According to a recent report published by Forrester 30% of all online shoppers now begin their search at Amazon rather than Google.

According to this article 86% of Americans who have bought something online said they’ve purchased from Amazon before and pressures on competitors as Amazon now controls more than 19 percent of all U.S. e commerce revenue, compared to 9 percent in 2001.

Google attracted only 13 percent of potential buyers as the first stop shop for product research. This is noteworthy change from 2009, when Google led Amazon among consumers 24 percent to 18 percent.

The downside for Amazon comes at the expense of retailers selling through the amazon marketplace:

There have been reports of sellers going into extreme pricing wars to win buy boxes (competing against other sellers and Amazon themselves). On top of that, there have been multiple retailer reports of Amazon reaching out direct to manufacturers that sellers on Amazon use (since retailers give up rights to all sales data that takes place on Amazon, Amazon can easily look at the big picture of their sales data and pick and choose where to expand their own fulfill by Amazon product line). Amazon may soon feel the pain as more retailers leave to list their product elsewhere.

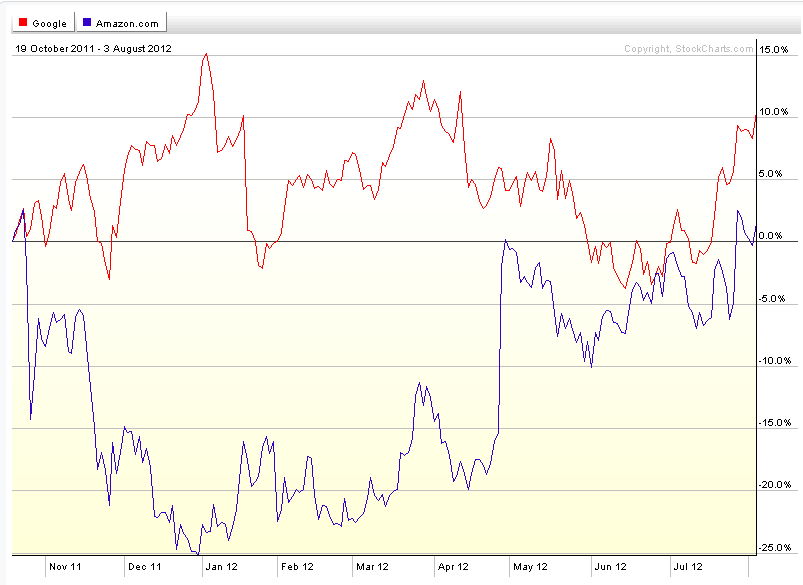

A quick look at the Stock performance of GOOG vs. AMZN over the past 9 months shows GOOG the clear winner. Obviously this is based solely on ad and click through revenues as some things will never be sold via AMZN. What is interesting is that AMZN has set it’s sites on Groupon (GRPN) and similar competitors with their Amazon Local program.