A friend recently sent me this publication from Empiritrage: Volatility-Based Allocation. I encourage reading the document as the strategy is interesting, and a basic understanding of what they are testing will be necessary to understanding my article.

The general idea behind the strategy is to use two $VIX moving averages (10 and 30 day) and a 12 month moving average (250 day) to create Risk-on, Risk-off regimes for 5 asset classes:

- SP500 Index ($SPY)

- FTSE NAREIT All Equity REITS Total Return Index—benchmark for REITs ($IYR)

- MSCI EAFE Index—benchmark for investment in equity markets outside of U.S. and Canada ($EFA)

- MSCI EEM Index—benchmark for investment in emerging markets ($EEM)

- Merrill Lynch 7-10 year government bond index ($IEF)

A quick glance at slide 3 of the publication will provide a graphic presentation of how VBA works.

The backtested results presented in the publication were decent enough for me to consider adding VBA to my own portfolio. But before doing so, I wanted to see what would happen if tradeable securities were used instead of the total return indices (which are not able to be bought and sold).

I’m not sure what to make of the dividend distributions that are part the total return indices but not the price indices. My data is all price indices, meaning it is dividend adjusted. In real life, would trading in and out of $SPY or other tradeable asset classes mean missing some dividend distributions? I think it would, and I’m not sure how Empiritrage took that into account. I have sent them an email with a link to this post in case I have erred or in case they want to provide some clarity.

We can assume, since I will be using price indices (ETFs, actually) for testing the system, that my results will not be as good as their results since dividends will not be included. Other considerations are that ETFs do not perfectly track their underlying indices and can be subject to bid/ask and liquidity issues. I am also including a return on cash via $SHY (iShares 1-3 Treasury Bond ETF), but I have not calculated the return the same as Empiritrage as they used T-Bills. My goal is to test how VBA would work in real-life for a real person who chooses to manage his or her long term accounts. I will test the strategy over the data and securities that such a person is likely to have available.

Backtested Results

I will present my results much the same way Empiritrage did, for the sake of easy comparison. All results are frictionless, meaning commissions and slippage have not been included. Trades are made and portfolios are rebalanced once a month, on the first trading day of the month.

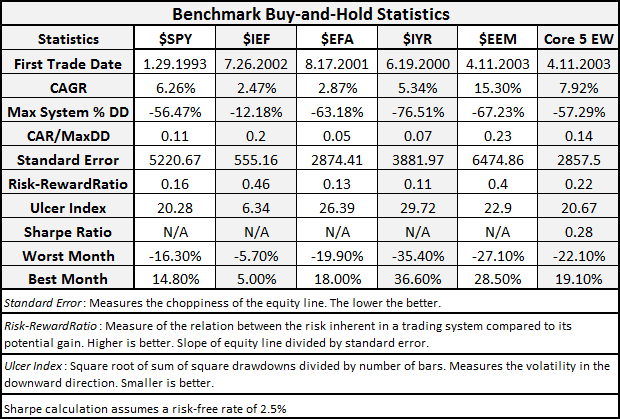

It has been a rough decade for these asset classes. While $EEM returned 15.30%, its maximum system % drawdown was a killer. The Core 5 EW, which is simply all five classes held in equal weights, also had a killer maximum drawdown. What Empiritrage is seeking to accomplish is to replicate the returns without the risk.

Let’s see if their volatility-based allocation strategy is able to do that.

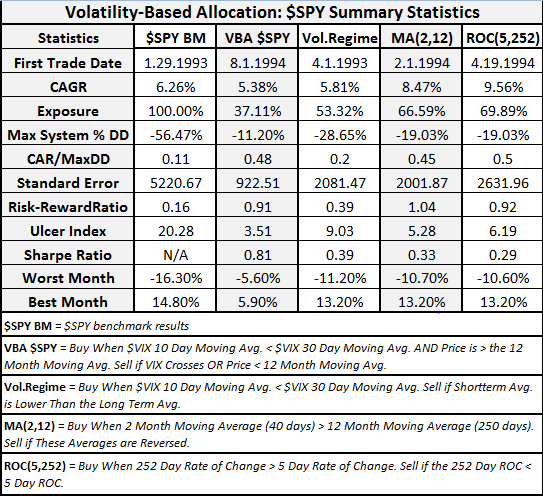

The volatility-based allocation (VBA $SPY) was able to come close to the $SPY benchmark return while significantly lowering risk metrics.

- Exposure was reduced by roughly 60%

- Maximum System % Drawdown was reduced by 80%

- Sharpe Ratio more than doubled compared to the other strategies.

If the goal is to beat the S&P 500 and include some downside protection, the ROC(5,252) and MA(2,12) have accomplished it. But with increased CAGR comes increased risk. I do not think it is possible to separate the good from the bad, but the VBA strategy shows on $SPY that it is possible to keep most of the good and throw out most of the bad.

The Volatility-Based Allocation Equity Curve

Click on the charts to make them bigger…

Upon seeing the equity curve, I started thinking that it would be hard to stick with this system from 2003 – 2006 when the market was steadily trending up and the system was losing money. And therein lies the system trader’s dilemma.

The next post will take a look at how this strategy has worked with the other 4 asset classes, and will then run the strategy over all 5 classes equally weighted. If there are any questions, please let me know in the comments. I have glossed over quite a few of the specifics in order to make this post manageable.

Exit question: Is the market making a huge triple top?

Comments »