[youtube://http://www.youtube.com/watch?v=IlY9C6pzxKc#t=12 450 300]

Comments »PPI Inflates Faster Than Expected

“U.S. producer prices rose more than expected in June with gains across most categories, pointing to some inflation at the factory gate.

The Labor Department said on Wednesday its producer price index for final demand increased 0.4 percent last month, reversing May’s 0.2 percent decline.

Economists polled by Reuters had forecast prices received by the nation’s farms, factories and refineries rising only 0.2 percent.

The government revamped the PPI series at the start of the year to include services and construction. The new series was viewed as an alternative measure of economy-wide inflation.

But big swings in prices received for trade services, a gauge of margins for retailers and wholesalers, have injected volatility into the series and made it difficult to get a clear read on producer inflation.

The dollar widened its gains against a basket of currencies after the data. U.S. stocks were set to open higher.

Inflation is edging higher, with key consumer price measures rising in both May and April, even though the main gauge watched by the Federal Reserve continues to run below its 2 percent target.

The U.S. central bank is widely expected to start raising interest rates in the second half of 2015, but labor market strength poses the risk of an earlier policy tightening.

Fed Chair Janet Yellen cautioned on Tuesday that the Fed could raise interest rates sooner and more rapidly than currently envisioned if the labor market continued to improve faster than anticipated by policymakers…..”

Comments »U.S. Economy Not Recovering Fast Enough From Overall Malaise & Polar Vortex

“The economy is recovering from a harsher-than-normal winter, but the pace of growth for the balance of this year and next will not create nearly enough decent jobs for the millions unemployed and recent graduates working at venues like Starbucks.

It’s easy for President Obama to blame Republicans in Congress, and vice versa, and for both to put their hopes in the Federal Reserve’s stewardship of monetary policy, but decades of bad trade, energy and education policies pursued by both parties have torpedoed prosperity.

A succession of trade agreements has opened U.S. markets to foreign manufacturers in Asia, whose governments continue to erect high barriers to competitive American products. Meanwhile, federal policies limit oil and gas development off the Atlantic, Pacific and Eastern Gulf Coasts.

The United States has chosen to pay its way in the world with exports of knowledge-intensive services, but the math doesn’t work. The annual international trade deficit on manufacturers and oil is approximately $615 billion, whereas the surplus on services is well less than half that amount.

Although knowledge-intensive juggernauts like Google and Citigroup create high-paying jobs in science-based disciplines and finance — and America still has notable knowledge-intensive manufacturers in industries like pharmaceuticals — those simply don’t create the growth and numbers of high-quality jobs lost to the surge of imported cars, coffee tables and computers.

Since the beginning of this century, the economy has grown 1.7 percent annually and created only 6 million jobs, compared with 3.4 percent growth and 41 million jobs during the Clinton-Reagan prosperity.

Also, the knowledge economy requires workers with very different skills than the industrial age did. It places a premium on specialized technical expertise and a capacity for self-directed learning, permitting workers to jump from employer to employer as new technologies create and destroy industries and jobs. Compared with 25 years ago, consider how many web designers and how few print journalists we have today.

What jobs the economy creates are either in the well-paying knowledge economy or in low-paying activities like restaurants, residential cleaning services and the produce aisle at Whole Foods.

Our educational system produces enough great scientific minds but not nearly enough technically sound folks with old-fashioned “get up and go”….”

Comments »

Industrial Production Drops, Misses By Most Since January

“For the 3rd month in a row, Industrial Production missed expectations as hopes and dreams of follow through in Q2 remain dashed on the shores of hard data. IP rose 0.2% (missing the 0.3% expectation) and May’s jump was downwardly revised to 0.5%. What is stunning is that Industrial Production has slowed its gains from the polar-vortex Q1 ….”

Comments »BRIC Nations to Create $100bn Development Bank

“The leaders of the five Brics countries have signed a deal to create a new $100bn (£583m) development bank and emergency reserve fund.

The Brics group is made up of Brazil, Russia, India, China and South Africa.

The capital for the bank will be split equally among the five participating countries.

The bank will have a headquarters in Shanghai, China and the first president for the bank will come from India.

Brazil’s president, Dilma Rouseff, announced the creation of the bankat a Brics summit meeting in Fortaleza, Brazil on Tuesday.

A new player

At first, the bank will start off with $50bn in initial capital.

The emergency reserve fund – which was announced as a “Contingency Reserve Arrangement” – will also have $100bn, and will help developing nations avoid “short-term liquidity pressures, promote further Brics cooperation, strengthen the global financial safety net and complement existing international arrangements”.

The creation of the Brics bank will almost surely create competition for both the World Bank and other similar regional funds….”

Comments »Did Israel Collude With ISIS to Justify Gaza Attack?

[youtube://http://www.youtube.com/watch?v=EfRyXnKbpaQ#t=82 450 300]

Comments »The Gaza Bombardment – What You’re Not Being Told

[youtube://http://www.youtube.com/watch?v=iXRO1YFreNA 450 300]

Comments »Hedge Fund Managers Load the Equities Boat

“While some investors have been scared away by the stock market’s continuous climb to record highs in recent weeks, hedge funds apparently aren’t among them.

