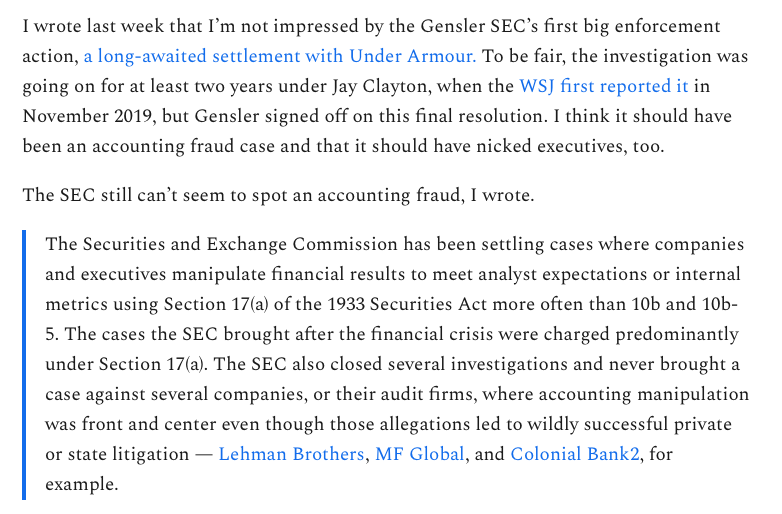

Gary Gensler “taught” a brief course at MIT in 2018 where one can see his true colors on the topic of crips. He’s so casual and fun. Cheering on aspiring mercenaries, regaling with one Lawrence Lessig. Ha ha ha! Let me tell you something, quietly, this man is a H8TR — a wonk that wants to make his name by REGULATION VIA ENFORCEMENT.

In a preprint posted online Thursday night, researchers at Google in collaboration with physicists at Stanford, Princeton and other universities say that they have used Google’s quantum computer to demonstrate a genuine “time crystal.” In addition, a separate research group claimed earlier this month to have created a time crystal in a diamond.

A novel phase of matter that physicists have strived to realize for many years, a time crystal is an object whose parts move in a regular, repeating cycle, sustaining this constant change without burning any energy.

“The consequence is amazing: You evade the second law of thermodynamics,” said Roderich Moessner, director of the Max Planck Institute for the Physics of Complex Systems in Dresden, Germany, and a co-author on the Google paper. That’s the law that says disorder always increases.

Time crystals are also the first objects to spontaneously break “time-translation symmetry,” the usual rule that a stable object will remain the same throughout time. A time crystal is both stable and ever-changing, with special moments that come at periodic intervals in time.

“REGULATING SWAPS = DEMOCRATIZING FINANCE” – PER GENSLER

“WILD WEST” – PER GENSLER

Currently, we just don’t have enough investor protection in crypto finance, issuance, trading, or lending. Frankly, at this time, it’s more like the Wild West or the old world of “buyer beware” that existed before the securities laws were enacted. This asset class is rife with fraud, scams, and abuse in certain applications.

“COME TALK TO ME” – PER GENSLER

Further, I’ve suggested that platforms and projects come in and talk to us. Many platforms have dozens or hundreds of tokens on them. While each token’s legal status depends on its own facts and circumstances, the probability is quite remote that, with 50, 100, or 1,000 tokens, any given platform has zero securities. Make no mistake: To the extent that there are securities on these trading platforms, under our laws they have to register with the Commission unless they qualify for an exemption.

“STABLE VALUE COINS” – GENSLER POTENTIALLY REBRANDS STABLECOINS

“TECHNOLOGIES DON’T LAST LONG IF THEY STAY OUTSIDE OF THE REGULATORY FRAMEWORK” – PER GENSLER

I am technology-neutral. I think that this technology has been and can continue to be a catalyst for change, but technologies don’t last long if they stay outside of the regulatory framework.

Gary Gensler, U.S. Securities and Exchange Commission Chair, is one of the world’s most powerful financial regulators and a key player in the push by the government to regulate the trillion-dollar plus cryptocurrency industry. On Tuesday, Sept. 21 at 12:00pm ET, Washington Post columnist David Ignatius speaks with Gensler about the cryptocurrency landscape, the growth in digital trading platforms and his call for more stringent financial disclosures around sustainability.

There’s also a less obvious group: women who believe in Bumble’s message and identify as feminists but who still prefer to have men make the first move. Wolfe Herd is aware of this—and frustrated by it. “They love the brand, they want to wear the T-shirt, but they [also] want archaic love,” she says. “They want a 6-foot-tall guy to make them feel small and make the first move. So it’s a paradox.”

fun fact:

The Bumble app, launched in 2014, is one of the first dating apps built with women at the center. On Bumble, women make the first move, and have done so more than 1.7 billion times from September 2014 to September 2020. Bumble is the second highest grossing dating app in the world according to Sensor Tower, with 12.3 million monthly active users (“MAUs”) as of September 30, 2020.

In preparing for this missive, Jungle has steeped herself in an ocean of bliss (non-synthetic). Hence, the usual vitriolic tone might be distant and this drivel may end up being a bore. Apologies in advance. Anger, greed, and lust you see are the three enemies of the mind. But you troglodytes wouldn’t know anything about that, save @diddy who practices vipassana on the regular. Diddy might have in fact reached a state of liberation, having ceased participation in the hallowed halls of late. Opting in its stead for a life of quietude, contemplation and focused attention. Hat tip, dear sir. Eventually, Jungle will follow. Or she will cross 47.5 – at which age subs are requested to graciously retire. At that time, you fuckers will be bored, longing for the days Jungle roamed. For now, her unbridled ego keeps her loquacious — enjoy it while it lasts.

Now, let us move on to the Orwellian matter at hand, Palantir. We will invoke this topic with an advertisement from our known and loved Apple Computer, circa 1984. A very important year for a plethora of reasons, which we will cover during this session.

PALANTIR. INCOMPETENT BIG BROTHER.

Named after the “Seeing Stones” in The Lord of the Rings, Palantir is designed to ingest the mountains of data collected by soldiers and spies and police — fingerprints, signals intelligence, bank records, tips from confidential informants — and enable users to spot hidden relationships, uncover criminal and terrorist networks, and even anticipate future attacks.

When Palantir descended upon Palo Alto many moons ago, it was shrouded in mystery. Like locusts, employees of the growing concern roamed around town in customary ‘patagonia-vest-uniform’ emblazoned with cryptic insignia. No one really knew “what they did” while skeptical regulars at Rose & Crown whispered, “it’s a cult”.

Let us examine perspectives from around the ol’ web, regarding said concern’s chicanery, shall we?

Palantir works to reanimate its clients. Its merchandise are not enterprise apps, rather modus operandi and culture. In many ways it is unique — a new type of company. It is an ideological company, a psychologist, a rabbi or a priest to the rulers of the world. Palantir’s software is the flesh that embodies that ideology.

“They” continue:

We live in the Shire and we call ourselves hobbits. Wearing identical t-shirts provided to us by the company we surrender our individuality to embrace the collective. A lot of us date and get married to our peers in the commune. To many Palantir is a tribe, family and home after years of adversity and insecurity experienced growing up middle-class but finding it hard to fit into the fabric of society. We gladly accept lower salary in exchange for the sense of purpose and common mission. At the local canteen daily we enjoy organic food while sharing stories of our victories against our common enemy: chaotic, uncertain, anxious and unimaginative present. We helped find Osama bin Laden!

Incidentally, in the early naughts, one of Jungle’s acquaintances who was a recent computer science graduate from The Farm, took up employment with said concern. In short order, this mild-mannered chap abandoned steady pay, stating that he fundamentally disagreed with practices of said cult — thus, inspired by degeneracy of the highest order, he was off to law school. Chuckle. Quietly, Jungle made a note to self.

Days turned into months, turned into years, turned into decades, and here we are at the tail end of 3Q2020 with Palantir making its grande debut on our (supposedly) liquid public markets. That said, Jungle rings the virtual opening bell, a sacred invocation — and welcomes Palantir to the circus. A “darling” of the US Intelligence community, and a concern that has enraptured the minds of pikers and Mungerian-Tea-Baggers alike.

And what wares does this diseased rort exactly sell? — essentially a system to organize unstructured data (often classified) and access to a trove of databases generally inaccessible to public eyes. Supposedly searches by race, gender, gang membership, tattoos, scars, friends, or family — all game! Some have called it a “pro-military” arm of SV. Hackers call it “a massive excel plugin” are candidly, unimpressed.

