Wells Fargo head of equity strategy, Christopher Harvey, says that if the bitcoin bubble bursts, the stock market may be toast for a while.

Harvey says the two are correlated, noting on Wednesday’s edition of Fast Money “On Monday what we saw is all risk products sell off,” and that as investors lose confidence in one major investment, such as the market, “It sometimes adds fuel to the fire” as people panic out of other asset classes.

Meanwhile, RBC analys Chris Louney sees a “fledgling” negative correlation between bitcoin and gold.

As markets continued to break all-time highs in what looks like a parabolic on a 30-year chart, investors sought alternate asset classes such as cryptocurrencies for the next rocket to the moon. Thus, the euphoria of banking coin in correlated asset classes can consequently lead to despair in both once they begin to go sideways and/or sell off.

Point in case, Monday’s epic 1,175 point selloff in the Dow was accompanied by a devastating rout in Bitcoin, which traded down to $5,947 after hitting all time highs weeks earlier. (Pop!)

“We think of it more as what we have to watch out for, what we have to … tell our clients to be careful of,” Harvey said. “We don’t make a call whether it’s going to go up or down but that it’s a risk in the marketplace, and it’s really far out on the risk spectrum.”

Wells Fargo raised its price target for equities, up about 10 percent over the next year. Its 2018 S&P 500 year-end target is 2,950, compared with the earlier target of 2,863. Cryptocurrencies and the market should trade in correlation over the next three to six months, it said.

“If we’re right, what we should see is risk product going higher,” Harvey said.

“If we’re right and risk starts to be bid again, it wouldn’t surprise us to see a bid in some of the crypto markets,” he said.

Testifying in front of Congress on Tuesday, Uber CIO John Flynn said that there was “no justification” for the company covering up a massive 2016 breach by hackers from Canada and Florida which affected 57 million accounts.

“I think we made a misstep in not reporting to consumers, and I think we made a misstep in not reporting to law enforcement,” said Flynn.

The CIO also said that it was inappropriate to have paid one of the hackers $100,000 through a “bug bounty” program to destroy the stolen data. The bounty program offers financial rewards to anyone who identifies vulnerabilities.

Flynn confirmed the man who obtained data from Uber was in Florida and that his partner, who first contacted the company on Nov. 14, 2016, to demand a six-figure payment, was located in Canada. The company’s security team made contact with both people and received assurances the pilfered data had been destroyed before paying the intruders $100,000, Flynn said. –Reuters

“We recognize that the bug bounty program is not an appropriate vehicle for dealing with intruders who seek to extort funds from the company,” Flynn said in his written testimony. “The approach that these intruders took was separate and distinct from those of the researchers in the security community for whom bug bounty programs are designed.”

Of the 57 million user accounts were compromised last November, 25 million were located in the United States. Of those, 4.1 million were Uber drivers, according to Flynn’s testimony. The hackers were able to obtain names, addresses and drivers license numbers.

Lawmakers on the Senate Commerce consumer protection subcommittee railed against the company over how it handled the breach.

“The fact that the company took approximately a year to notify impacted users raises red flags within this Committee as to what systemic issues prevented such time-sensitive information from being made available to those left vulnerable,” said subcommittee chairman Sen. Jerry Moran (R-KS).

“There ought to be no question here that Uber’s payment of this blackmail without notifying consumers who were greatly at risk was morally wrong and legally reprehensible and violated not only the law but the norm of what should be expected,” added Sen. Richard Blumenthal (D-CT).

Blumenthal also noted that Uber was in the process of negotiating a settlement with the Federal Trade Commission over an earlier, smaller breach and charges of deceptive privacy claims – while covering up the giant breach from November 2016.

U.S. federal prosecutors want imprisoned former hedge fund manager and drug company exec Martin Shkreli to forfeit $7.4 million following his August conviction for securities fraud, reports Bloomberg. Prosecutors point to his stake in Vyera Pharmaceuticals, formerly known as Turing Pharmaceuticals, along with $5 million in a personal trading account, a Picasso, and a one-of-a-kind special edition Wu-Tang Clan album.

Prosecutors say Shkreli is worth over $27.1 million.

Shkreli responded, saying that his only liquid asset is the trading account, and he owes state and federal taxes. While prosecutors say they won’t go after Shkreli’s assets until his appeals are exhausted, he does have consult with them before selling a portion of Vyera or any other asset.

“His net worth belies Shkreli’s prior representations to the court claiming undue financial hardship,” prosecutors said in a filing late Monday. “He appears to have sufficient assets to satisfy all of his debts.”

Last May the feds seized Skhreli’s WWII Enigma code machine, used by Germany to send secret messages. The machine fetched $65,000 at a Sotheby’s auction, according to a spokesman for the NY State Department of Taxation.

The Enigma machine’s seizure came seven months before federal prosecutors in Brooklyn, New York, listed it as an asset they wanted him to forfeit in connection with his criminal conviction. The seizure came four months before Shrekli was convicted in the fraud case.

Shkreli’s lawyer, Benjamin Brafman, first disclosed the Enigma machine’s seizure on Thursday in a letter filed in Brooklyn federal court that opposes a forfeiture request by prosecutors. –CNBC

“It’s like owning a gas chamber — like, what the f—?— but it’s a constant reminder that we should use knowledge for good, even if the process is ugly,” Shkreli told the magazine. “From the Pythagorean theorem to Fermat’s theorem, the math is ugly, but if you hold your nose during the process of proving it, you get to the right place.”