Hedge funds that deploy a “market neutral” strategy, meaning they typically hold equal amounts of long and short stock positions, were 18 percent net long as of July 2, according to Bank of America Merrill Lynch, CNBC reports. That compares with 10 percent net long two weeks earlier.

The funds are emphasizing growth and small-cap stocks in their long exposure.

Macro funds, which bet on macroeconomic trends through all kinds of asset classes, also have raised their long exposure to stocks in the S&P 500 and Nasdaq Composite indexes, according to the report….”

Comments »El-Erian: What Yellen Can’t Tell Congress About Rates

“By Mohamed A. El-Erian

Some major questions stand out as Federal Reserve Chair Janet Yellen heads to Capitol Hill for her semi-annual testimony to Congress: particularly, when should the Fed start raising interest rates, and are its unconventional stimulus efforts contributing to a financial bubble?

Unfortunately, neither Yellen nor anyone else is in a position to provide decisive answers at this stage.

Watching for Bubbles

With the unemployment rate falling faster than the Fed expected, and with the end of the extraordinary bond-buying program (known as quantitative easing) currently slotted for October, some officials — including Philadelphia Fed President Charles Plosser, St. Louis Fed President James Bullard and, more surprisingly, San Francisco Fed President John Williams — have publicly wondered whether the central bank should move more quickly to start raising interest rates. They worry that failing to do so would increase the probability of problems down the road, particularly when it comes to inflation.

Others, including Yellen, note that significant “slack” remains in the job market: A historically low percentage of the population is participating in the labor force, and too many people are working part time for lack of better options. These Fed officials also want to do whatever they can to counter the risk that long-term unemployment will become even more entrenched, eroding the economy’s productive capacity and its responsiveness. Given the still-anemic growth in wages, they don’t see inflation as an imminent threat.

A related issue has to do with the impact of all of the Fed’s unconventional policies not only on the economy but also on financial markets — or what former Fed Chair Ben S. Bernanke called the balance of “benefits, costs and risks.” The experimental policies are intended to push up the prices of stocks, bonds and other financial assets to high levels, in the hopes that the resulting optimism among consumers and companies will cause economic fundamentals to catch up.

Some within the Fed think that the risk of bubbles in financial markets has become too great — that they have gone beyond what the economy will be able to justify. Their concerns extend beyond the high valuations and low volatility of all sorts of assets, including hard-to-trade ones. They also worry about the behavioral changes that come with excessive financial laxity, such as complacent lending with too-lenient conditions, irresponsible bond issuance and the excessive use of borrowed money — or leverage — to boost returns.

Again, Yellen is among those who appear less concerned at this stage. While aware of the risk of bubbles, they think that the problems are isolated: Most would be alleviated by a stronger economic recovery, and the rest could be mitigated by so-called macro-prudential policies designed to improve the resilience of the financial system.

Ideally, Yellen could use her congressional testimony to narrow the differences between the two camps. But Fed chairs typically don’t employ the occasion to dissipate new ideas that haven’t already been discussed at a high level in the central bank and, more important, there still isn’t enough evidence to make a conclusive analytical case for either side…..”

Comments »Should We Even Worry About Potugal’s Banking Woes?

$GS & $JPM Manage to Beat Net Profit Estimates

June Retail Sales Fall Right in Line With Q2 Bust

“Following disappointing retail sales number for both April and May, or two thirds of Q2, there was hope that June would finally be the month retail sales would soar. Alas, that would not be the case, following the release of the latest retail sales data by the Department of Commerce which reported that in June retail sales rose just 0.2%, well below the 0.6% expected and matching the lowest end of the forecast expectations (from 0.2% to 1.1%).

Misses were also reported for retail sales ex-autos (0.4%, Exp. 0.5%) and ex-autos and gas (0.4%, Exp. 0.5%). Perhaps the only saving grace was the upward revision of May data from 0.3% to 0.5% for the headline number and from 0.0% to 0.3% for the ex-autos and gas. If anything, however, today’s retail sales increase which was the slowest in 5 months confirms that the trend we warned about in April, namely that the US consumer tapped out in March to fund that month’s mad spending spree, and the spending trend has been deteriorating ever since.

There was some good news in today’s report which was the retail sales control group, which rose 0.6% compared to estimates of 0.5%, and the May revision of 0.0% to 0.2% means that GDP beancounters will likely end up adding a few basis points to their Q2 GDP estimate even as consumers enter Q3 in the weakest shape they have been since the polar vortex.

Finally, the breakdown of retail sales by business was rather paradoxical….”

Comments »Is it Time to Invest Globally ?

“Last week, I listed concerns of a stock market correction in the U.S., including high valuations and a weaker-than-expected economy. Investors seemed to acknowledge those risks, as stocks drifted steadily lower on the week.

At the same time, European equities had a shock as the solvency of a major Portuguese bank was called into question. Shades of the 2011 European debt crisis spooked investors, and stocks across Europe slid.

With trouble in developed markets and yields on interest-bearing assets still paltry — and perhaps threatening to drift even lower given recent trends with the 10-year Treasury — then where is an investor to turn?

I say go global — and start staking out a position in emerging markets. The valuations are much cheaper, the momentum is much better and there are some very attractive ETFs that allow you to play the upside potential in these volatile regions but with enough diversification to reduce your risk significantly.