… Palantir applies Silicon Valley’s playbook to domestic law enforcement. New users are welcomed with discounted hardware and federal grants, sharing their own data in return for access to others’. When enough jurisdictions join Palantir’s interconnected web of police departments, government agencies, and databases, the resulting data trove resembles a pay-to-access social network—a Facebook of crime that’s both invisible and largely unaccountable to the citizens whose behavior it tracks.

Per the S-1’s opening manifesto, Alex Karp (founder) declares:

Our software is used to target terrorists and to keep soldiers safe. If we are going to ask someone to put themselves in harm’s way, we believe that we have a duty to give them what they need to do their job. We have chosen sides, and we know that our partners value our commitment. We stand by them when it is convenient, and when it is not.The ability of our most vital institutions to protect and provide for the public requires the right technology. And we believe that as a result, over the long term, the strength and survival of democratic forms of government do as well.

A fear-mongering dandy, full-of-shit individual, with a Ph.D. in neoclassical social theory, to boot. So sweet of him, no?

With Karp, as with Palantir, it’s often hard to know what is real and what is mythmaking. It’s often repeated in articles, for example, that Karp studied in Germany under Jürgen Habermas, perhaps the most influential living philosopher. “The most important thing I learned from him is I couldn’t be him, and I didn’t want to be him,” Karp confided on a recent podcast with a sort of knowing intimacy. In fact, as Moira Weigel, a historian of media technologies, has pointed out, Karp not only didn’t do his dissertation under Habermas, he didn’t even study in the same department

Eccentricities continued:

When he grows excited about an idea, say current and former employees, he balls his fists and taps employees rapid-fire in the solar plexus.

Mkayyyyyyyy.

Getting back to business:

Palantir’s software can ingest and sift through millions of digital records across multiple jurisdictions, spotting links and sharing data to make or break cases.

The scale of Palantir’s implementation, the type, quantity and persistence of the data it processes, and the unprecedented access that many thousands of people have to that data all raise significant concerns about privacy, equity, racial justice, and civil rights. But until now, we haven’t known very much about how the system works, who is using it, and what their problems are. And neither Palantir nor many of the police departments that use it are willing to talk about it.

At the big picture level, Palantir reminded me of MicroStrategy: big claims and hype, DC-centricity, elite school hiring focus, youth focus, a large field technical team, and a work hard / party hard ethos.

For you n00bs who are kicked about Microstategy’s latest hail mary — as of September 15, 2020 the company has purchased a total of 38,250 bitcoins at an aggregate purchase price of $425 million — just remember said concern was once dubbed “MicroTragedy” on The Walled Street.

Kellog continues:

At this point I should admit to having some scars from having run marketing at Business Objects during MicroStrategy’s rise. Let demonstrate what a day in life looked like:

Dave, MicroStrategy says their mission is to “purge ignorance from the planet.” How come we can’t say anything visionary like that in our mission?

Dave, Michael Saylor says he’s going to build a modern-day Versailles just outside of DC. How come our CEO never says stuff like that?

Dave, MicroStrategy says they’re building a service where people will wear tiny microphones in their ears and it will notify them if their house catches fire. How come we don’t have product vision like that?

Dave, MicroStrategy just did a $52.5M deal in an industry where average sales prices are $250K and a big deal is a few million. Why can’t we do huge deals like that?

Dave, Michael Saylor says that there will be riots if his software doesn’t work and that this year people will die — literally — because they didn’t buy his software. How come we’re not mission-critical like that?

To which for several years I had to say “it’s all bullshit, it’s all bullshit, it’s a barter transaction and they’re double counting, and it’s all bullshit.”

Nothing changes on the Walled Street dear penii. Palantir is simply an avatar of many a rort that came before it. Same playbook, different decade. 16 years in business and still losing money.

Mr. Karp characterizes those struggles as part of a creative process now yielding results. “This is not a science,” he says. “We are a colony of artists. You cannot go to Basquiat or Monet and say, ‘Well, that painting didn’t capture the time.’ ”

As a sidenote for you illiterates, an “avatar” is not that stupid pic that you spend half your day changing daily — and for fucks sake, its not “avitar” — do you even know what the word means? No, you don’t. Give your self lesson in etymology, because we have lots to cover and Jungle can not do everything around here.

Back to business.

Palantir, Palantir

On the Wall

Who is the Top Dog

Of them All?

“Here is the problem with no IPO,” said Robert Ackerman, a venture-capital investor with $30 million in Palantir shares. “Palantir has a lot of investment funds with limited lives.”

Venture-capital funds typically have a 10-year lifespan before their limited partners must be repaid. Some investment funds already have sold Palantir shares, partly because demand in the secondary market is high.

GSV Capital Corp. sold $7.8 million in Palantir stock in the second half of 2014, said Michael Moe, the Woodside, Calif., firm’s chairman, chief executive and chief investment officer. At the end of this year’s third quarter, GSV still held Palantir shares valued at $54.6 million, securities filings show.

“Given the fact that there’s an active private market, we’ll continue to look for opportunities to sell when appropriate,” said Mr. Moe.

For all you homegamers who were excited about SSSS‘s stake — the fund was formerly GSV Capital (ticker: GSVC), rebranded and renamed : NeXt Innovation Corp — odd, no?

Mutual funds have written down their investments in the company. Bailie Gifford, the Scottish fund manager, disclosed that its stake in Palantir had made annual returns of -3.5 per cent from 2014 through March this year, according to its annual report.

Net net, we know Orwell and Huxley called it — some souls have made hay, and some have not. Palantir is squarely in the latter category and we need not waste any more time on said concern. Been going at it for 16 years, lost 580 mil in 2018, and 580 mil in 2019. For 1H20, loss of 164,729. Average client yields $5mi — this after almost two decades of aggresive marketing. Trash heap extraoridnaire, ’nuff said.

Now, let us move on from the Orwellian concern, to Orwell and his contemporaries. A beautiful worlds awaits.

Orwell and Huxley. Huxley and Orwell. Incidentally, these gents have been mentioned in the hallowed halls as of late. Le Wasp (nee Le Fly) has been mentioning Brave New World, a show based on Huxley’s classic novel. Furthermore, as if a sign from above to get this fcking post out, Jungle was recently walking around the hood, and noticed a small memento on the neighbor’s fence:

Odd! No!?

George Orwell, born Eric Arthur Blair in Motihari — modern day Bihar, India, 1903. Supposedly, tutored in French by Huxley; famous for the dystopian novel 1984, in which the term BIG BROTHER was coined. His contemporary, Aldous Huxley, born in Surrey, England, 1894. Some call him the Godfather of Psychedelics. Both gents Etonians, of the same “caste”, if you will.

While we mainly know Huxley for Brave New World, he was quite prolific. From 1937 until his death (the same day as JFK) he resided in the United States, mainly in Southern California. What we hear less about is Huxley’s book, Island. @peterbebergal does a fine job of reviewing Huxley’s time in SoCal, so Jungle will not bother reinventing the wheel — but below, do note whilst using the language “material and spiritual crisis” which is eventually approached with a “faster and less strenuous” methodology — Huxley was not trying to sell anything (maybe a book). These days peddlers have coined “spiritual capitalism” as the sales pitch for the next drug company. Silicon Valley is having a crisis of conscience. Cloying to say the least.

per @peterbebergal:

Between his 1932 vision of a sterile dystopia in Brave New World and the 1962 novel Island about a spiritual utopia, the author Aldous Huxley experienced two things; the Hindu religious philosophy known as Vedanta and psychedelic drugs. In Brave New World, people are addicted to Soma, a hallucinogenic that artificially simulates a kind of dull transcendent state, and so makes religion irrelevant. In Island, the Palanese (residents of Pala where the book takes place) ritually use the drug moksha for spiritual and mystical insights. It wasn’t that by the time he was writing Island Huxley no longer believed that civilization was potentially doomed to a homogenized over-indulgent consumer culture, but rather that there was another possibility for human destiny. Soon after writing Brave New World Huxley saw this other opportunity but believed it would take work, a disciplined and rigorous adherence to a spiritual ideal. By the time he got around to writing Island he was convinced there was a faster, less strenuous way to find the higher purpose of human consciousness: mescaline.

HUXLEY IN SOUTHERN CALIFORNIA

In 1937 Huxley moved to California and within a few years was introduced to the Vedanta Society of Southern California by his friend, the writer and scholar Gerald Heard. Huxley had been developing his perennial philosophy, the idea that religious traditions are historically and culturally relative but that they each validate, in their own way, that human beings are divine and that the purpose of our lives is to come into a relationship with the numinous behind the phenomenal world. Huxley believed the realization of our latent divinity to be a possible remedy to what he perceived as a Western material and spiritual crisis. Vedanta was the method Huxley had been looking for.