Shkreli named his drug company after mathemetician and cryptoanalyst Alan Turing, who cracked the Enigma machine.

The feds also sold off three documents from Shkreli’s collection. One of them was “a rare, unpublished manuscript in Latin signed by Isaac Newton at the beginning of his chemical research,” which sold for $38,000, according to James Gazzale, the tax department spokesman.

Another letter owned by Shkreli was written by English mathematician and write Augusta Ada King-Noel, the Countess of Lovelace, which fetched $26,000. King-Noel, who signed the note “A.A. Lovelace” was the only legitimate child of the poet Lord Byron.A third letter written from Charles Darwin to a man named Thomas Green discussing the publication of Darwin’s research while traveling aboard the HMS Beagle sold for $5,500.

All in all, officials raised $134,500 from the sales.

According to court documents, the 34-year-old Shkreli still owes New York State over $450,000 in taxes. His $5 million bail was revoked last September after he offered a $5,000 bounty on Facebook for anyone who could obtain locks of Hillary Clinton’s hair in order to analyze her DNA.

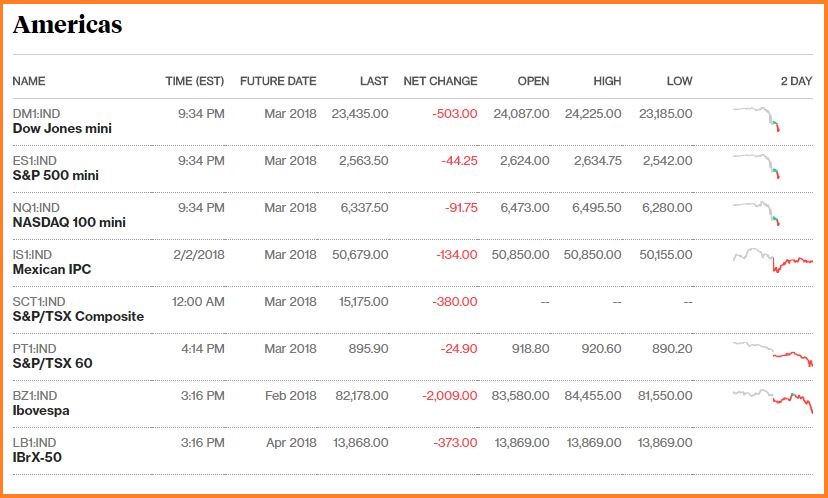

US Futures are deeply in the red tonight following Monday’s massive route which saw the Dow retreat by a staggering 1,175 points, or –4.6%.Treasury yields are meanwhile tumbling as scared money heads for the land of no returns.

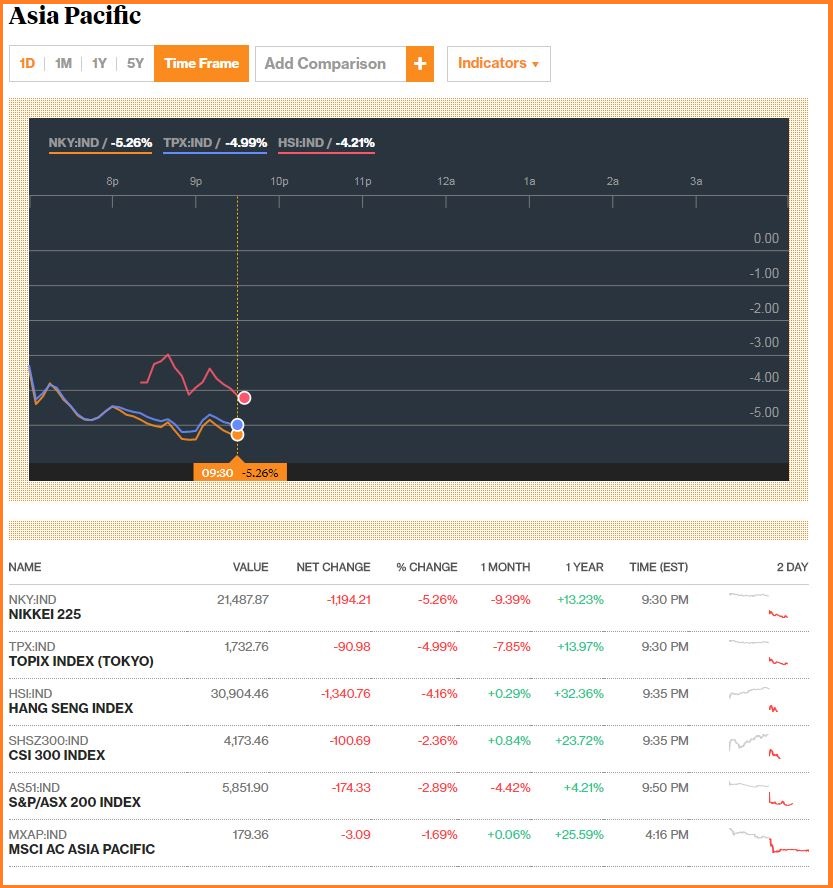

Following US markets, Asia is a bloodbath today, with the Nikkei down over 5% as of this writing.