Here are three such emerging market ETFs I’m watching now:

iShares MSCI Taiwan Index ETFEWT -0.31%

• 60-day return: 11%

• 2014 return: 13%

• Net assets: $3.3 billion

• Expense ratio: 0.62%, or $62 on every $10,000 invested

Many emerging market stocks and ETFs have picked up nicely since their May lows, outperforming the S&P 500 in that period. But one region that has actually outperformed all year long is Taiwan…..”

Comments »Should Individual Investors Zig Instead of Zag?

“Main Street and Wall Street are moving in opposite directions.

Individual investors are plowing money back into the U.S. stock market just as professional strategists say gains for this year are over. About $100 billion has been added to equity mutual funds and exchange-traded funds in the past year, 10 times more than the previous 12 months, according to data compiled by Bloomberg and the Investment Company Institute.

The growing optimism contrasts with forecasters from UBS AG to HSBC Holdings Plc, who say the stock market will be stagnant with valuations at a four-year high. While the strategists have a mixed record of being right, history shows the bull market has already lasted longer than average and individuals tend to pile in at the end of the rally.

“If Wall Street, after poring over all known data, comes up with a target and we’re already there, and you still see individual investors buying and they’re typically the ones that are late to the party, it would seem there is limited upside,” Terry Morris, a senior equity manager who helps oversee about $2.8 billion at Wyomissing, Pennsylvania-based National Penn Investors Trust Co., said in a July 8 phone interview.

U.S. stocks slid from record highs last week, sending the Standard & Poor’s 500 Index to the biggest drop since April, amid concern over financial stress in Europe and the timing of higher U.S. interest rates. The Chicago Board Options Exchange Volatility Index jumped 17 percent from a seven-year low.

Steady Gains

The S&P 500 is still up 6.5 percent for 2014, compared with a 3.5 percent advance in the Bloomberg Commodity Index of 22 raw materials and 3.3 percent gain for the Bloomberg U.S. Treasury Bond Index.

For most of this year, equity investors have seen little volatility and steady gains, giving them confidence to put money back into the market. Individuals deposited about $9.5 billion in June to stock funds and have added cash in eight of the past 10 months, data compiled by ICI and Bloomberg show. That’s a reversal from the five years through 2012, when $300 billion was withdrawn.

Professional investors, such as Nick Skiming of Ashburton Ltd., say that individuals investors are attracted to stocks after seeing others getting rich from a big rally, a time when equities are usually overpriced. The bursting of the technology bubble in March 2000 was marked by mutual funds absorbing a record $102 billion in the first quarter.

Blue Skies

“As institutional investors, we’re always concerned when the retail investor is actually arriving in the market,” Skiming, who helps manage $10 billion at Ashburton, said by telephone from Jersey, the Channel Islands. “The retail investor arrives when they can only see blue skies.”

For Laszlo Birinyi of Birinyi Associates Inc., stocks have entered what he calls the exuberance phase…”

Comments »Is $C’s Settlement Charge a Way to Hide Declining Revenues ?

“Earlier today, moments after hearing that Citi would incur a near-record $3.8 billion Q2 charge as part of a $7 billion settlement for the US investigation into its fraudulent MBS sales in the pre-Lehman period, an announcement which came literally minutes before its Q2 earnings announcement, we knew precisely what was about to happen:

Sure enough, moments after we sent this out we learned that Citi magically beats consensus EPS of $1.05, reporting a non-GAAP number of $1.24. The only problem: reported GAAP EPS was a laughable $0.03. Where did the bulk of the company’s net income come from? Why the “one-time, non-recurring charge” of course: $1.21 of the $1.24 in Citi EPS was thanks to the “punishment” the government just served it with.

And since Wall Street, all of it in the same boat as well, does not care about actual numbers based in reality, but merely pro forma adjustments, such as this one which was a kitchen sink addback for Citi, allowing it to generate $3.8 billion in pro forma “Net Income” when in reality none of this is an actual cash flow item, and certainly does not benefit the balance sheet, Citi stock is now a solid 3% higher on, well, magic!

In reality what happened: Citi’s revenues dipped 4%, and 5% for Citicorp excluding Citi Holdings….”

Comments »Trading Revenues Hit a Pitfall, Will it Be Permanent?

“UBS AG UBSN.VX +0.92% ‘s trading floor in Stamford, Conn., once teemed with traders occupying a space equal to two football fields. The Guinness World Records recognized it as the biggest such facility on the planet. And the Swiss bank used it to showcase its Wall Street credentials.

Stu Taylor, a former UBS managing director in trading who now runs trading-technology company Algomi Ltd., remembers when guests were brought around the gallery regularly. “It was very much a showpiece,” he said.

Today, there are virtually no traders shouting into their phones or staring at terminals. UBS’s cavernous floor is taken up mostly by back-office, legal and technology staffers, according to people familiar with the bank.

A spokeswoman for UBS said the trading floor was built for 1,400 traders, but wouldn’t disclose the number of employees at the facility.

A deep slump in trading activity in everything from stocks and bonds to currencies is changing the face of Wall Street. Businesses that once contributed disproportionately to the revenues of the world’s largest banks are now bleeding jobs and sparking fears of a permanent decline.