Vedanta is the philosophical underpinning of Hinduism, itself a dreamscape of multiple deities and stories of epic battles. Vedanta distills all of the multi-armed, elephant-headed, sword-wielding gods into one simple idea. The most important of the Vedic literature, The Upanishads, teaches that brahman, the supreme reality of all things, and atman, the manifestation of the divine in the human soul, are one and the same, a pure and perfect whole. Our purpose during our gross bodily manifestation is to recognize the divinity within all things. When we come to this, Vendata tells us, we will also see that every religion is merely a different way of expressing the same principle, the same overarching truth that there is no separation between the soul and God.

Huxley wrote for the Society’s journal and took up the cause of teaching one of Vedanta’s essential ideas; do not mistake the quick and often dramatic effects of meditation for actual spiritual truths. In one journal article, “The Magical and the Spiritual,” Huxley wrote, “At present there is a lamentable tendency to confound the psychic with the spiritual, to regard every supernormal phenomenon, every unusual mental state as coming from God.”

Swami P and Huxley disagreed on the topic of “fastrackery” — with Swami P vehemently opposed to the use of psychedelics.

Nothin’ wrong with “installing a little software”, says Jungle — with all due respect to the monk.

The most famous account of mescaline remains Aldous Huxley’s The Doors of Perception, the first book to evangelise about the possibilities of psychedelics to mainstream audiences, especially in the US. Huxley took mescaline in May 1953, at his home in the Hollywood Hills; he was approaching his fiftieth birthday and at a low point in his life. It seemed to lift him out of a depression and he wrote The Doors of Perception with an epiphanic zeal that today reads as both naive and not (our culture holds two ideas of psychedelics at once, that they can be both serious and life-changing, or something you do on a Friday night to get goofy with your friends). Huxley’s famous description of the folds of his grey flannel trousers was an embellishment, Jay informs us (he was actually wearing jeans), and his hope that mescaline would be a cure for schizophrenia turned out to be misplaced. But Huxley did help to normalise the psychedelic experience. He was, Jay writes, ‘an adept of spiritual self-discovery, but also a stand-in for a sober general public to whom, until the arrival of mescaline, all mind-altering drugs had been “dope”, of interest only to bohemians, foreigners and criminals’ – the Michael Pollan of his time.

Which brings us to dear ol’ Michael Pollan (aka DAD, aka THE MIDWIFE, aka THE CHOSEN ONE). Pollan unlike Huxley doesn’t want you getting there too fast either:

I look forward to the day when psychedelic medicines like psilocybin, having proven their safety and efficacy in F.D.A.-approved trials, will take their legal place in society, not only in mental health care but in the lives of people dealing with garden-variety unhappiness or interested in spiritual exploration and personal growth.

My worry is that ballot initiatives may not be the smartest way to get there. We still have a lot to learn about the immense power and potential risk of these molecules, not to mention the consequences of unrestricted use. It would be a shame if the public is pushed to make premature decisions about psychedelics before the researchers have completed their work. There is, too, the risk of inciting the sort of political backlash that, in the late 1960s, set back research into psychedelics for decades. Think of what we might know now, and the suffering that might have been alleviated, had that research been allowed to continue.

When psychedelics like psilocybin and LSD burst upon the scene in the 1950s and 1960s, they arrived without an instruction manual. Half a century later we’re still struggling to learn how best to harness their spooky power. One source of wisdom on that question is other cultures with much longer experience using these medicines. (Just this week, archaeologists reported finding a 1,000-year-old set of tools in Bolivia bearing trace amounts of ayahuasca and other psychoactive chemicals.)

Thanks DAD!!!

For whatever reason Michael Pollan has been ordained THE MIDWIFE. The midwife that births America’s Upper Middle Class Consciouness into accepting weed, plant-based diets, and now psychedelic medicine as reasonable “lifestyle” choices, with “transformational potential”. He roams around and blabs on podcasts, on campus, and widely accepted purveyor of culture, The New York Times — wherever the “right” demographic will tune in. Recall, it was almost 20 years ago that he cited GW Pharma (ticker: GWPH) at a talk titled Cannabis, Forgetting, and the The Botany of Desire at the University of California. Now he’s a “thought leader” on psychedelics. Jungle believes this go round of widespread acceptance/adoption will be expedited, not only due to the proliferation of information, but by groundwork done by the gateway drug, marijuana. Old world institutions still roaming aroung with their nose up in the air, while tech bros are coming to the rescue.

So we have tried the traditional sources of funding and that has not worked.

There are over a million veterans that are receiving disability payments from the Veterans Administration for PTSD and it costs the Veterans Administration somewhere in the neighborhood of 15 to $20 billion a year on these disability payments. They pay multiple billions of dollars every year on SSRIs and other things to treat people with PTSD and yet we’ve not been able to get a penny from the VA.

So we’ve tried the VA, The Department of Defense, The National Institute of Mental Health, a lot of the major foundations. The Wellcome Trust is the largest foundation in England, started by Burroughs Wellcome stock, by pharmaceutical stock. They’re focused on neuroscience and psychology and they said, “Go away. It’s a reputational risk for us.” I said, “It’s a reputational opportunity.” But that didn’t work.

THIEL, SUGARDADDY OF TECH BROS INVESTS IN COMPASS

Backed by Theil, Compass is a UK based operation that went public recently. Co-founders Ekaterina Malievskaia and George Goldsmith “involuntarily” founded the company as their son became “unrecognizable” — the mother had sleepless nights and stayed up at night reading literature and discovered papers on psilocybin — a drug that was synthesized in 1958 by Sandoz Pharmaceuticals by a gent named Albert Hofmann. Sidenote: Sandoz produced 2 mg pink psilocybin pills under the trade name Indocybin that was marketed for psychotherapeutic uses in the 1960s. Sandoz is now a division of Novartis. Point is, this is not an entirely new endeavor but was severely hampered by The Controlled Substances Act of 1970.

The company has a great backstory, with roots in the serendipitous invention of lysergic acid diethylamide by the Swiss chemist Albert Hofmann at Sandoz in 1938 through to Timothy Leary’s Harvard Psilocybin Project in the early 1960s. Leary, whom Richard Nixon deemed the “most dangerous man in America”, upended proper studies of the potential benefits of psychedelics after he was thrown out of Harvard for his unorthodox – some might say hedonistic – approach to research. The classification of LSD and its trippy cousins as Schedule 1 substances in 1970 relegated them to recreational use.

per Goldsmith, co-founder CMPS:

“Our goal is to develop psilocybin therapy—the preparation, the support for the actual dosing, the medicine, and the follow-up,” said Goldsmith, a lanky, bespectacled sixtysomething former executive coach. “And then other clinics and so forth will buy and deliver that.”

the product, the service:

Compass has developed a crystalline formulation of psilocybin called COMP360, which could lead to “rapid reductions in depression symptoms and effects lasting up to six months, after administration of a single high dose,” it says. COMP360 forms part of an overall treatment, including a six-to-eight-hour session under its influence, with support from specially trained therapists.

COMPASS PATHWAYS 424B4 FILING EXCERPT

The potential of psilocybin therapy in mental health conditions has been demonstrated in a number of academic-sponsored studies over the last decade. In these early studies, it was observed that psilocybin therapy provided rapid reductions in depression symptoms after a single high dose, with antidepressant effects lasting for up to at least six months for a number of patients. These studies assessed symptoms related to depression and anxiety through a number of widely used and validated scales. The data generated by these studies suggest that psilocybin is generally well-tolerated and has the potential to treat depression when administered with psychological support.

COMP360 is our proprietary psilocybin formulation that includes our pharmaceutical-grade polymorphic crystalline psilocybin, optimized for stability and purity. Our investigational COMP360 psilocybin therapy comprises administration of our COMP360 with psychological support from specially trained therapists with specific professional and educational qualifications. We believe this support, or therapy, is as important to the psilocybin therapy as the psilocybin itself. The psilocybin administration session lasts approximately six to eight hours, with patients supported by therapists in a non-directive manner. Psilocybin administration sessions are preceded by preparation sessions, in which patients are given a thorough orientation, and followed by integration sessions to help patients process the range of emotional and physical experiences facilitated by COMP360 administration.

