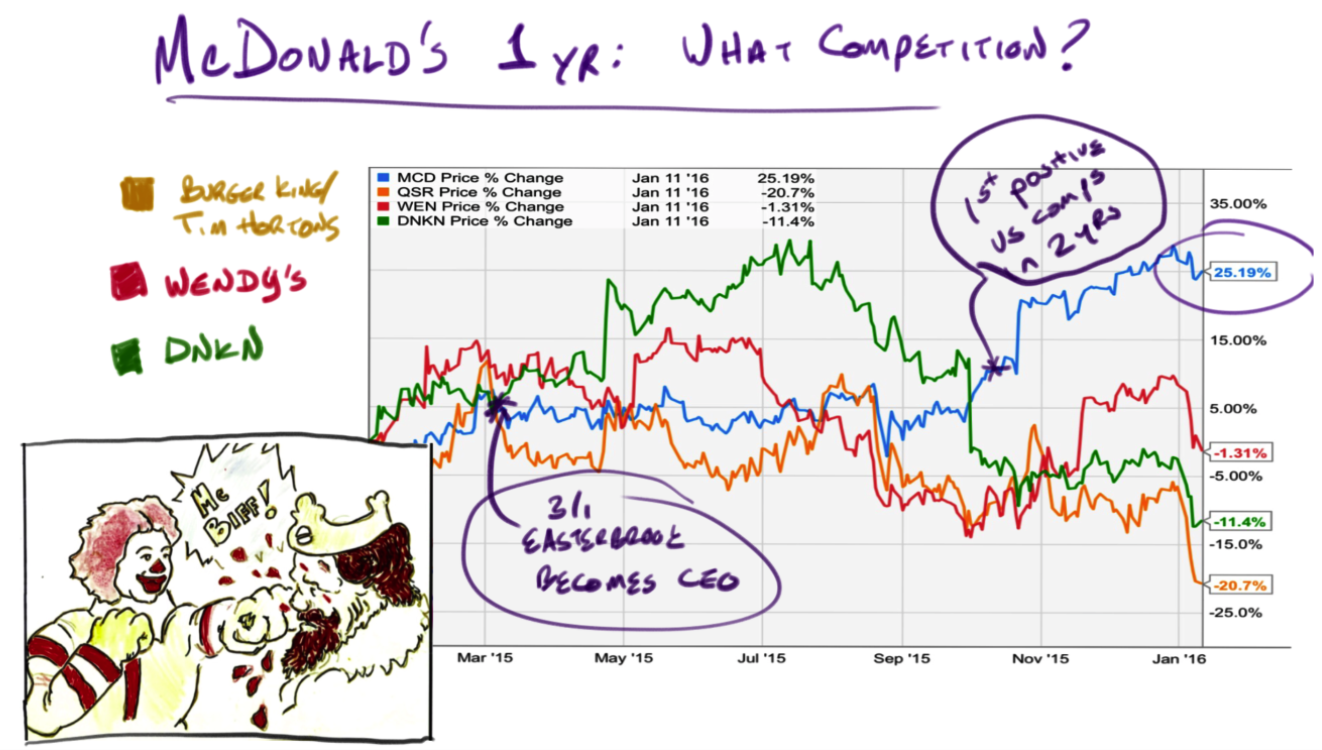

In Easterbrook We Trust

I’ve been long MCD since Steve Easterbrook became CEO on March 1st. It was a bumpy start but slowly the ship has turned. Last quarter MCD reported its first comp unit sales increase in the US in 2 years. For Q4 estimates are as high as 3.5%.

I love investing in new CEOs. If they’re good they get about a year where they can report just about anything they want in terms of earnings and still get a pass from Wall St. If they’re great the pass can get extended. It took a while for the Street to warm to Easterbrook but when SSS went positive the laggards got on board.

A little turnaround goes a very long way when you’re operating on the scale of Micky D’s. Over the last 12 months MCD is up 25%. The rest of the group has been charbroiled. Buffett and Ackman’s tax-dodging Canadian Burger King/ Tim Horton QSR has lost 20%. Wendy’s gets included just for being nearly flat. Dunkin’, included because it presumably competes for roadside “gas savings” is down 11%:

The European Commission has time to review the complaints and suggest remedies. The EU is also reviewing charges MCD is dodging taxes. If sales were falling I’d be worried. With comps expected to rise in all regions in the current period none of these protests matter.