Today’s markets are “boring,” said Thomas Thees, a former head of North American credit trading at Morgan Stanley MS -0.85% and a former co-head of fixed income at Jefferies Group. “This is affecting the opportunity to make money, and ultimately the earnings these [trading] businesses can provide.”

Global revenue from trading in fixed income, currencies and commodities, or FICC, dropped to $112 billion last year, down 16% from a year earlier and 23% from 2010, according to Boston Consulting Group.

As big banks with large trading operations such as J.P. Morgan Chase & Co., Goldman Sachs Group Inc. GS +0.84% and Citigroup Inc. report second-quarter earnings results this week, investors and analysts will be trying to find out whether the slowdown is a temporary funk or a lasting shift.

The forces arrayed against banks’ trading businesses are powerful. Since the financial crisis, regulators have limited their ability to take risks with their own money, and have made the process costlier, prompting many to dial back or push in different directions. At the same time, global markets have fallen into an unusually placid pattern that has damped clients’ desire to make trades.

“It’s been absolutely dead,” said Jarrod Dean, a municipal-bond trader at Sierra Pacific Securities in Las Vegas. Municipal-bond trading volumes are down about 30% since last August, he said, while profits are down more than 70%. “We’ve just got to keep toughing it out,” he said.

The malaise has prompted an Exodus of traders from big firms to smaller ones that are less subject to government oversight.

Late last year, Sound Point Capital Management LP, a $5.2 billion, credit-focused asset manager based in New York, scooped up five credit traders and analysts from UBS.

The rowdy atmosphere once celebrated on Wall Street already was on the wane when the crisis hit, as electronic-trading platforms began ushering in a quieter era. But the downturn and the new rules that followed have emptied desks and left fewer people to make sales calls and trade securities.

Down the road from UBS in Stamford, the U.K.’s Royal Bank of Scotland Group PLC has faced similar struggles. In 2005, RBS accepted $100 million of tax breaks in exchange for spending $345 million on a gleaming new headquarters in Stamford, creating 1,150 new jobs and retaining 700 employees in the state.

Two months ago, the bank, now majority-owned by the British government after a crisis-era bailout, said it planned to cut 400 jobs, in part to refocus the bank’s attention on the U.K. market.

A spokeswoman for RBS confirmed the intention to reduce staff and said it met the requirements under its agreement with the state of Connecticut, but otherwise declined to comment.

Among those no longer at RBS is Alan Osborne, who formerly sold fixed-income products for the firm ….”

Comments »Wall Street Begins to Worry About the….

CONSUMER

“Wall Street’s latest worry: The current state of the American consumer.

Despite a blockbuster June employment report, buffeted by positive auto sales and same-store retail sales numbers, many investors and strategists worry that American consumers just don’t have the cash, or the willingness to spend it, that is required for the recovery to continue.

These concerns have recently come to the fore, as companies from Wal-Mart to Rent-A-Center have warned that slack consumer demand will weigh on results.

In a filing released on Thursday, Rent-A-Center CEO Robert Davis said that “Macro-economic pressures continue to burden our financially constrained consumers contributing to softer than expected demand in our U.S. business segments. Consequently, revenue and earnings for the second quarter 2014 will not meet expectations.” (In response, the stock dropped by more than 10 percent on Friday.)

Some on Wall Street are ringing the alarm bell as well.

Nicholas Colas, chief market strategist at ConvergEx Group, warned on Friday that there’s a chance stocks will get rattled by “a shallow U.S. recession starting early next year,” caused by “slack consumer spending and a slower labor market,” due in part to the Federal Reserve reducing its stimulative measures.

“From a jobs perspective, things are slowly healing. But I do think that the desire to spend is still somewhat sketchy,” he told CNBC.com. “We’re still at low levels of confidence compared to other recoveries.”

Betting on the consumer has not been a great call this year. The S&P 500‘s consumer discretionary sector is up less than 1 percent in 2014, compared with a 6 percent rise for the index as a whole, making it the single worst-performing sector. (Of course, this comes after several years of outperformance.)

Craig Warga | Bloomberg | Getty Images

A Pier 1 Imports store in New York.

Some light on the consumer should be shed this week….”

Documentary: Education for a Sustainable Future

Cheers on your weekend!

[youtube://http://www.youtube.com/watch?v=_Eh6n-Kj5lw 450 300]

[youtube://http://www.youtube.com/watch?v=2OlAx4Dok38 450 300] Comments »

Comedy Files: An Honest Message from Phillip Maouf-Wifarts

Chart Chompers Special: Manipulation vs Productivity

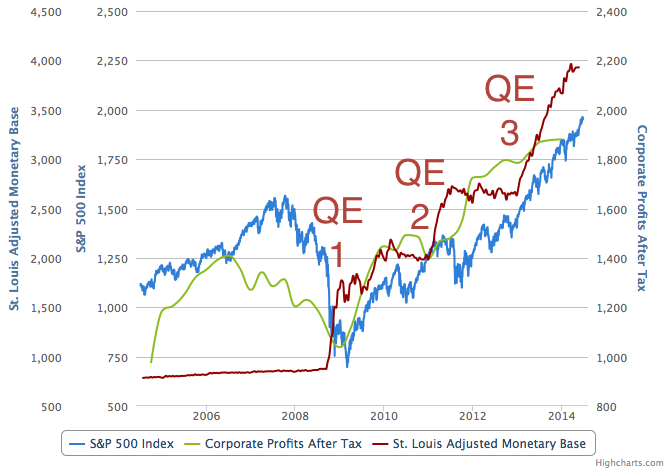

“Gary Tanashian writes: The following is an excerpt from NFTRH 298′s 38 pages of hard hitting, no b/s market analysis, which also included extensive work on the precious metals along with commodities, currencies, global markets andmarket sentiment.