In 2019, we completed a Phase I trial in 89 healthy volunteers, the largest controlled trial of psilocybin to date, with our investigational COMP360 psilocybin therapy. In this trial, we observed that COMP360 was generally well-tolerated and supported continued progression of Phase IIb studies. The trial also showed the feasibility of simultaneous administration of COMP360 to up to six people in the same facility, with 1:1 therapist support, which we believe will accelerate future clinical trials and commercial scale-up upon potential regulatory approval. In August 2020, the FDA approved our request for a 1:1 model of therapist support and we intend to use this model in future clinical trials. We previously conducted a series of in vitro and in vivo toxicology studies, including tests for genotoxicity and cardiotoxicity. We are now undertaking an additional series of safety pharmacology and toxicity studies, to be completed prior to commencement of our anticipated Phase III program.

We are currently conducting a randomized controlled Phase IIb clinical trial in 216 patients suffering with TRD, in 20 sites across North America and Europe. This dose-finding trial is investigating the safety and efficacy of COMP360 combined with psychological support, for the treatment of TRD, and aims to determine the optimal dose of COMP360, with three doses (1mg, 10mg, 25mg) being explored. The primary endpoint of this clinical trial is to evaluate the efficacy of COMP360, as assessed by the change in the Montgomery-Åsberg depression rating scale, or MADRS, a widely accepted scale for depression that has been used as a primary endpoint in pivotal trials of other depression treatments. This trial has been designed to capture a statistically significant reduction in MADRS. We plan to report data from this trial in late 2021. We are using digital technology in this trial, including an online portal to help patients prepare for their psilocybin experience, and a web-based “shared knowledge” interactive platform to complement therapist training. We are also collecting digital phenotyping information through the measurement of human-smartphone interactions. After the trial, these data will be compared with information collected from validated psychiatric scales, such as MADRS, to develop potential digital applications to help anticipate relapse of depression. In the future we plan to expand our research into additional digital technologies to complement and augment our therapies.

The need for innovation in mental health care is significant, given that the current paradigm is ineffective for millions of people. Our vision is a world of mental wellbeing – a world in which mental health isn’t simply the absence of mental illness, but the ability to flourish. We want to help reduce the stigma surrounding mental health, to acknowledge that “everyone has a story,” and to create a system of care for all who are not helped by the existing system and existing therapies.

Money making endeavors aside. Rick Doblin PhD is the founder of MAPS.org, a non-profit organization. He wrote his dissertation on the regulation of psychedelics and marijuana. MAPS was started in 1986. He and Pollan are making the rounds on panels along with boffins looking at brainwaves — the pioneer and the midwife, if you will. One can’t help but admire his relentless pursuit to prove that MDMA indeed has therapeutic value. For more on Doblin’s journey, give this a listen, or a read. Doblin cites an MDMA Assisted Psychotherapy trial in which n = 107 and after a 2 month followup 56% of particpants no longer qualified and after 12 months 68% non longer qualified. Net net : EFFECT SIZE HUGE. MDMA is important because it reduces the fear response (which psilocybin does not do) and thus in combination, could be the “killer app” — kapish?

As a sidenote, isn’t it amusing that “coiner” Michael Novogratz is on the bandwagon as well?

I think one of the things we need to do as a society is to allow that people have mental health issues, that depression is real, and that people have shit to work through, and that we should help them work through that. And both psilocybin and ayahuasca are, I just think, two things in that tool kit, powerful things in that tool kit of how one can process trauma, one can learn about themselves, one can dig into places that they haven’t understood before. And it’s funny, once you see it, you can’t unsee it.

Jungle unequivocally agrees, Install the Software! Updates are few and far between.

Sat May 30, 2020 7:26pm ESTComments Off on GET READY FOR A DEEP $DKNG

BACKGROUND ON THE ILLUSTRIOUS IPO

In December, Draft Kings announced plans to become a publicly traded entity via a reverse merger with Diamond Eagle Acquisition Corp. (NASDAQ:DEAC) and SBTech. DraftKings was founded in 2011 as a fantasy sports company. Its earlier investors include the Raine Group, and the owners of the New England Patriots. The deal valued the sports betting firm at $3.3 billion. Under the terms of that transaction, Diamond Eagle a special purpose acquisition company (SPAC) or blank check entity took the Draft Kings name, changed the ticker and reincorporated in Nevada from Los Angeles. The combined company projects to have $540 million in revenue next year, with $400 million of that coming from DraftKings and $140 million from SBTech, per founder Jason Robins. Revenues are expected to grow to $700 million in 2021, with $550 million coming from DraftKings.

Diamond Eagle is the fifth SPAC set up by serial dealmaker Jeff Sagansky, who founded Diamond Eagle with investor Harry Sloan. Sloan served as chairman and CEO of MGM between 2005 and 2009 prior to the completion of its restructuring via a pre-packaged bankruptcy. He was also the founder, chairman and CEO of SBS Broadcasting, Europe’s second-largest broadcaster. Sloan founded SBS Broadcasting in 1990 with a personal investment of $5 million. He built SBS into the second largest broadcaster in Europe, with 16 television stations, 21 premium pay channels and 11 radio networks, reaching 100 million people in nine countries. He led the company’s initial public offering in 1993 and sold SBS (Nasdaq: SBTV) for $2.6 billion in October 2005 to Permira and KKR. In 2007, SBS consolidated its operations into Prosieben Sat.1 Media AG, Germany’s largest television broadcasting group, creating a European media powerhouse.

Incidentally, the two have their sixth SPAC on deck, Flying Eagle Acquisiton Co. SPACs raise money from public investors to pursue acquisitions, allowing a private company to go public without an initial public offering.

DISNEY “INVESTMENT”

In 2015, Fox invested $160 million in DraftKings. DFS was hot hot hot. Of course, much like weed being hot hot hot and Constellation writing down Canopy, Fox took a write-down to the tune of 60% on DKNG. A miniscule deep dicking, for the behemoth. Disney later picked up Fox in a $71 billion deal, leaving them with the scraps of the Draft Kings investment. Hence Disney owns 6% — not quite a deliberate stake.

++++

DUOPOLY

For you ham and eggers who are not well versed in googling. The DFS (Daily Fantasy Sports) “industry” if you can call it that, is currently a duopoly, or a situation in which two suppliers dominate the market for a commodity or service. The other player is known as FanDuel.

FanDuel was founded in 2009 and sold to Paddy Power Betfair in 2019. For whatever reason, Paddy Power changed its name to Flutter Entertainemnt in 2019 also, to better reflect the diversity of its brands. Per Flutter Annual report, FanDuel share of US online sports betting market stood at 44%. Together with DraftKings, the duopoly makes up ~95% of US Online Sports Betting. Unclear if that metric refers to stakes or actual revenues.

The FanDuel sportbook has a retail presence in 6 states and is live online in 4 (four multichannel in New Jersey, Indiana,West Virginia and Pennsylvania, and two retail-only in NewYork and Iowa). In addition to the sports-books, FD offers daily fantasy sports across 40 states, horse racing wagering via TVG business and online casino in both New Jersey and Pennsylvania.

All in all, Total Flutter Group Revenues for 2019 = £2.1 billion. Of that, roughly £376 million in revenues were from “US Operations” which are comprised of: FanDuel + a dainty horse racing operation + online casinos in NJ/Penn + a few retail boxes.

To put sports betting into context of Total Flutter Group Revenues, 42% or £900m of reveneues were a results of Sports Betting and of that sum, approximatley 57% or £513mil from online/mobile channels.

The question is what the hell is the actual market size of online sports betting at the moment. The answer is UNCLEAR. Morgan Stanley, with no reason to be modest, puts the number at $7 BILLION US in 2025, saying it could “swell” to $15 BILLION if all 50 states sign off by then.

GamblingCompliance, a company that tracks the activity across the U.S. and Europe, is forecasting that sports betting will generate between $2 billion and $6 billion per year in 2022.

Goal posts are wide. Abjectly laughable.

In any case, forecasters gonna forecast. So we take it wit a grain of himalayan pink salt. Elitist salt, per members of the hallowed halls.

++++

A NOTE ON FANDUEL SALE TO PADDY POWER/FLUTTER GROUP

In considering Draft Kings, one might also look at FanDuel’s history. In July of 2018, Paddy Power (now Flutter Group) picked up FanDuel for what some might consider a paltry sum, given the $416million it had raised in 7 rounds of funding at valuations reaching $1 billion plus.

For the figures, The Paddy Power Group contribued its existing US assets (aka Betfair Assets) along with $158m of cash. This cash contribution was to be used to pay down existing FanDuel debt (net debt of $76m at 31 March 2018) and fund working capital of the combined business. Betfair US had gross assets of $612m at 31 December 2017. So, at max, the total consideration was $770million.