To things keep me bullish even up 25%. First is the new CEO factor. Second, and more importantly, McDonald’s sells the best consumer product of all time. The salty perfection of the McDonald’s french fry is universal and unique. It can’t be knocked off and it is fully optimized in terms of quality. You can go anywhere in the world and recognize a MCD french fry blindfolded. It’s the same value proposition Starbucks offers, discounted for the lack of addictive caffeine.

Shares finished just under $60 afterhours, a 9% gain. Short interest is up ~50% since last summer. It was a good trade… right up until tonight when bears got their heads kicked in by a hippie yoga company with inventory control problems.

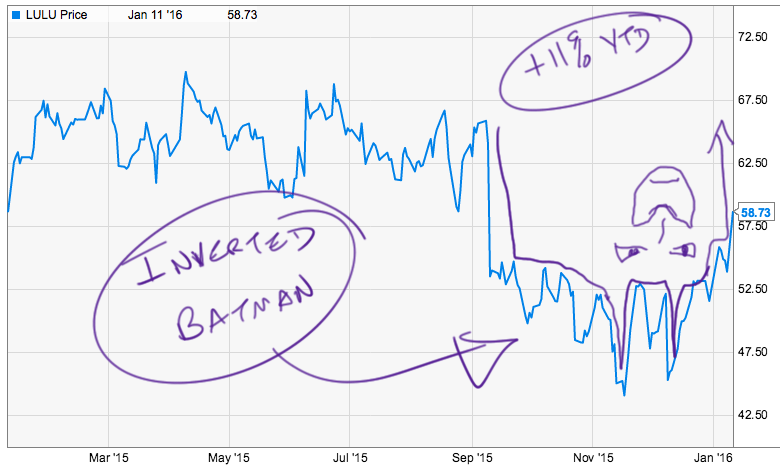

Nana na na na na na na, nana na na na na na na, Inverted Batman

Malls don’t die. Bad stores do. Lulu is likely to spend some time planking around the $60 level. The stock owes us nothing between now and when they report earnings. If you’ve been trading along don’t be afraid to book some profits.

If you’ve been fading me on the short side… Namaste.

I could make up lots of reasons. I’m a trained broadcast professional. I have an MBA from Stanford. I am practiced at the art of spouting best guesses with a confident, strong voice.

But those reasons don’t actually matter. Oil shouldn’t move 6% in one day. Oil isn’t Under Armour. It’s not FitBit. Crude should move in pennies. If oil is down 6% in one session it can only be because something in the marketplace is broken. Whatever it is if it can take oil down 6% it sure as hell can trash my shares of FaceBook.

Bear markets are hard. They take money from everyone. It’s too late to short and too early to buy. If you’re long a ton of broken GoPro et al and it’s keeping you up at night just sell it until you can relax. Otherwise, from where I’m sitting the best trade today is nothing.

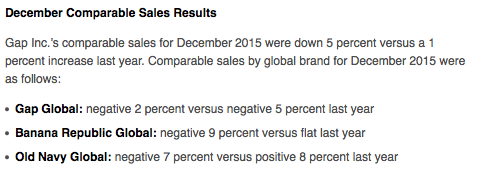

Gap pole-axed investors after the close yesterday. The specialty discount bin reported a 5% decline in same-store-sales for December. Analysts were officially expecting -3.9% but I doubt they had any idea given how promotional Gap was during the holidays.

Spying on the Gap: Black Friday

I shopped at the Gap on Black Friday. I took pictures because I’m that kind of dork. From the upper left those are pictures of Gap, Sean Connery disguised as a Japanese ninja in “You Only Live Twice” and a heap of what look like sweaters selling for 60% off at Banana Republic.

I’ve worked with the Gap. It’s a proud organization. I took those pictures at 7am on Black Friday because that’s when stores look their best for Christmas. Whoever told Gap Inc store managers to make their sales floor resemble a Haight Ashbury Salvation Army is an inept, sadistic bastard. The stores never had a chance and the store managers knew it.

I try to spy when I go to malls. I rarely buy anything and I take a lot of pictures in stores. I’m recognizable among a very select set of people, most of whom work in finance or retail so my hiding is a little absurd but I do it anyway. A little like a 6’3″ Scottish guy pretending to be a ninja.