Stock Markets – US

Happy Independence Day America! Your markets are bullish… and over bought, over loved and running on increasing momentum.

Courtesy of SlopeCharts

The graph tells a story of the end of the Greenspan era’s commercial credit inflation, which was resolved in 2008, and the beginning of the Bernanke era and official credit inflation, which is ongoing.

1) The bubble in mortgage and high risk commercial products (notice how official monetary base was in essence flat) began to fade in 2006 as corporate profits began to roll over, soon followed by the S&P 500.

2) The 2008 liquidation of the Greenspan era excesses brought with it all manner of official bailout operations, including QE’s 1, 2 & 3. Notice how each QE was instituted after a flattening of money supply.

3) But ultimately it is corporate profits that conventional market analysts are paid to respect (paying no attention to that man behind the policy curtain) and they have generally been strong.

4) As we noted last week, profits are rolling just a bit. Meanwhile money supply and the stock market continue upward. But there is a thing called ‘QE tapering’ in play and that could eventually flatten out the money supply as happened in 2010 and 2011/12.

5) They are tapering in an effort to gently manage an exit from the latest round of market and economic manipulation AKA official inflationary operations.

It will end badly because it was created through manipulation, not productivity. The current operation makes Greenspan look like child’s play. He had plausible deniability because it was the evil entities on Wall Street that took his policy ball and ran with it, slicing and dicing up all sorts of investment vehicles to sell to an unsuspecting public.

This time, there is no middle man. The Fed is more honest about its inflation as it expands its own balance sheet for all to see. And yes, the balance sheet is still expanding albeit at a tapered pace. Add in Zero Interest Rate Policy (ZIRP-Infinity?) and the Bernanke Fed has been celebrated as heroic because the majority perceive that they successfully did what they had to do to save the financial system.

But what the sycophants always seem to forget is that they had to do it because a different flavor of the same inflationary Fed policy fomented bubbles and brought on the big bust to begin with.

We remain in the age of Inflation onDemand and of boom/bust, which is much different from the pap that the happy idiots pumping today’s bullish environment would like to believe. Right now we are on a boom and that should not be denied. But understanding the framework within which the boom exists is important in managing risk.

What look like stellar technicals right now could continue to an upward blow off because that is how booms usually end. But if we are correct on the boom/bust nature of policy driven markets, the bust is gonna be a doozy. So please keep that on radar as well.

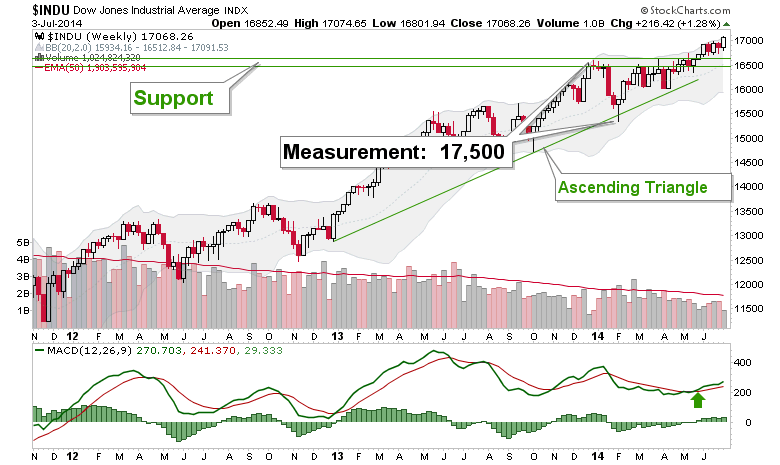

These are not conventional markets.

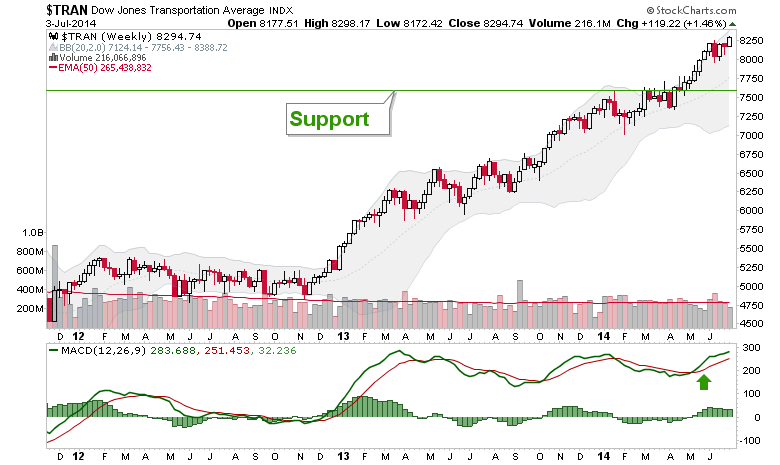

With that said, the Dow continues to target 17,500.