As a sidenote, In 2017, the last full year of results prior to merger, FanDuel reported $124 million in revenue and 1.3 million active customers.

In court, FanDuels founder moaned about the $465 million “valuation” which was allegedly depressed to favor preferred investors. Probably because he got a big fat bagel out of the deal. Apparently, the deal was not adjusted to reflect the repeal of PAPSA, which is really the tailwind/hype behind the industry at the moment. That and of course “the return of sports” – yawn.

Interestingly, in another lawsuit, filed by employees who also received nothing — we see some details of Moelis’s prognostications on FanDuels prospects.

The lawsuit also notes that after the failed DraftKings merger, Moelis & Company offered this information to the board of directors (mostly KKR and Shamrock):

On information and belief, Moelis instead presented potential investors with an appendix to its presentation-prepared at least in part by FanDuel itself-that indicated that FanDuel would be substantially more valuable if the Supreme Court overturned the federal prohibition on state-sanctioned sports gambling.

That analysis assumed annualized revenue gains for FanDuel ranging from $20 to $35 million in year 1 (2018) to $490 to $815 million in year 5 (2022), assuming, FanDuel obtained a conservative 5% share of the U.S. sports betting market. When combined with the expected growth of the daily fantasy sports business, FanDuel was projected to earn more than $1.1 billion in revenue within five years at an average year-over-year revenue growth of greater than 50%.

So, per Moelis, we have a high estimate of a roughly $20 billion “sports betting market” on the high end, implied by $1.1 billion in 2022 revs and 5% share. Lord only knows if thats all sports betting or online sports betting. No matter, just get the deal done.

++++

QUANTIFYING DEGENERAGY

What better place to look for answers to this TAM question than Flutter Group’s Annual Report.

Global betting and gaming market incorporates a wide array of products and services including sports betting, lotteries, casino games, poker and bingo. These products are offered in both land-based venues (such as casinos, betting shops and race tracks) and across online/mobile/ telephone channels. The total market is estimated to be worth c. £345bn. Since the late 1990s, online channels have grown strongly (estimated CAGR* of 10% in the five years to 2019) with online now representing c. 12% of the total market.

UK is a relatively mature gambling market but remains highly competitive. It is fully regulated and is estimated to be worth approximately £14bn annually (including lottery). The UK online sports and gaming market is worth c. £5bn with the UK retail market worth c. £3bn. Flutter Group (owner of Paddypower) estimates — UK online market is growing at 4-5% per annum. The Irish online sports and gaming market is worth c. €350m, slightly larger than the Irish retail market which is worth an estimated €340m.

The Spanish online betting market was regulated in 2012 and is worth an estimated €700m.Italy is the largest fully-regulated continental European online betting market, worth an estimated €1.7bn. The Swedish online market regulated in 2018 and is worth an estimated £700m. The Australian sports betting market is fully regulated and is worth an estimated A$5bn, with online and mobile accounting for almost 69% of the total market.

En toto Europe with 700million people, does roughly 25 billion Euros in Gross Online Gaming Revenues. Of that 42% or so are Sports. 10 Billion Euros, maybe.

With regards to the US Market :

Traditionally the market has been predominantly land-based, with online sports betting (horse racing) and gaming only available on a very limited basis at state level. In May 2018 the US Supreme Court overturned the Professional and Amateur Sports Act (“PASPA”), which effectively imposed a federal ban on sports betting across 46 US states. The growth opportunity in the US has continued to unfold quickly during 2019. We have been encouraged by the pace of regulation to date, with 14 individual states having now passed sports betting legislation. These 14 states account for c. 24% of the US population and with more states expected to follow, we are now increasingly confident that the total US addressable market for our products could exceed $10bn.

++++

A NOTE ON UK’S HIGHEST PAID EXECUTIVE AT £323 MILLION QUID

Who might this be? One Denise Coates of Bet365. A wonderful pure-play online betting concern. Founded in 2000. Think about that, 20 odd years to get to £3billion in revenues.

What you want to note about Bet365 is that roughly 40% is sports betting, and of that 79% is “in-play” betting or live betting, per company filings. Piking on the next point in the match is the holy grail.

Although Bet365 isn’t the first mobile sportsbook to enter the market (Colorado), their presence will be felt once they’re operating.

FIRST TO MARKET IN NJ DON’T MEAN SHIT

A list of the entrants in New Jersey, along with their back end “partners”, for your perusal.

Neat that they built their own DFS product, but the rest is off-the-shelf. Nothing makes them special.

. . . we built our whole Daily fantasy product from scratch and have always had pretty much full control over all aspects of it. And we have had — in a very quick time period, we went from having absolutely nothing on sports betting to being first to launch in New Jersey. And the only way we were able to do that was a big chunk of the product, the back end, we’ve been utilizing a third-party called Kambi to provide the betting lines and all the risk management and all that behind it, the trading and everything behind it. — Jason Robins DraftKings, Inc. – Co-Founder & CEO at MS TMT 03/05/20

Draft Kings uses Kambi for their back end, formerly part of Swedish online gambling giant the Kindred Group that provides B2B sports betting services for several top-tier operators, including Kindred and 888. The latter, is of course another late 90s era online gaming outfit, delivers about $560mil in revs whilst trading at $700mil cap — ticker 888.L for those of you intrigued.

Jason Robins DraftKings, Inc. Co-Founder & CEO @ MORGAN STANLEY 030520 :

. . . Australia is certainly a rabid betting market. But I think the U.S. is too. The U.S. people don’t realize it’s #3 in the world in gambling losses per capita, and that’s in a market that is actually not really well regulated and doesn’t have a robust online market. Australia is #1. But I think the U.S. has the potential to, on a per capita basis, be every bit as big as those. — Jason Robins DraftKings, Inc. Co-Founder & CEO @ morgan stanley tmt 030520 —

h/t @bubba

FINAL THOUGHTS

Quit telling yourself stories about a grande ol’ sports coming back. This is a customer acquisition tool at best, not the 800 pound gorilla in online sports betting. The DFS crowd will surely get excited about betting on sports and cross-selling is the name of the game.

Look to Flutter’s comments on FanDuel for a big-pic clue :

During 2019, we successfully leveraged our key US assets to acquire 285,000 additional sports betting customers, bringing our total US sports-betting customer base to over 350,000.

42% of our sports betting customers have come from the Daily Fantasy Sports database to date and cross sell into the New Jersey casino has accelerated significantly since we embedded gaming content into our sports app.

The FanDuel brand which resonates strongly, benefitting from a marketing investment of $130m during 2019 alone and over $600m to date. Average customer acquisition cost has been less than $250 since the sportsbook was launched.

Recent Results :

2019 Revs = $323 mil

2019 Net Loss = $142 mil (2x yoy)

1Q20 Revs = $0

Company cash burn to $15 million to $20 million per month (during shutdown)

$405 million cash

684,000 monthly unique paid users (MPUs) in 2019, up nearly 14% from 2018

Stock probably a Mersenne Twister rather than a compounder. Beware the short, culturally clumsy European operators could be in for a quick deal for brand awareness. $10 billion+ an unlikely sticker price.

When your PC hasn’t been touched all week, and you wake it from its slumber to find :

TAKE FUCKING NOTE

Fuck you very much, Eric Yuan. This is making jungle quite unhappy.

THE GENESIS

ZARA ZHANG: So the idea for Zoom first came to you when you were a freshman in college in China, right? Could you tell us that story?

ERIC YUAN: Yeah, that is a long story, but anyways. I was a freshman, my girlfriend was a sophomore. That was 1987, I think. She lives in another city. I was born in Mount Tai in the Shangdong Province. Between the city where she lived and the city where I lived was very far away. Every time I wanted to visit her, it would take more than 10 hours.

HANS TUNG: More than 10 hours?

ERIC YUAN: More than 10 hours.

HANS TUNG: One is the eastern side, one is the western side of Shangdong.

ERIC YUAN: No direct train either. I forgot, so probably at that time, you took the train and then probably in the middle of the night, you needed to change to another train. It was a very long journey. And also, I can only see her maybe twice a year, on the winter break or summer vacation.

Someday, I remember that actually. Someday if I can have a smart device and with just one click I can talk with you, can see you, that was my daydream, right? And every day I thought about that. But when I started Zoom, I started to connect the dots. It’s like wow, I thought about that before but the technology was not ready, but the idea was there.

but lucky for us, there’s translation . . . from 2017, so beware of dated information

Machines cannot take away translators’ job completely, but it plays its role in providing translation service by “matching” the right words.