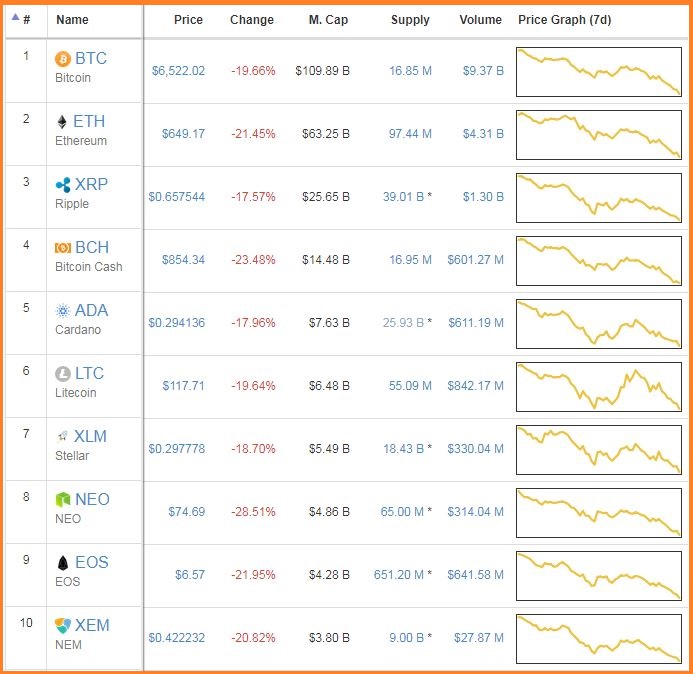

Meanwhile the Crypto complex has virtually ZERO support – with Bitcoin crashing another 19.66% to $6522. Who would have thought that a currency backed by nothing and under active suppression from governments, banks and private companies would get crushed when volatility returned. WHO. COULD. HAVE. KNOWN?

Oh, and this may just be the beginning of VIX insanity…

Via Charlie McElligott, managing director of cross-asset strategy at Nomura (via ZeroHedge)

The ETNs are the “patient zero” of this current market meltdown. It is estimated that there was anywhere from ~$125mm to $200mm of vega / VIX futs to BUY on the close from the two main “short VIX” ETNs that rebalance daily (XIV and SVXY). As S&P traded -50 handles AFTER the cash close from 4:00pm to 4:15pm into the market’s anticipation of the massive rebalancing of volatility (buy to cover) on the close, XIV then saw a delayed and terrifying ~-87 PERCENT move after the close, as some who owned XIV puts as crash protection sniffed this potential and speculated liquidation from the ETN, which is set per a rules-based system to buy back short vega after an 80% “crash trigger”(which again isn’t a certainty because they use a blend of 1st and 2nd month). The asset pool nonetheless was seemingly / largely wiped-out and the note is guaranteed to “pay out” to their shareholders as set per their prospectus. It is likely that this thing has indeed been “triggered” and will be forced to liquidate. SVXY doesn’t have the firm 80% “trigger” but too is seeing its NAV “wiped out” and is trading ~-80% post-close as well.

The issue NOW is the pile-on going-forward across assets, as the systematic “short vol” community’s models are now completely toast, and they too will be forced to cover remaining “short vol” positions that didn’t trade today—i.e. BE PREPARED FOR A MAJOR VIX FOLLOW-THROUGH TOMORROW.

Lloyds has become the first UK banking giant to ban all cryptocurrency payments on its credit cards, echoing a similar move last week by Bank of America and JP Morgan. The Lloyds banking group, which includes Halifax, MBNA and Bank of Scotland, are all affected by the new restriction.

The Lloyds group has more than eight million credit card customers, and is concerned that it may end up footing the bill for defaulting debtors should the price of Bitcoin continue to fall.

The move follows a report by the Wall Street Journal reported that Capital One banned customers from using credit cards to purchase bitcoin or coins on the Ethereum blockchain, citing “limiting mainstream acceptance and the elevated risks of fraud, loss and volatility.” Discover Financial announced it would likewise block bitcoin transactions.

In January, over $400 million in cryptocurrency was stolen after Japanese crypto exchange Coincheck was hacked.

And in yet another attempt to make digital currencies less attractive, banks have started to process cryptocurrency payments as “cash advances,” which carry extremely high interest rates. As such, Coinbase customers were greeted to this message a few weeks ago:

Dear Coinbase Customer

We’re writing because you have a credit card on file and want to inform you of a recent change that may increase the cost of purchasing digital currency with a credit card.

Recently, the MCC code for digital currency purchases was changed by a number of the major credit card networks. The new code will allow banks and card issuers to charge additional “cash advance” fees. These fees are not charged or collected by Coinbase. These additional fees will show up as a separate line item on your card statement.

