Buyback-Lash(TM) is picking up steam as investors sell-off shares of companies with monster buyback programs. Apple, IBM, Chipotle, Gilead… the list is growing.

The story is also picking up steam. Perhaps inspired by the Weekend Buyback Primer I created with links to pieces on AutoNation, Apple, WholeFoods Markets, Macy’s and IBM) Fortune went through Apple’s hypothetical P&L on repurchased shares yesterday:

It’s a decent read but misses the main points. Allow me to elaborate:

Repurchased Shares Go to $0 Immediately

I went over exactly why in the nuanced piece “Wall Street Street Screwed You Again! Buyback Mailbag“. It’s a nice exercise to point out that Apple is down 21% on buybacks but it misses the point.

If shares move higher after a repurchase the company has no direct benefit. Apple doesn’t trade its shares. If AAPL were trading at $200 the company itself wouldn’t be able to flip stock for a profit. Unlike literally every other potential investor corporations can’t just flip shares in the open market. The stock is instead retired to reduce share count.

In part this offsets dilution from stock option programs. That means buybacks are a good pay to hide pay and help push EPS higher all things being equal. Most executive pay packages are based at least in part on earnings per share. Buying back stock is easier than coming up with new business ideas and can lead directly to an executive team getting paid more, regardless of what the stock itself does.

Buybacks Don’t Work

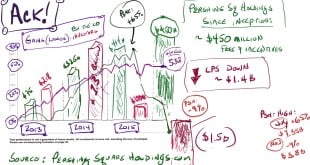

On their call last night Gilead announced it had spent an insane $10 billion repurchasing shares at an average cost of $95. As a result EPS in the fourth grew faster than net income! Ya! Everyone got a bigger chunk of the earnings pie! Gilead added another $12 billion to its $15 billion repurchase program last night. $27 billion and the company is openly accelerating buybacks right this second.

The problem isn’t that Gilead is down $10 on its investment. Gilead is down $10b but that’s not even the problem. The real issues are a) shares are going lower anyway b) that money might come in handy some day c) Gilead is competing for stock with its own investors even though Gilead has no real use for the stock.

That’s not returning cash to shareholders. It’s screwing them in the short term so your monster options package is less visible.

Yes, Gilead generates a ton of cash. So did IBM at one point. $75b in buybacks later IBM, a company once so powerful it was considered a monopoly, has missed every trend of the last decade. IBM shareholders are left with net profits of $0 since 2010.

Parade of Dunces

Financial media is like a game of telephone. Somehow has an insight then everyone passes it alone in some slightly different form. I’m not complaining or bragging about other folks picking up on this story without attribution. I expect that to happen. I just want to make sure they get it right. It’s important because investors should be insanely outraged right now and it’s not quite happening.

Among the inanity…

Chipotle spent 30 minutes detailing every margin-crushing hell that can befall a company on last night’s call. -36% comp sales, loyal customers abandoning them, promotions of unknown expense and higher costs in general. I was on the call. Shares held up fine right up until the CFO said this:

This was after the company guided to breakeven for Q1 and pulled guidance for the rest of the year because he openly has no idea how much the company will have to spend to buyback shares. How about settling the NoroVirus investigation before getting long CMG, guys? Because the stock really isn’t a buy as long as we’re synonymous with both bacterial and viral ways of contracting explosive diarrhea.

Comcast hiked buyback by $10 billion. Because the best way to fight cord cutting and ad drops is investing in your own stock.

Buybacks Need to Die Before Walmart Does

They never make sense. “Opportunistically buying back shares” is the 2016 version of Citi’s Chuck Prince blithely telling the New York Times that his bank was taking on more debt because “as long as the music is playing you’ve got to get up and dance“.

Citi still has risk to $0.

Walmart has $20b in repurchases in place. Target is buying its own stock. Amazon is not. Amazon is going into bookstores. Those are Trojan Horse distribution systems. Target and Walmart have a combined growth rate of 0%. Both chains get less than 5% of its sales from online. By Christmas Amazon will be killing them ecommerce and brick and mortar stores.

Walmart is spending under $1b developing its internet business this year. How much cash do you think there will be to return to shareholders in 10 years if Walmart doesn’t create a viable online presence?

If you enjoy the content at iBankCoin, please follow us on Twitter

Great post.

SPX 1880 is here, Next Stop SPX 1812…Us Bears Love that elevator. I agree with Doubleplus above, Great Post. Best Call Fly made was having you here.

Great thought-provoking piece. But unfortunately it will never stop.

Jeff, I’ve been following you for years and want to thank you for your outstanding work.

In this case I feel compelled to offer an alternate perspective. Share repurchases are way of returning cash to shareholders. The company could pay a dividend but that would be taxed as regular income. Alternatively, by using a share repurchase program, long term investors are taxed at capital gains rate. Of course share repurchase programs do not increase the intrinsic value of the company, and it’s not intended to, it’s intended to return cash to shareholders. If the company is worth $100 with 20 outstanding shares, it’s still going to be worth $100 with 10 outstanding shares, but theoretically the share price would have gone from $5 dollars to $10.

And of course companies that have share repurchase programs are growing more slowly than companies without them, which is due to the fundamental nature of the reason you would look to return cash to shareholders in the first place: you don’t have good growth prospects to invest that cash in.

Hi Jeff,

I had a debate with someone on this topic the other day, and through your writings, I completely agree. However, if we were to look at the other side of the coin, market logic states that if a company issues more shares, then there is share dilution and the shareholder’s shares are no longer worth as much.

But if they do a buyback, then there are less shares in the market. This person’s contention was, because a shareholder’s ownership is now worth more (theoretically speaking to the inverse theory of share dilution), this is a way to return “value” to the shareholders. My retort was that it’s not actual cash, and now the dollars are gone forever.

Is that how you would respond, if not, how? Does this persons argument hold water? Thanks in advance for all the knowledge; truly starting to do much more individual thinking.