How big is translation market? Zhou Feng, CEO of NetEase Youdao (网易有道), estimated it is a 40-billion RMB market. According to the 2016 China’s Language Service Industry Development Report, the value that China’s language service sector created in 2015 was about 282.2 billion yuan, an increase of 79% over 157.6 billion yuan in 2011. The average annual growth was about 19.7%. By the end of 2015, there were about 72,495 companies providing language services or language-related services in the country. Translation is indeed a big market, but not until recently did it begin to embrace the Internet.

NetEase Youdao has rolled out human translation services in 2012, tapping into the translation market by offering language service tool. Traffic is the advantage of tool products, but how to cash in on the traffic must be considered after the product is mature. Making money from ads is the most direct method, but the problem is that the ceiling is not high. Naturally, language and service products are connected. In addition to the word search and machine translation, there is also a need for more accurate translation services. Therefore, it is not surprising to see Youdao expanded its business from online dictionary to translation.

When it comes to development logic, Youdao Translation follows a path of “C to B”, that is, after a complete set of service system is established by serving consumers, Youdao will then serve the medium and small businesses and plan to cooperate with large businesses in the next stage. Liu Ren, Vice President of Youdao’s marketing department, mentioned that traditional translation companies focused mainly on B end and ignored C end users because of low demand and unit price, failing to offer specific solutions. The C end to B mode can be seen as prioritizing low-frequency translation demand over high-frequency. Low as the C end users’ demand is, their demand and willingness to pay is strong. Generally, they, looking for professional translation solution, can only seek translation service on platforms like Taobao only to find that the translation quality varies each time. Of course, the traffic that YoudaoDict has accumulated is a precondition for this logic.

According to the needs and content, there are two types of services currently available. One is fast translation, another document translation. With 0.02 yuan/word as the charge, the former applies to users who set a tight deadline and everyday content like business correspondence. The latter applies to professional content or relatively large volume, whose charges depend on the content. According to the data provided by Youdao, from 2012 to date, the total number of Youdao Translation orders has exceeded 1 million, with 1000 orders per day and a nearly 100% increase of human translation orders per year.

Similar to the traditional translation company’s business model, Youdao Translation outsources orders to over 3000 translators. For fast translation content, translators can “grab orders in the background”. For document translation, project managers will “assign translation task” in accordance with the translators’ professional background. And project managers are responsible for the quality control of translation results and customers’ feedback. For B end, Youdao has launched the human translation API service. Specifically, Youdao cooperates with B end customers and sells its translation service by offering API interface and embedded SDR model.

Overall, on the premise of similar service model, compared with the traditional translation services, the advantage of Youdao is mainly at the technical level. That is, its human translation is not “pure human labor”. Rather, based on NMT (Neural Machine Translation) technology, Youdao adopts an approach of “man-machine translation”, that is, after the machine finishes the first draft, translators do follow-up examination and make improvements, bringing down the overall price by 50% compared with human translation.

The other reason why the human translation business is a rigid demand is that much of the free machine translation does not make sense. So, with the emergence of neural network machine translation, will human translation be replaced? At least the Google case indicates there is still a long way to go. Some translation scenes emphasize “faithfulness, expressiveness, and elegance”, but at present NMT technology can only meet the requirement of “faithfulness”. Although it does improve the accuracy of content translation, human engagement is needed if translation involves “expressiveness and elegance”. Therefore, at this level, machine cannot replace human entirely, instead it plays its role in providing translation service by “matching” the right words.

On top of Youdao, Baidu, Jinshan (金山), and the voice-recognition technology company— IFLYTEK(科大讯飞) all tapped into the translation market by offering language service tool. In addition, 36 Kr wrote that Wormhold (虫洞)Translation, modeled on Taobao, built a platform to serve translators and customers. As a whole, the translation market has become white hot due to low threshold for standardization. Of course, compared with the interpretation , a greater demand, sufficient supply of translators, and the lower cost is also add to the fierce competition.

in more recent news:

this stupid pen known as the : Translation Pen Scanner – Netease Youdao Dictionary Pen 2.0 for Word and Sentence Translation for Chinese and English – Digital Highlighter and Reader – Wireless — is selling like gangbusters.

per 3q19 call :

In the third quarter, revenues from our intelligent learning devices increased by 707% year-over-year. We released the second-generation Dictionary Pen in August. Within 2 months of its release, the second-generation Dictionary Pen became the best-selling product on JD.com under the digital dictionary category, with a positive customer review of over 99%. In the meantime, we continue to expand sales channels for our intelligent learning devices.

also per 3q19 call:

Our total net revenue for third quarter of 2019 was RMB 345.9 million or USD 48.4 million. This represents a 98.4% increase from RMB 174.4 million in the third quarter of 2018. Our net revenue are comprised of the 2 segments, learning services and products, and our online marketing services. Net revenue from our learning services and products were RMB 225.2 million or USD 31.5 million for the third quarter of 2019. This is up by 141.6% from RMB 93.2 million for the third quarter of 2018. We attribute this growth to the strong growth in the K-12 paid student enrollments and the increase of ASPs.

Net revenue from the online marketing services were RMB 120.8 million or USD 16.9 million, a 48.8% increase from the same period in 2018. The increase was primarily attributable to increased distribution of advertisement through third parties’ Internet properties.

gross margins:

Gross margin for online marketing services were 22.6% for the third quarter of 2019 compared with 39.5% for the third quarter of 2018.

SEA TURTLES WANT TO COME TO THE U.S. of A. DAMMIT – – – AND THERES NOTHING YOU OR YOUR STUPID CORONA VIRUS CAN DO ABOUT IT — GOD BLESS MURKA.

Mon Feb 10, 2020 11:28am ESTComments Off on THE IMPORTANT MATTER OF EXCELLENCE AND TRASH $MO $BREW

jungle is tired of garbage and mediocrity. junk and trash and junk and trash. all for a pretty penny no less. after a long sojourn, jungle is back in the saddle of the nor’east. gloomy, wet — it has its own charm, if you have a roof over your head, of course.

as you all may know the cancer-as-a-service business known as – altria has been on sale for sometime. trading at somewhere under ten times earnings, while assigning zero to juul.

one fintwitter said it best : “huge installed base of subs that churn at a rate of 0.3% per month. ever increasing arpus as subs face massive lock-in, and huge switching costs. juul actually lowered the industry cac. all metrics except sub growth up”

meanwhile, it of course also owns a stake in ab inbev.

Altria holds 56.8 % of the restricted shares representing 9.45 % of the total number of AB InBev shares excluding treasury shares as at 31 December 2019. In addition, Altria announced in its Schedule 13D beneficial ownership report on 11 October 2016 that, following completion of the business combination with SAB, it purchased 11,941,937 Ordinary Shares in the company. Finally, Altria further increased its position of Ordinary Shares in the company to 12,341,937, as disclosed in the Schedule 13 D beneficial ownership report filed by Stichting dated 1 November 2016, implying an aggregate ownership of 10.08% based on the number of shares with voting rights as at 31 December 2019.

and it follows that the purveyor of swill, just finished off buying $brew (kona, widmer) as of november 2020. less shitty beer, but still shitty if you will.

you may have heard:

CBA would join A-B’s high-performing Brewers Collective — a collection of craft partners spread throughout the country committed to providing consumers with innovative, quality beers and investing in their local communities. In the last three years alone, A-B has invested more than $130 million in its craft partners, allowing them to expand their production volume by an average of 31 percent. A-B’s craft partners have created nearly 1,000 new jobs in their home communities to support their growing breweries.

A-B currently owns a 31.2 percent stake in CBA and has offered $16.50 in cash for the remaining shares.

which brings me to the matter of excellence. jungle has already fired off a missive about shitty brews. shitty brews have mass appeal. in fact, most shitty things have mass appeal. and this is one very important matter that we must meditate on as rent-seekers. excellence and cash flows are not correlated. remember that, dear penii.

for now, please read about the excellence of one shaun hill and his brews.

A pilgrimage to visit Shaun Hill, elusive guru of the beer geeks.

Meet Shaun Hill: notorious perfectionist, philosopher, and producer of the most-sought-after beer in the country.