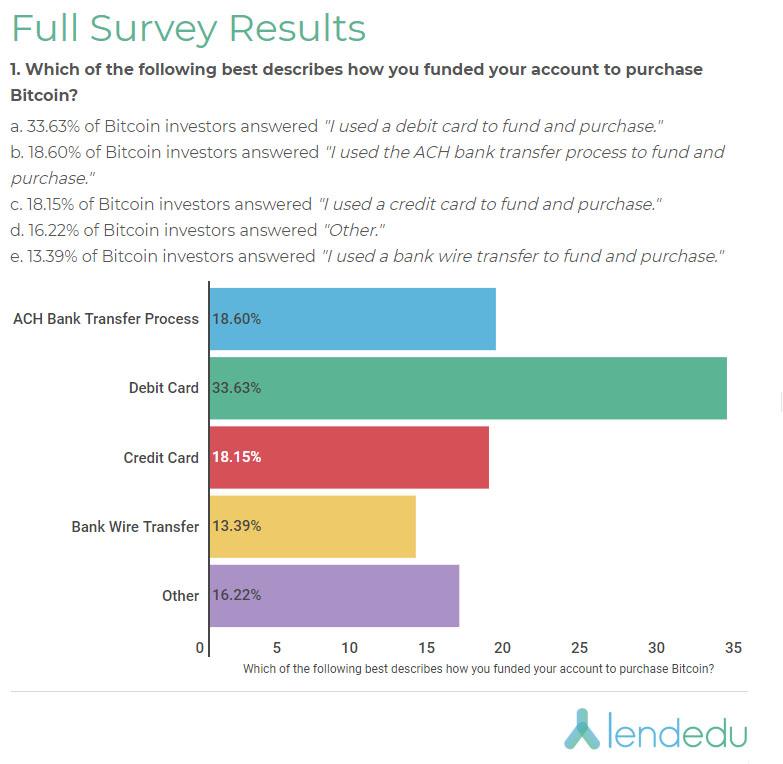

That said, credit card purchses account for just 18% of bitcoin purchases according to a poll by Lendedu:

As anyone with a computer, television or radio knows, the price of Bitcoin has been tumbling – from a December high of $20,000, to under $8,000 in overnight trade. Whether cause or effect – though we suspect the former – banks, governments, and private businsses have been cracking down on cryptocurrency speculators and suppressing demand over the last several months.

Last September, Bitcoin and other cryptocurrencies plunged as much as 20% after China banned Initial Coin Offerings (ICOs) and shuttered local Bitcoin exchanges. Chinese authorities pointed to Bitcoin’s ability to facilitate “illegal fund-raising and other types of illegal financial activities,” and “pyramid schemes, fraud and other issues.”

Last week, India said it would “take all measures to eliminate use of these crypto-assets in financing illegitimate activities or as part of the payment system.”

And on Sunday, China beefed up regulatory pressure – banning various cryptocurrency exchanges, and actively blocking crypto-related search results from search engine Baidu and social media microblog site Weibo – less than a week after Facebook created a new policy banning Bitcoin and ICO advertisements.

Bitcoin investors are claiming Australia’s banks are freezing their accounts and transfers to cryptocurrency exchanges, with a viral tweet slamming the big four and an exchange platform putting a restriction on Australian deposits.

According to the Herald, cryptocurrency trader and Youtuber Alex Saunders called out National Australia Bank, ANZ, the Commonwealth Bank of Australia and Westpac Banking Corporation on Twitter for freezing customer accounts and transfers to four different bitcoin exchanges – CoinJar, CoinSpot, CoinBase and BTC Markets.

That said, South Korea – which by some estimates constitutes 20% of the crypto trading market sent Bitcoin and the entire crypto sector tumbling over 10% in early January after the Ministry of Justice threatened a serious crackdown on cryptocurrency exchanges, South Korea’s Ministry of Strategy and Finance – a key member of the country’s cryptocurrency task force, said that it does not agree with the “premature statement” of the Ministry of Justice about a potential cryptocurrency trading ban.” This sent Bitcoin and its fickle peers surging.

“We do not share the same views as the Ministry of Justice on a potential cryptocurrency exchange ban,” MSF said according to the local Naver website.

Between the parabolic chart, banking rules, government regulations, hackers, and social media sites banning cryptocurrency ads and search results, one can hardly be shocked at the recent volatility in the crypto space.

Bitcoin fell below $8,000 this evening to a low of $7,861, erasing nearly three months of gains.

The Sunday night drop comes amid news that crypto-related advertisements have stopped appearing on Chinese search engine Baidu and social media platform Weibo, as part of sweeping crypto-crackdowns aimed at curbing speculative trading in the currency, according to cointelegraph.

Furthermore, the People’s Bank of China was told on Sunday that China will be ratcheting up regulatory pressure on cryptocurrency exchange sites and Initial Coin Offerings (ICOs), according to Chinese news outlet Sina.

In September 2017, China banned both ICOs and cryptocurrency exchanges. Some of those businesses responding by relocating off the mainland to Hong Kong. Now, Sina reports, Chinese government plans to mitigate that by banning domestic and foreign “virtual currency exchange websites.”

Meanwhile, the South China Morning Post news site reported that when the terms, in Chinese, “bitcoin,” “cryptocurrency,” and “ICO” were searched on Chinese search-engine Baidu and microblog Weibo, no obvious paid sponsored content came up alongside the expected organic results. –CoinTelegraph

Facebook similarly banned crytptocurrency advertisements last week, citing the giant number of fintech companies on the platform that are “not operating in good faith” – a move which was received favorably on Reddit’s /r/Bitcoin forum, with users commenting on the large volume of scams they’ve seen floating around social media.

In reference to scam Facebook ads, user erisiamk wrote,

“Anyone who would actually buy because they were convinced by a Facebook ad will probably not research crypto properly and end up making more bad decisions and spreading more FUD.”

On the bright side this Sunday evening, Dow futures have recovered a bit, and are only down $186 as of this writing – having been down over $300 in earlier trade.

Shares of Wells Fargo plunged over 6 percent after hours following an announcement by the Federal Reserve ordering the bank to halt its growth until it can straighten out “systemic compliance problems” which have led to consumer abuses, “until it sufficiently improves its governance and controls.”

The country’s third-largest lender with $1.95 trillion in assets will also replace three current board members by April, and a fourth by the end of the year, according to the Fed – who did not name the individuals.

“Regulators have rarely intervened directly in a bank’s operations in the past, and it is unprecedented for the Fed to order a bank to stop growing altogether, officials said. The central bank said Wells Fargo’s aggressive business strategy prioritized growth over effective risk management, leading to serious compliance breakdowns,” reports Reuters.