Tranny is in confirmation.

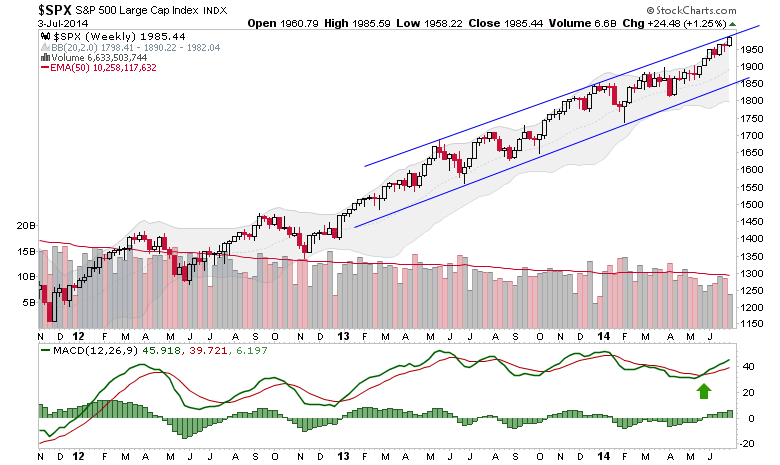

S&P 500 is at the top of the channel and in a strong bull trend. The channel top marks it as a candidate for a normal corrective decline. Alternatively, a break upward out of the channel – a channel buster – would be a sign of a possible building bull climax.

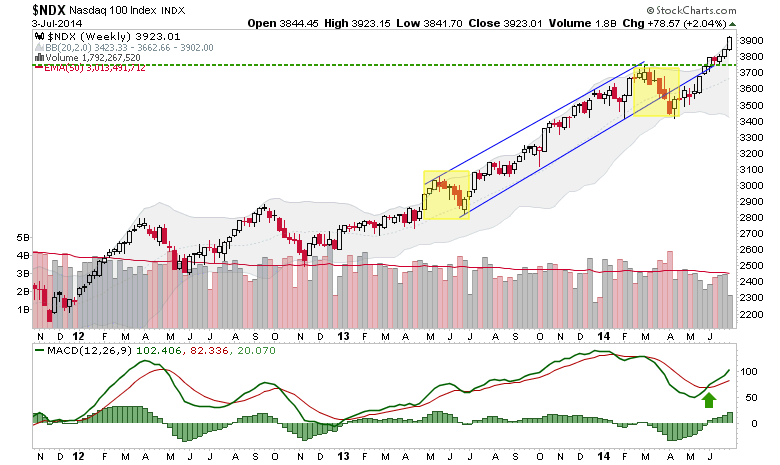

Nasdaq 100 is very strong on post-corrective momentum.

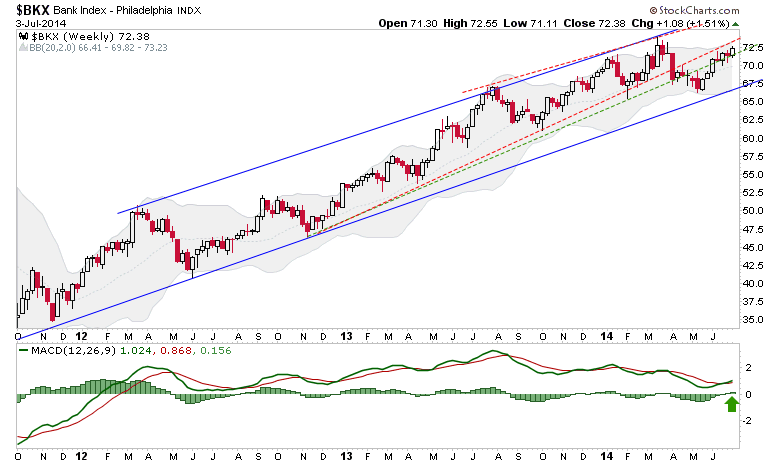

The banks are relatively under performing but are bullish.

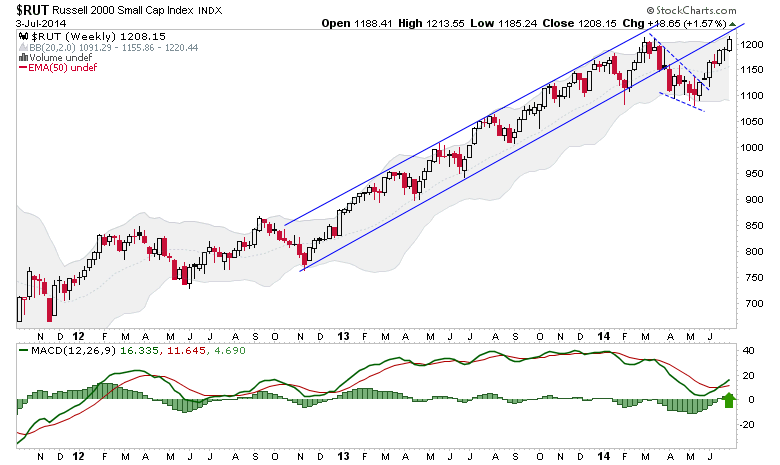

The Small Caps could either lead a market breakdown from the former channel bottom or gain some serious upside momentum. Watch the Small Caps as they are a momentum key and also because the Russell 2000 has a big picture measurement of 1378.