To get to Vermont’s Hill Farmstead brewery, the best brewery in New England and arguably in the country, you have to follow meandering back roads, each marked with gnarled street signs that are either falling down or pointing into overgrown pastures. Hill Farmstead is located in Greensboro, just 40 miles from the Canadian border, and the town’s dirt roads look as if they were freshly carved out of the earth with a backhoe. GPS won’t help you here—coverage is spotty, when you can get it at all, and Google hasn’t bothered to map large swaths of the geography. As you traverse unmarked paths, stretching in front of you as craggy and pocked as the surface of the moon, you’ll feel your resolve being challenged with every wrong turn.

Once you crest the hill and come upon the blond siding of the brewery, you may find yourself awash with emotion, not only because you’re that much closer to procuring some of the world’s most-sought-after beers—but also because your sense of equilibrium has returned. You’re back on terra firma.

When I visited in October, snow had already blanketed much of the stark landscape, and Brian Hill was directing visitors into impromptu parking spots to the right of the barn. After recovering from a logging accident, Brian accepted a part-time job at the brewery washing kegs, pumping wastewater, and acting as the site’s unofficial parking-lot liaison. People don’t come here for Brian, though. They come here because of his son, Shaun Hill, a single-minded, ambitious brewmaster who, at 35, has helped make Greensboro one of the can’t-miss destinations for beer pilgrims around the globe.

Even at 10 a.m., two hours before Hill Farmstead opened its doors, there were more than 100 people in line, mostly men outfitted in logoed beer hoodies and mesh trucker hats embroidered with some of their favorite haunts: Allagash, Maine Beer Company, and the Prohibition Pig. I took my place next to a trellised overhang sheltering a mountain of stainless steel kegs. The early-morning congregation was making small talk and shuffling from foot to foot, the clinking of their growler-filled canvas beer coolers echoing across the frigid late-autumn air like wind chimes.

“You here for Art?” asked the guy behind me. Art, a barrel-aged farmhouse saison, scored 100 out of a possible 100 points on RateBeer, a leading review site. “Because if you don’t want yours,” my neighbor continued, “I’ll buy it off you. I’m serious. We’re only allowed to buy one bottle, and I want to get as many as I can before heading back to Jersey.”

For most of the smaller craft breweries, attaining a perfect score with even one beer can prove difficult, but Hill Farmstead seems to dash them off by the dozens. This feat is even more impressive considering Hill Farmstead’s minuscule annual production of around 3,000 barrels a year. To put that in perspective, Delaware’s Dogfish Head brewery produced 200,000 barrels in 2013. Craft-beer pioneer Ken Grossman and his company, Sierra Nevada, reached as many as a million barrels in 2014.

But even among Shaun’s secluded fun house filled with wild yeasts and hundreds of used wine and bourbon barrels, Art is a true anomaly. Whereas most Hill Farmstead beers—much like popular IPAs from Sierra Nevada and Harpoon—ferment over several weeks, Art takes years. Shaun’s manic drive to reach transcendence, even if it means pushing a beer to its absolute breaking point, is one of the things that separate his beers from the rest of the pack. But that’s no guarantee that the Art you drink will always be perfect. “Oh man, did you try the last batch?” a guy in front of me interjects. “Something was definitely off. It was corked or something. I wanted to return it.”

It’s a common complaint among Shaun’s many devotees, who trek to Vermont knowing that his unorthodox methods sometimes produce the world’s greatest beer—and, other times, less than perfection. Like wine, which lives and mutates inside its bottle, Shaun’s beer can be unpredictable, and has become part of the brand’s mystique.

As we wait in 40-degree temperatures, the conversation in line turns to Shaun’s rumored upcoming releases—“I heard he’s working on a batch of Earl”—which kegs are running low—Double Citra is supposed to kick before noon—and whether the truly ambitious among us have time to drive up to Newcastle, Maine, for an event at Oxbow Brewing Company. There’s even some conjecture about Shaun’s love life. The guy behind me—the one angling for my supply of Art—is speculating about rumors that Shaun has dated a cheese maker at Jasper Hill Farm. “They were like Vermont royalty,” he says. “The king and queen of all things craft.”

Hill uses local malts in his award-winning beers. / Photograph by Pat Piasecki

I can’t help but stare at the weathered exterior of Shaun’s childhood home, its second-story window peaking just above the corrugated roof of the keg shed. In the intervening years, Shaun’s parents moved into a different house across the street, but Shaun remained. Today, its gray façade appears lifeless, the windows black and still. But I feel eyes watching me, like Shaun is up there in the shadows, surveying the chaos below—a bemused demigod, like Kurtz in his Congo kingdom.

An abrupt silence falls over the lot as an employee charges outside and announces that they’ll be opening early to accommodate the growing throng. As we crowd inside the taproom to fill our strict five-growler limit, the conversation inevitably turns to the architect behind this shrine to hops and barley. The bready aromas of yeast and caramelized malt hang heavy in the air, but nothing is more palpable than the omnipresent Shaun Hill, the auteur who has been lauded by everyone from Vanity Fair to the New York Times, the wunderkind who built the world’s best brewery two years ago, at just 33 years old.

With about 40 breweries in the state, three of which repeatedly make RateBeer’s list of the best in the world, it’s no wonder that Men’s Journal has declared Vermont the Napa Valley of the beer world. In measuring breweries per capita, Vermont rivals the country’s craft-beer strongholds: It’s in a dead heat with Oregon, and easily eclipses Colorado. This meteoric growth, however, is a new phenomenon.

Shaun can remember with clarity when Magic Hat #9 showed up on the shelves at the Willey’s Store in Greensboro, where he worked when he was 15. The appeal of its offbeat, psychedelic label inspired Shaun to become a home brewer and craft-beer convert well before the legal drinking age. But that desire to own and operate a brewery? That didn’t take hold until much later in life.

After graduating from Haverford College, outside of Philadelphia, with a degree in philosophy, he returned to his hometown and settled into a life of odd jobs: painting houses in the summer, tutoring, and washing tanks at night at the Shed, a local brewpub.

In a moment of serendipity, the head brewer there left his position while Shaun was on vacation in Europe tasting the world’s best beers, his passion for the craft reaching fevered new heights. When he returned home, the Shed let him take over. Shaun, however, was immediately bored by the mundane canon of browns and ambers that dominated the draft lines—not just the Shed’s, but most brewpubs’ in the early aughts.

That’s when he found salvation in the pages of Yankee Brew News, and its profile of John Kimmich’s upcoming seven-barrel brewpub in downtown Waterbury, 40 miles away. Kimmich had created Heady Topper—once the top-rated beer in the world—and Shaun was eager to pick his brain. “Yeah, he was around a lot, to put it bluntly,” Kimmich says. “When he first got that job at the Shed, he started coming in all the time. He would come down into the brewery and ask questions and show interest. I don’t really talk nuts and bolts with just anybody, but I could see he was way into it.”

Another break came when he discovered that Anders Kissmeyer, a standout Scandinavian brewer who had broken off from Carlsberg to found Nørrebro Bryghus, was specifically looking for an American to head up his Copenhagen brewery. Shaun left his life behind in Vermont to work and train overseas, an opportunity he didn’t take lightly. Kissmeyer says he came in with a bullish, uncompromising attitude. The two brewers became fast friends, a rapport that was no doubt strengthened by Shaun’s dogged work ethic and what Kissmeyer calls his “impeccable skills” in the brewhouse. Within six months Shaun took over Nørrebro Bryghus’s barrel-aging program, and in 2010, he won two gold medals and a silver at the World Beer Cup, a global contest often referred to as the “Olympics of beer competitions.”

But the pull of home overtook Shaun. So he found a group of investors, who raised $80,000 to turn his family’s farm in Greensboro—a town his ancestors helped found in the 1780s—into the type of farmhouse brewery he’d long admired. Within the year, RateBeer anointed Hill Farmstead 2010’s Best New Brewery in the World, the national media began taking note, and Vermont suddenly became a tourist destination for beer fans as far away as Australia and Japan.

“When he went off to Europe, that’s when he really began expanding his horizons,” Kimmich says. “He obviously made a good decision, because when he did get back he was ready to get rolling.”

hill farmstead

Only a small crew of trusted employees get to help Hill out with his brewing. / Photographs by Pat Piasecki

Despite the fan-boy craziness out front, making beer at Hill Farmstead is not glamorous work. On the morning of December 9, there are already a swelling number of crises.

A water-heating unit on one of the tanks is busted, and the lug nut holding it in place is calcified with old beer. Shaun is grunting and pulling on a heavy-duty pipe wrench, but the thing isn’t budging. Chalky white deposits are now spewing into Shaun’s newest batch of Edward pale ale, and he’s yelling at me to twist nozzles and push buttons on a control panel above my head. “Hey, there you go, you just had your first professional brewing assignment,” he says, panting and dripping with sweat after having finally released the rusted coil.