The @federalreserve should remove every @wellsfargo Board member who served during this scandal. I don't know what they're waiting for.

Wells Fargo president and CEO, Timothy Sloan, said “We take this order seriously and are focused on addressing all of the Federal Reserve’s concerns,” adding “It is important to note that the consent order is not related to any new matters, but to prior issues where we have already made significant progress.”

Under the terms of the Fed order, Wells Fargo must maintain an average of $1.95 trillion in assets over any two-quarter period, which Fed officials say will allow the bank to continue its normal operations while halting expansion.

In order to comply with the Fed’s ruling, the bank must submit a plan within 60 days detailing how it plans to address the Fed’s concerns, and independent third parties will conduct a review by September in order to confirm that the bank is executing on its new roadmap.

The growth halt will be in place until this review, which will be led by the San Francisco Fed and top regulatory officials in Washington, has been completed to the Fed’s satisfaction, the Fed said. –Reuters

Wells Fargo agreed to pay $190 million in 2016 to settle charges that it created millions of fake customer accounts. Then in 2017, Wells Fargo uncovered up to 1.4 million more fraudulent accounts – bringing the total up to 3.5 million potentially fake bank and credit card accounts. The bank also discovered approximately 530,000 customers were enrolled in online bill pay without their authorization.

In the wake of the scandal, several top executives left Wells Fargo, including then-CEO John Stumpf.

Former White House communications director Anthony Scaramucci unleashed on former West Wing Trump advisors Reince Priebus and Steve Bannon in an incredibly candid and revealing Vanity Fair article published Thursday evening.

In a series of three “epic” interviews with investigative journalist William D. Cohan, Scaramucci covered a tremendous amount of ground – from his humble beginnings as an Italian kid growing up on Long Island, to his time at Harvard Law, and finally on to Goldman Sachs and the world of hedge funds – which “The Mooch” says pales in comparison to DC politics.

I want you to imagine the worst person that youíve met on Wall Street, the most ruthless and the most diabolical … That’s the best person in Washington. That’s the Eagle Scout of Washington.

In order to take the job, Scaramucci agreed to sell his majority stake in SkyBridge – the New York City-based hedge fund of funds he founded in 2005.

It’s no mystery why Trump wanted Scaramucci around him. Having known each other for many years, “The Mooch” is the consummate Washington outsider; a self-made super high energy Wall St. multi-millionaire, vs the swamp creatures attempting to “handle” Trump – Bannon included as it turns out.

And even though Scaramucci originally backed Jeb! for President, Trump still invited the straight-talking Mooch into his circle of trust – giving him the job of rooting out leaks and stopping them.

Im not intimidated by Trump. I have a relationship with him. I said that to him once in the Oval: “By the way, how do you want me to talk to you? Do you want me to talk to you like youíre the president of the United States, the way these other people talk to you, or do you want me to talk to you the way I was talking to you on the campaign, or when we were friends? Tell me which way you want to go here. Obviously, when they’re around I’ll say Mr. Presidentí and all the sycophantic stuff, but when weíre alone, how do you want me to talk to you?í [Replied Trump:] You’ve got to talk to me like we’re friends.

Rancid Penis

Scaramucci delved into his experience with various DC swamp creatures, starting with former White House chief-of-staff Reince Priebus, whom he refers to as “Rancid Penis” – who Mooch refers to as a Jamoke; described in the Urban Dictionary as a “clumsy loser who is incapable of doing normal human tasks.”

“Rancid Penis, you know, he just cannot believe this. He’s just very jealous, can’t believe I’m this close to Trump. Priebus had the society broken up into “Always Trumpers” and “Never Trumpers,” and he was trying to flood the White House staff, as the chief of staff, with “Never Trumpers,” and trying to figure out ways to blockade, slow down, and keep out, particularly of the White House, the “Trumper-Trumpers.”

Originally tapped to head up the Office of Public Liaison – Valerie Jarrett’s old job under Obama, Scaramucci says Priebus tried to talk him out of the West Wing:

So, when the president turned to me and said he wanted to give me the O.P.L. job, I got a call from Reince: Don’t take the O.P.L. job. You can be the finance director for the R.N.C. Stay at your company. Blah, blah, blah. I said, No, no, no. Iím gonna take the O.P.L. job. I want to work with the president.” How many times in my life am I gonna be able to work in the White House and work for the president of the United States? And Reince’s answer was, “Actually, Iím gonna do everything I can [to help you]. He did say this because he’s a Washingtonian. Thatís what they do to you, they say, “golly gee” to your face and they act like Richie Cunningham to your face. Theyíre Richie Cunningham and theyíre Opie from The Andy Griffith Show, but they’re the fucking Sith Lord behind your back.Theyíre hitting you with a lightsaber behind your back.” In fact, according to Scaramucci, Priebus disinvited Scaramucciís parents from the January 22 swearing-in ceremony for the new White House staff. –Vanity Fair

Scaramucci says Priebus jumped all over his decision to sell his stake in his hedge fund, SkyBridge, to Chinese conglomerate HNA Group Co. Ltd. “He gets this whole nefarious research packet over to The New York Times. They love this stuff. Boom: HNA is this mysterious, nefarious company.”

Cock of the Swamp Bannon

In order to get rid of Scaramucci, Priebus reportedly enlisted Steve Bannon – another Jamoke – enticing him with a seat on the National Security Council (which lasted approximately three months before National Security adviser H.R. McMaster gave him the boot).