Is the current low relative momentum a negative divergence indicating an oncoming stock market correction (perhaps prior to new highs later in the year?) or is this index refueling to lead a big market mania blow off in a nearer term? Again, watch the Russell.

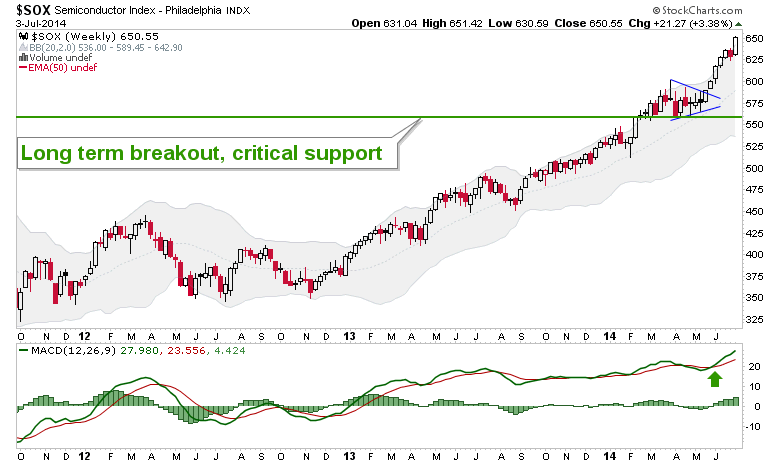

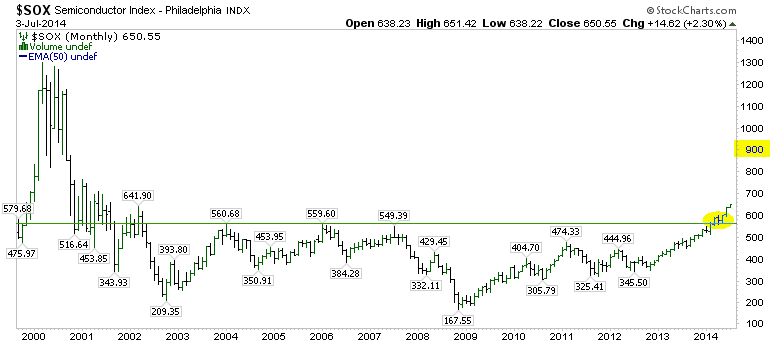

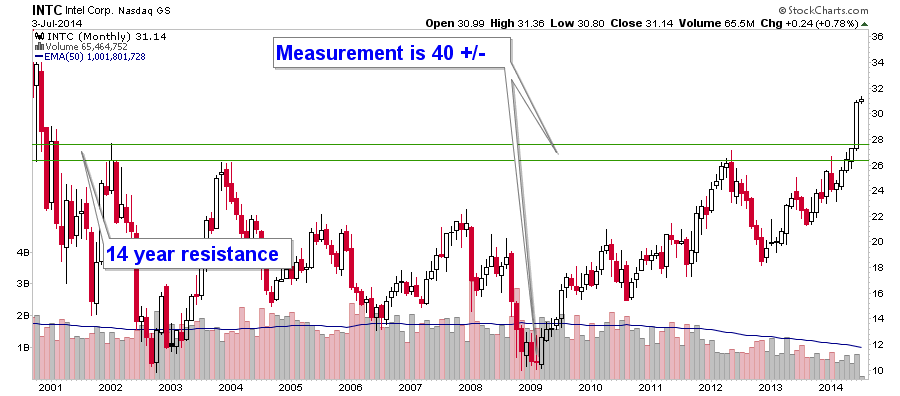

The SOX has long since proven its case as a momentum leader. Yet the reason I do not write the SOX off as a bubble index is because I do not write its biggest component (Intel) off as a bubble stock.

Monthly SOX has a target of 900.

Monthly INTC has a target over 40. The NFTRH+ chart above was created before the break through resistance, now support. I mention this so you will know that I am not simply charting or trend following. I liked Intel for its technical and fundamental potentials. Now a technical potential (long-term resistance break) has become a reality.

The information I had on Intel was to expect big improvements in their mobile chip initiatives, which have been sorely lagging for this chip giant. Instead what happened was that corporate PC demand increased (driving Intel through our projected breakout point) and the mobile chip market is still out there to be better penetrated, at least if Intel has any kind of fundamental execution coming.

Functionally what this does for me however, is to tell me to be careful about getting bearish on the SOX if I am bullish on Intel, the highest weighted component (of the iShares SOXX fund).

By extension it continues to moderate a bearish long-term stance on the stock market just yet, since the SOX has been our leading indication since January of 2013.

So the discussion on page 15 and 16 is in the realm of the theoretical, where I do not believe that a bullish backdrop is sustainable. But everything since page 16 has been bullish and you do not fight the market for what you may think you know is right with money you don’t want to lose, because you probably will lose it.