A local farmer has arrived with a truck full of frozen plums for Shaun’s latest iteration of Flora, a wild farmhouse saison aged on various organic fruits; a walkie-talkie at his hip keeps erupting with questions from his cellar man; and several of the new tanks that arrive are the wrong size and won’t fit into the snug dimensions of the loading bay.

Due to his brewery’s breakneck growth, Shaun is expanding his operations for the second time in as many years. Given the limitations of the rough-hewn roads surrounding Hill Farmstead, Shaun insists it’ll be the last, at least above ground. Not only will the additional square footage make space for a sleek new taproom in early summer, it will also allow the business to double its capacity and distribute its beers outside of Vermont for the first time ever. Even today, bartenders selling Shaun’s beer in other states, which happens all too often, have been doing so illegally.

“It worries me to think what would happen if we didn’t have limits on the amount of beer you could buy,” says Shaun, who has launched a social media campaign to publicly shame retailers and bar owners who unlawfully sell his beer. “We’ve had people buying growlers and going back to Washington, DC, and serving our beer from their bars out of growlers [which have a short shelf life]. I feel like there’s this unsaid, unwritten understanding between publicans and brewers: ‘Don’t be a douche.’ There are certain things that you just don’t do. Selling from a growler? But the almighty dollar, man, that’s all that matters to some people.”

Eternally in a semi-permanent state of dishevelment, as if he hasn’t slept in days, Shaun’s guise doesn’t exactly scream perfectionist. The errant wrappers and foodstuff surrounding his laptop speak to a steady diet of wild-boar jerky, roasted peanuts, and Cuties clementines. His clothes emanate a pungent musk that seems to even give him pause, as he leans in at one point during our conversation and sniffs one of his armpits. But Shaun is striving for perfection in his beer, and it pains him to see it mishandled and compromised by illegal vendors.

Before kegs of Abner, Edward, and Everett Porter, for instance, can make their way into Massachusetts and New York, Shaun is drafting a quality-control manual for businesses interested in pouring his beers. Examples of his edicts include the type of non-chlorinated soap to use when washing glassware, the temperature at which to store kegs and bottles, and how often to flush draft lines.

This type of control and stewardship is the natural next step in Shaun’s development as a brewer. He wants to take his beer into uncharted territory, shifting into something closer to wine, with the “elegance” and “palatability” more comparable to white burgundy than the high-alcohol hop bombs that dominate craft beer today. He’s even become a regular at Moët Hennessy in Champagne, where he’s learning cellaring tricks from heralded Dom Pérignon chef de cave Richard Geoffroy.

In his quest to follow in the footsteps of the wine business, Shaun sees his future underground, like the cellars of France. He might never add another fermentation tank or encroach upon the pastoral landscape of his farm again, but he does plan to dig below the surface, where he can build a 5,000-square-foot cave dedicated to cherished barrel-aged projects such as Art, Civil Disobedience, and Genealogy of Morals. And like the wine world’s grand cru burgundies, or its most storied champagne houses, Shaun says beer—at least his beer—should approach something close to the sublime.

“One of the most interesting things anyone has said to me was Richard [Geoffroy] from Dom Pérignon, who said, ‘In the end, luxury is emotion,’ which I think is amazing,” Shaun says. “How does it make you feel? If it makes you feel good, then it’s luxurious. What makes chocolate or our beer a luxury? It’s the emotion that it evokes. If it does nothing for you, well, then I pity you. You have to enjoy things in this world. Pushing yourself to grow and pushing yourself to be transformative, well, that’s what brings me joy.”

An esteemed member of the hallowed halls @rock brought the rort known as $AIMT to Jungle’s attention. Jungle has things to do, places to go, people to see. Howevever, this nonsense has gripped Jungle over her 6th cup of tea. Jungle is living an asynchronus life at the moment and lacks the gusto for a true missive. However, the inane mosaic is presented, with low-grade disgust. First and foremost understand this:

The Global Hand Sanitizer Market size was valued at $919 million in 2016 to reach $1,755 million by 2023, and is anticipated to grow at a CAGR of 9.9% from 2017 to 2023. Hand sanitizer is an antiseptic solution, which is used as an alternative to soap and water. It is used to prevent the transmission of infection, which is majorly caused through hand transmission, further causing several diseases such as nosocomial food-borne illness and others

Wash your stupid hands with soap and water and quit using these idiotc products. The FDA itself questioned the efficacy of this bullshit.

New safety information also suggests that widespread antiseptic use could have an impact on the development of bacterial resistance

Meanwhile Dr. WoodCOCK had this to say:

“Today, consumers are using antiseptic rubs more frequently at home, work, school and in other public settings where the risk of infection is relatively low,” said Dr. Janet Woodcock, director of the FDA’s Center for Drug Evaluation and Research.

Your useless spawn are not only little weaklings, but you are fomenting their inability to cope.

++++

Jungle is spent, and has little vitriol left for the day. After all, its past 0100GMT. Almost time for high tea at The Palace, bullshit institution that it is. Applause to H&M for attempting to change the rules of the game.

Back to fucking peanuts. What a bogus ass “problem” — likely invented by the CABAL. Let us take a look at some stats, shall we? We already know the obvious : allergies of all ilks are on the rise. But peanut allergies in particular are “in fashion”.

The epinephrine market is expected to exhibit a CAGR of 11.0% during the forecast period (2018 – 2026), attributed to increasing number of generic cost-effective auto-injectors in the market, and strategic support of companies and government agencies for increasing generic epinephrine adoption. Furthermore, pipeline of epinephrine products is increasing and this is expected to fuel the market growth over the forecast period.

Moreover, increasing incidence of anaphylaxis associated with food allergy is driving the market growth. According to a research conducted by the Centers for Disease Control and Prevention (CDC) in 2013, in the U.S., between 1997 and 2011, food allergies among children increased around by 50%.

Moreover, according to the European Academy of Allergy and Clinical Immunology (EAACI), over 17 million people in Europe were affected by food allergy in 2015.

Market growth is attributed to approval and launch of cost effective generic epinephrine products. For instance, in December 2016, Mylan introduced an authorized generic option to EpiPen (epinephrine injection, USP) Auto-Injector with a different packaging and same drug formulation, which was available at 50% lower prices than its branded version.

Some of the major players operating in the global epinephrine market include Mylan N.V., Pfizer, Inc., Teva Pharmaceuticals Industries Ltd., Impax Laboratories, Inc., Kaleo, Inc., Adamis Pharmaceuticals Corporation, Bausch Health Companies, and ALK- Abello A/S.

++++

CABAL: NEW ENGLAND JOURNAL OF MEDICINE HAS BLESSED AR101

But while preventing all food allergies is clearly unrealistic, researchers are making remarkable progress in developing better treatments—therapies that, instead of combating symptoms after they’ve started (like epinephrine or antihistamines), aim to make patients less sensitive to allergens in the first place. One promising approach is oral immunotherapy (OIT), in which patients consume small but slowly increasing amounts of an allergen, gradually reducing their sensitivity.

A study published last year in the New England Journal of Medicine showed that an experimental OIT called AR101, consisting of a standardized peanut powder mixed into food, enabled 67 percent of participants to tolerate a dose equivalent to two peanut kernels—a potential lifesaver if they were accidentally exposed to the real thing. Because OIT itself can trigger troublesome reactions in some patients, however, it’s not for everyone.

Another experimental treatment, sublingual immunotherapy (SLIT) uses an allergen solution or dissolving tablet placed beneath the tongue; although its results are less robust than OIT’s, it seems to generate milder side effects. Epicutaneous immunotherapy (EPIT) avoids the mouth entirely, using a technology similar to a nicotine patch to deliver allergens through the skin. Researchers are also exploring the use of medications known as biologics, aiming to speed up the action of immunotherapies by suppressing IgE or targeting other immune-system molecules.

One downside of the immunotherapy approach is that in most cases the allergen must be taken indefinitely to maintain desensitization. To provide a potentially permanent fix, scientists are working on vaccines that use DNA or peptides (protein fragments) from allergens to reset patients’ immune systems.

++++

CABAL: FASTRACKED BY FDA

The BLA for AR101 was originally accepted in March 2019, with an original review target date of late January 2020. The biologic was previously granted Fast Track and Breakthrough Therapy designations for peanut-allergic children and adolescents aged 4-17 years old. The once-daily peanut allergen therapy gradually desensitizes patients from allergic reactions, symptoms, and anaphylaxis.