“Then he goes to [Steve] Bannon [then Trump’s chief strategist] and he says, I’m gonna get you on the National Security Council if that’s where you want to go, but youíve got to join forces with me and take out Scaramucci.

Scaramucci was shocked at Bannon’s betrayal. ìI helped Bannon through the three months that he was on the campaign, and we had a good relationship. But Bannon turns on me, because Bannon is ultimately railing against the swamp, but he’s actually a cock of the swamp.”

He’s the creature from the Black Lagoon, Bannon. He acts more swamp-like than any person thatís ever become a Washingtonian. So for all of his railing on the swamp, he is literally the pig in George Orwellís Animal Farm that stands on his two legs the minute he gets power. He is the creature from the Black Lagoon.

Bannon and Priebus eventually recommended Scaramucci to the role of US ambassador to the Organization for Economic Cooperation and Development, in Paris – a position which included a 17-room apartment in Paris to move to with his family. Unfortunately, that would require a lengthy Senate approval, so in the meantime Priebus found Scaramucci a desk job at the Export-Import bank in Washington.

On To Communications

While Priebus and Bannon successfully blocked Scaramucci from heading up the Office of Public Liaison, Ivanka Trump called The Mooch and set up a meeting – the topic being the White House’s copious leaks to the press, along with how to manage Trump’s image. “So I go over that day,” he said. “I go see Ivanka. They clearly don’t want Priebus to know that Iím coming. I go through the door. There’s a study off the Oval Office. Iím sitting there with the president. Ivankaís open with me. She says, “We have to re-structure.” The meeting would lead to Scaramucci’s appointment as the new White House director of communications.

Go back [to July] and look at the news cycles. What was going on was absolute berserkazoid craziness: internecine warfare, leaks every 13 seconds, Bannon leaking on everybody, Priebus leaking on everybody, total chaos in the White House, total disorganization.

After Scaramucci accepted the job, Priebus and Bannon took it upon themselves to try and talk him out of it – peppering Scaramucci with a string of desperate phone calls and text messages. When Bannon was finally able to get through, he told Scaramucci that he wasn’t fit for the job.

“You want to know what your chances are?” I said, “What are my chances, Stephen?” [Replied Bannon]: “Zero! You got that, man? Zero. You got it? Zero.” I said, “Zero, O.K., I didnít realize that the word “president” was in front of your last name, Stephen…”

The next day, Scaramucci headed over to the White House where Trump would announce his decision to name him comms director – with instructions to his senior staff that Scaramucci was to report directly to him.

In response, former Press Secretary Sean Spicer walked directly into the Oval Office and resigned.

“He comes back and he announces that heís resigned, and I said, “O.K., thatís great.” Trump’s irritated. He says, “These guys are unbelievable. I gave them the job of a lifetime, theyíre letting everybody down. Theyíre letting me down.” (Spicer could not be reached for comment.)”

The fall…

After a leak about Trump’s dinner plans was tweeted by Ryan Lizza, then-Washington correspondent for The New Yorker (who was subsequently fired for sexual misconduct), Scaramucci called Lizza to try and find out who his source was – dropping copious F-bombs, making jokes about murdering leakers, and referring to Steve Bannon in not-so kind terms.

Ryan Lizza

Much to The Mooch’s chagrin, the profanity-laced conversation was taped – which Lizza promptly turned into a profanity-laced New Yorker article which would ultimately cost Mooch the dream job that he sold out of his hedge fund to take. Lizza’s article includes such gems as “I’m not Steve Bannon, Iím not trying to suck my own cock,” and “What I want to do is I want to fucking kill all the leakers and I want to get the Presidentís agenda on track so we can succeed for the American people.”

Two days later – and a half hour or so after Reince Priebus was pushed out of his post as Chief-of-Staff and replaced by John Kelly, the New York Post ran an article stating that Scaramucci’s wife was divorcing him because she hates Trump.

Two days after that – and following an effort by Bannon to undermine Scaramucci by convincing the evangelical Freedom Caucus to complain to Trump over the profanity-laced Lizza phone call, John Kelly called The Mooch into his office and fired him, to which Scaramucci replied “Wow, that’s super disappointing.”

Scaramucci notes that his firing at the hand of Kelly did not leak to the press. Moreover, Kelly even allowed Scaramucci to leave the White House through the East Wing exit near the Treasury to avoid cameras.

Takeaways

The Mooch reflected on his very brief time at the White House;

“You want to talk about the education of Anthony Scaramucci? I learned that the swamp is probably a gold-plated cesspool with no drain. You understand what Iím saying? You canít drain the fucking thing. Itís a gold-plated cesspool, and you got cesspool operators in there that know how to slow down disruptors like Donald Trump.”

On Trump, Scaramucci says that “one Trump tweet more than any other sums up the man: “My button is bigger than your button.” He said, “If you really know the guy and you know how he’s raking it over everybody and breaking everybody’s balls, it’s like laugh-out-loud funny.”

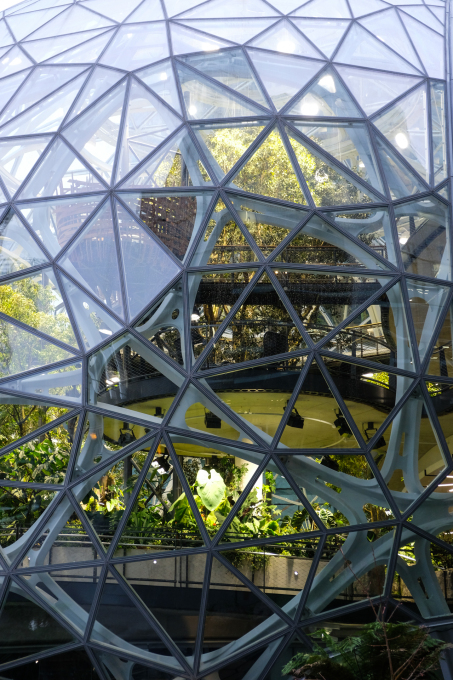

Amazon unveiled a rainforest-like office space on Monday for Seattle employees who want to be one with nature while conducting meetings and going about company business in “organic” office spaces – such as a giant nest.