On Black Friday I bought the Banana manager a coffee. She was looking at a month of warding off anarchy. If you’ve worked retail that table of sweaters is a ticking time bomb. The first time a customer looks for their size at the bottom of a stack it’s going to become a 60% off laundry hamper. I handed her the coffee without a word. She looked confused then smiled wanly. I may have heard a small whimper.

Anyway, Gap is an operational trainwreck and that shouldn’t be a shock. In their press release the CFO says she’s excited to bring in the spring merchandise. Here’s the thing: there’s no place to put it.

Gap came up short on revenue despite deep discounts. That means they’re still choking on sweaters and markdowns from winter.

I don’t short specialty. The stocks never go down in a straight line. Fundamentally Gap is terrible. When it turns there will be time to buy. Until then GPS is a murder pit. Yesterday the stock was up 5% before falling 8% after hours on this sales report. Specialty is a cruel mistress that way.

Retail has been strong this year. Sales were good (though most cos don’t report monthly anymore). I’m long LULU and ANF.

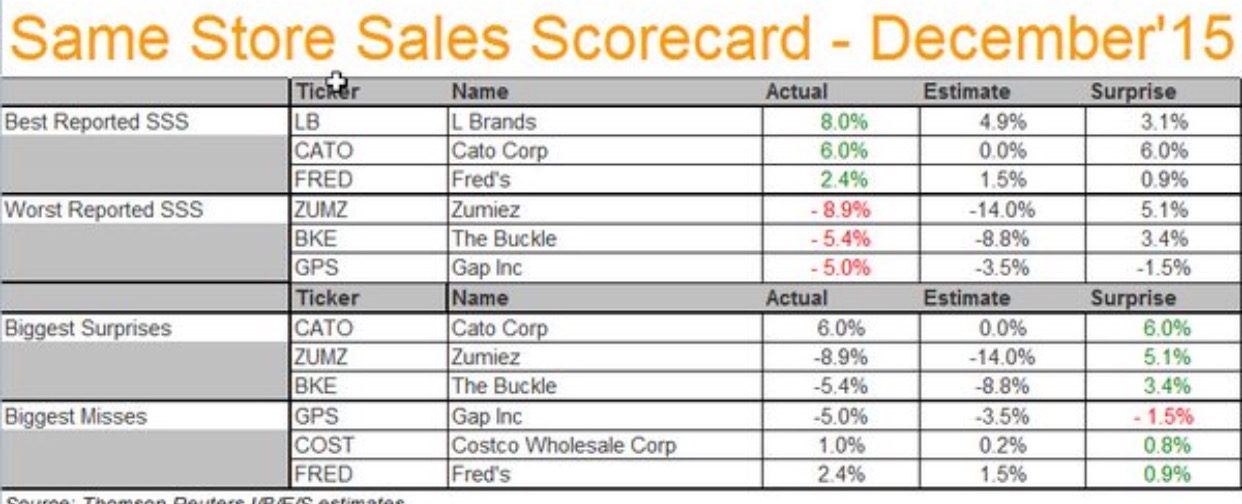

Here are the rest of the comps reported yesterday.

The analyst blamed weak sales. That’s the nicest possible take.

Macy’s liquidity problems are the result of years of systemic, moronic capital allocation. The company was an accident waiting to happen. As it turns out, that accident was the weather.

As of the end of last October Macy’s had repurchased $1.84 billion of its own shares at an average cost of $60.13. In part to help fund these buybacks Macy’s issued $500 million in debt last December. At 3.45% interest Macy’s figured it was a no-lose opportunity.

Macy’s was wrong. Shares are in the mid-$30s and the company still has to pay the juice on the debt. The bet big and wrong. In a low-margin business that’s very bad.

Macy’s is down a paper loss of about $700 million on the shares it retired. Earnings per share fell anyway. The fact that it would have been worse without the buyback isn’t really any consolation. Macy’s has guided lower twice for Q4. It now expects to make $2.18 to $2.23 compared to $2.44 last year.

The smart play for Macy’s would have been buying puts instead of all that stock and those winter jackets.

Macy’s is just begging for an activist to come in and beat some sense into the place. At best department stores have a 5-10% margin. Macy’s is much worse than that. The stock is down 50% in 6 months. That could look like a bargain a year from now.

Same Store Sales

Gap hates shareholders. That’s the only explanation for why they still release same store sales.

Gap stock was up big all day and crashed after-hours.