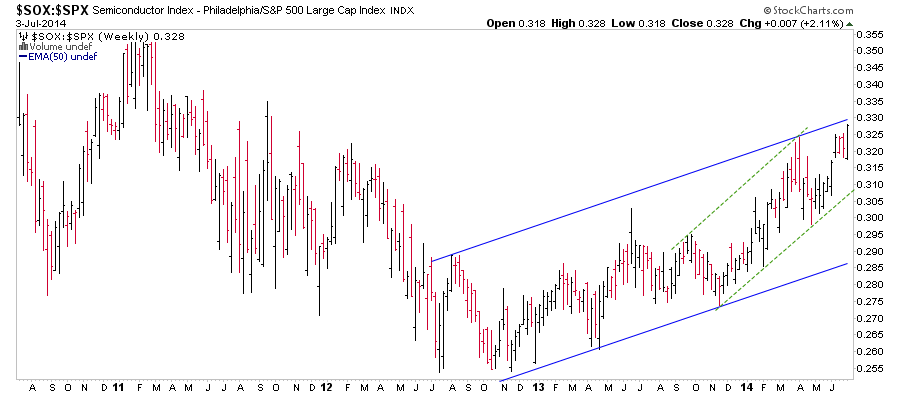

SOX leadership vs. SPX remains intact…

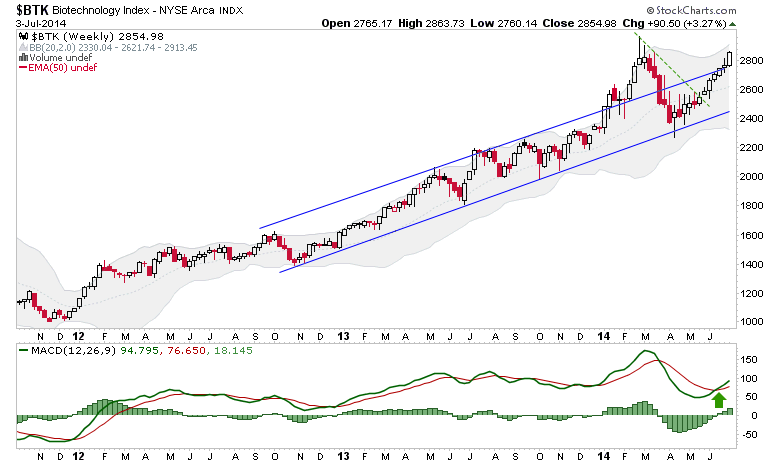

Talk about rebuilding momentum, check out the Biotechs…

Indicators

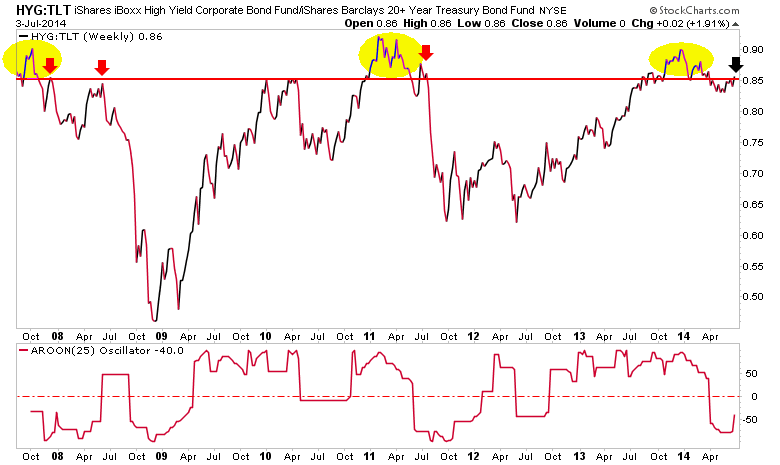

HYG-TLT (a junk vs. ‘quality’ credit spread) turned up last week and is threatening the breakdown line. This could simply be a breakdown retest (like the 3 red arrows) to suck in a few more bulls prior to a market correction. It could also be a gateway to an upside market blow off.

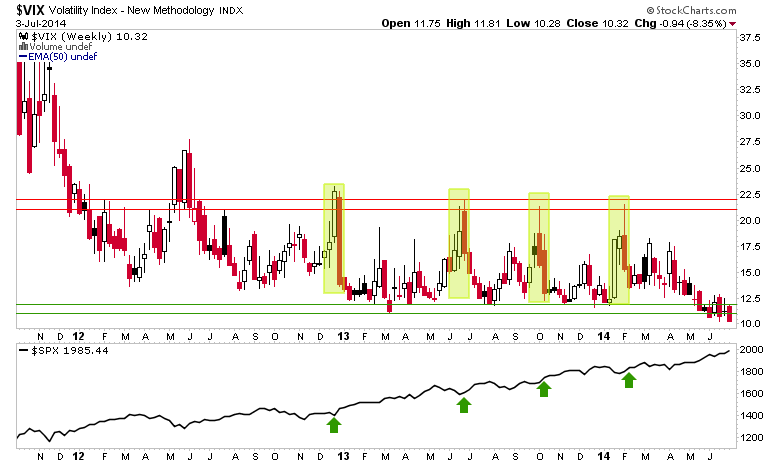

VIX is comatose as market players seem to perceive no volatility problems ….”

Comments »