The giant glass structures, called the “Spheres” feature a 90-foot tall central sphere that’s 130 feet in diameter, which is flanked by two smaller spheres.

“The idea is that we connect them with nature,” said Amazon’s lead horticulturist Ron Gagliardo. “We get them away from their normal desk environment so you don’t see any desks or cubicles around.”

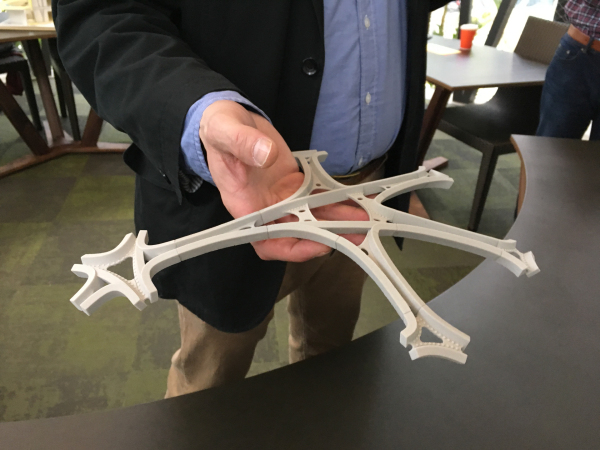

Designed by Seattle architecture firm NBBJ, the complex features 2,643 glass “facet” window panes, reinforced internal structures they call “Catalans”

The complex can house up to 800 Amazon employees, and will feature over 40,000 plants from 400 botanical species, tree-house meeting rooms, waterfalls, a river, and of course – the nest.

“We wanted to create something really special, something iconic for our campus and for the city of Seattle,” said John Schoettler, Amazon’s vice president of global real estate and facilities, during the opening ceremony

While the buildings will only be open to Amazon employees (unless you go on a company tour), shops by the entrance will be open to the public.

Earlier this month, Amazon unveiled the 20 finalists for its coveted second headquarters. Cities including Los Angeles, New York and Washington, D.C. are among them. –USA Today

In mid-January the online retailer narrowed down its pick for a second headquarters from 238 cities to 20, including Boston, New York and Austin, Texas. The company plans to pick a winner later this year.

The company has invested $3.7 billion on infrastructure and buildings between 2010 and mid-2017, and says it plans to invest over $5 billion to construct HQ2 – which should create as many as 50,000 jobs.

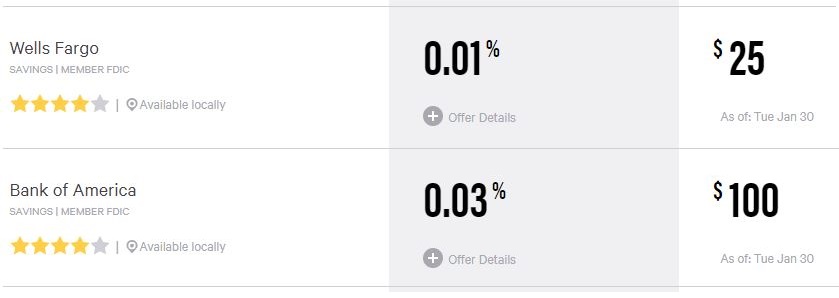

Big banks such as JPMorgan, Wells Fargo, Citigroup and Bank of America have been shafting depositors with terrible interest rates – refusing to keep pace with the Federal Reserve’s rate hikes.

JPMorgan, for example, has only raised its average deposit rate by 0.21 of a percentage point, despite the Federal Reserve raising rates by 1.25% over the same period – effectively punishing customers by locking them into historically low rates required to bail out the same banks which caused the financial crisis a decade ago.

The trend is so remarkable that analysts at Goldman Sachs Group Inc. (GS – Get Report) , a rival Wall Street firm with a comparatively tiny banking franchise, published a report on the matter earlier this month, noting that rates on savings were “virtually untouched” in 2017, even as banks charged fatter payments on loans and other assets whose rates jumped along with the Fed’s increases.

Consequently, a decade after the 2008 crisis, retirees and others who shun stocks and choose less volatile, government-insured savings accounts at big banks are still getting meager returns. –TheStreet

“Some of the big banks literally have not moved deposit yields higher at any time during this cycle of Fed rate hikes,” said Greg McBride, the chief financial analyst at BankRate.com, which tracks the savings and lending industry.

In fact, none of the Fed’s three rate hikes noted by Goldman were passed on to savers at JPMorgan, Bank of America and Wells Fargo, with Citigroup passing along just 4% of the rate increases, or 0.03 of a percentage point.

Goldman’s takeaway? Shareholders in big U.S. banks are “not to worry,” Goldman wrote in the Jan. 8 reports. “Large banks are still raising cheap funds.”

To review; Home lenders and “too big to fail” banks conspired with lawmakers to remove the Glass Steagall act, allowing banks to commingle investment and retail banking operations and making them “too big to fail.” Said banks then went on a drunken lending spree as politicians like Barney Frank pushed affirmative-action lending practices, while insisting that Fannie Mae and Freddie Mac were in great shape. This was very disrespectful to the stability of America’s financial institutions.

Of course, in order to keep banks alive, the Fed had to use trillions of taxpayer dollars and drop it’s target rate to a historically low zero percent to avoid what Ben Bernanke and Hank Paulson warned Congress was sure collapse were they not to act quickly.

And now – the same banks which created the crisis and then took taxpayer money during the crisis, refuses to reward savers now that the crisis is “over” (until it’s not) – driving up profits as they use the cheap deposits to fund loans written at the new, fed-hiked rates.

Partly as a result, JPMorgan’s net interest income – the difference between what it makes on loans and other interest-earning assets and what it pays out on deposits and other borrowings – jumped to $50.1 billion in 2017 or a 15% increase from 2015 levels.

For “retail, checking and core savings, there’s been little to no movement” on deposit rates, Marianne Lake, JPMorgan’s chief financial officer, confirmed to bank-stock analysts this month on a conference call.

She signaled that regular depositors might again see little improvement in 2018 on their savings rate, at least relative to the Fed’s expected rate increases of 0.5 percentage point to 1 percentage point.

“My expectation, just given where we are, in the absolute level of rates, is that on the retail space, we would still see a lot of discipline,” Lake told the analysts. –TheStreet

Smaller banks are the place to be

According to BankRate’s McBrde, higher deposit rates can be found at smaller banks and online financial institutions, which have been forced to pay higher rates to attract deposits. “They don’t have a branch on every corner, ATMs everywhere and their name on the stadium,” said McBride, adding “You’re not going to be able to out-market the big banks, so you pay a higher rate on deposits and compete that way.”

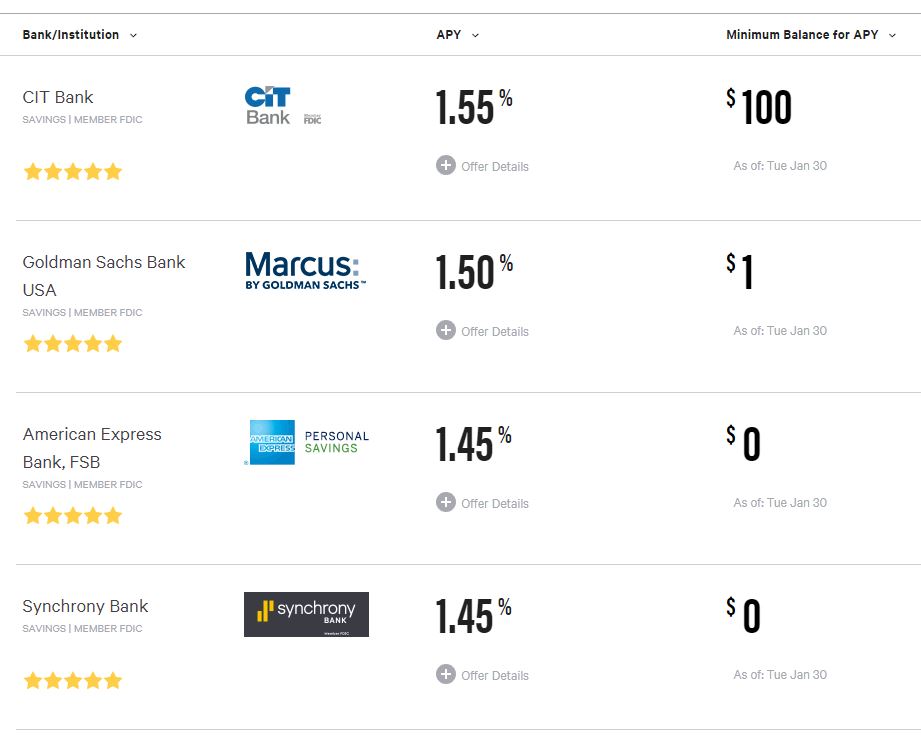

According to Bankrate, the top four savings rates can be found at CIT Bank, Goldman Sachs’ Marcus Bank (which wrote the analysis referenced in this article), American Express, and Synchrony Bank – the largest provider of private label credit cards in the US to brands such as Amazon, Walmart, Lowe’s.

Meanwhile, Wells Fargo and Bank of America clock in near the bottom of the list.

Bank of America CEO Brian Moynihan justifies his bank’s crappy deposit rates by pointing to all of the wonderful services and conveniences offered by their savings accounts, which apparently can’t be found elsewhere. Moynihan also points to an increase in average checking account balances – suggesting that savers are more interested in safety than return on capital.

Citigroup CFO John Gerspach said that the low deposit rates are a “reflection of the state of competition” between banks. “Given deposit rates have been largely unchanged following the December 2017 hike, strong industry deposit growth suggests larger banks continue to have little problem raising cheap funds,” wrote the Goldman analysts.

In previous periods, top-yielding savings accounts kept pace with the Fed’s increases, and would anticipate rate hikes by competitively raising their own payouts in advance according to McBride. Now, the top payers have a correlation with the fed of around 0.5, and the rates are dismal.

If and when the much talked about volatilityrears its head in 2018, any hopes savers had of higher rates on their cash will be sadly disappointed.

Wells Fargo head of equity strategy, Christopher Harvey, says that if the bitcoin bubble bursts, the stock market may be toast for a while.

Wells Fargo head of equity strategy, Christopher Harvey, says that if the bitcoin bubble bursts, the stock market may be toast for a while.