Tokyo based, expat Cape Bretoner. Learning to live in a de-leveraging world. Better suited to the crusades. CFA & FRM charter holder.

Disclaimer: @Firehorsecaper reminds investors to always perform their own due diligence on any investment, and to consult their own financial adviser or representative when warranted. Any material provided is intended as general information only, and should not be considered or relied upon as a formal investment recommendation.

I had the pleasure of hearing Singapore based Mark Mobius, Ph. D. (Economics, MIT) Executive Chairman, Templeton Emerging Markets Group keynote speech at the Asia PE-VC Summit 2016 held 30 September 2016, run by Deal Street Asia / mint asia.

Dr. Mobius was born August 17, 1936 (six years younger than Warren Buffett, born August 30, 1930). Nobody can rock a baby blue two piece suit and white shoes better than Mobius. Style and substance are rarely brought together in such a seamless fashion. At 80 year young, he is beyond sharper than a tack and offered a great deal of insight to a crowd, on average 45 year his junior.

Templeton has $28bln invested in 70 global EM markets at present, sprouting from a kernel of $100 million circa 1987. In South East Asia, the focus has been on PIPE deals (Private Investment in Public Equity). EM is up 1848% over the 1987-2016 period.

What keeps Mark up at night, other than travails of being 80, can best be summarized as the three i’s;

1.) Interest rates – Global Central Banks are the classic non profit maximizing counterparty and Mobius thinks they are destined to “make a mess” of it. Negative interest rates are far from a rational state. In terms of rational equity valuation, almost any p/e multiple can be justified in an environment of negative rates, 100 OK, 200 sure. Mark questions the mentality of said central bankers, overly influenced by academia, economist and other charlatans (my term). Specifically called out was Ken Rogoff’s “Curse of Cash” as poppycock.

2.) Isolationism – Both with respect to trade and investments. A damaging trend. Little comment required on this point. Mobius grew up in Boston, Mass. but long ago relinquished his US passport and holds a German passport (his father was German and his mother was Puerto Rican) and a Singapore tax domicile.

3.) Internet – On-going game changer, especially in EM. Largely a mobile phenomenon.

China, still a monster growth story. It is all about the absolute numbers. Growth is slowing, but the absolute numbers are bigger every year (10% growth in 2010 is smaller than 7% in 2015 given the absolute size of the economy).

Biggest take away:

The people you are dealing with is the most important factor in investing, over the long haul. Having a legal agreement is of course required, and governing law important, but typically if it gets to the stage of lawyers and the courts, the result is a big zero for all involved. Word to the wise, word to the wise indeed.

My current public market favorite instrument for EM exposure is WisdomTree’s Emerging Market High Dividend ETF, DEM, yielding 4.15%, ytd 2016 performnance +20%, AUM $1.6bln. No home country bias, as a global citizen. JCG

Follow me on twitter; Caleb Gibbons @firehorsecaper

Even the Asian elephant in the room is endangered.

Over 80% of the market value in the S&P is attributable to intangible factors (environmental capital, sustainability governance and stakeholder relationships). Less than 20% is accounted for by physical and financial assets.

Global sustainable investing assets grew by 61% over the 2012-2104 period and now stand at $21.4 trillion. The domicile of these assets is telling; 99% are in the United States, Canada and Europe.

Environmental and social issues affect both valuation and financial performance. If your investment decisions focus only on financial disclosures, you will not be getting a complete picture of the drivers of value.

Global ethical principles have never been more important or, it appears, more wanting than in current times (i.e. VW, Phoney Express aka Well Fargo, global Trumpism, and global lawsuits imperiling not just returns but the very viability of global commerce beyond national borders).

The UN supported Principles for Responsible Investment (PRI) ,a not-for-profit organization, held their 10th anniversary conference in Singapore last week (Sept. 6-8th) which I attended. No conference bag full of binders and junk mail at this conference, your 1 page agenda fold up into your name tag and all meals were vegetarian, a subtle but effective message. Forbes Magazine The conference domicile was not chosen by chance. Asia has been termed the cradle of disorder for a reason, it is home to 5 of the world’s 7 billion population and on metrics of social investing if the game has even started it is is the 1st inning. When a region has practices like dynamite fishing and farmers still clear land with a match much work lies ahead.

Chris Sanderson, Co-Founder of The Future Laboratory focussed largely on the sustainability of the capital markets. He characterized global citizens as being tired of austerity, wary of politicians and perhaps even more wary of brands. Backlash culture; http://shop.thefuturelaboratory.com/products/backlash-brands-report.

Elliott Harris, Head of the United Nations Environmental Program (UNEP) gave a rousing speech on environmental and social sustainability. The end game is that all investments will be social. Elliott introduced the concept of thick profit versus thin profit, a concept akin to quality, hard to define, but you know it when you see it.

Georg Kell of Arabesque Partners Arabesque spoke of Generation S, a cross-section of all age groups working towards making the world a better place, one worthy of handing down to future generations. While ESG (environmental, social & governance) alpha may prove illusory, ESG smart beta appears to have legs.

Millennials were of course discussed with the most shocking realization being that the oldest ones (born 1990) are in their mid 30’s now! Generation D (Digital), whose only need or want in life is wifi and lithium, was out in full force, albeit well behaved and overall attentive. The 600 conference attendees were largely baby boomers, representing approx. 50% of global financial assets under management (AUM), signatories to the PRI whose mission states, “We believe that an economically efficient, sustainable global financial system is a necessity for long term value creation. Such a system will reward long-term, responsible investment and benefit the environment and society as a whole.” Clear, concise, devoid of the typically mumbo jumbo one gets when issues like climate change and the environment are normally tabled.

The session run by GS alum David Blood, Managing Partner at Generation Asset Management Generation Investment Management was excellent. Al Gore is the Chairman of Generation Investment Management. If Obama delays the election to allow Clinton to get her legs perhaps they could run as a Third Party choice? Could not lose with the ticket “Blood & Gore”. Both men can readily point out Aleppo on a map too. In any event, David’s sage words rang true to all in attendance. Finance and capitalism is not working for everybody was a key statement. The transition to a low carbon economy will clearly not be an easy one. A full 1/3 of aggregate world equity and fixed income market value lies in the cross hairs. We can do this the hard way or the easy way, but de-carbonization is a trend now moving under its own power. Mr. Blood noted that while the majority of global asset managers in attendance (120 signatories, 50% of global AUM) were managing to sustainability factors, those not present (i.e. non PRI Signatories) are largely American. The reasoning to date for USA firms reluctance is that becoming signatory could put them in breach of their fiduciary duty. We must collectively get the remaining 50% on board as priority #1.

Investing for the long term. Short termism. A great panel on investing for the long term had some serious panel power. The headliner was Hiro Mizuno, CIO of Government Pension Investment Fund, Japan (GPIF), the world’s largest funded pension plan. GPIF manage their liabilities to a 100 year time frame. Their most recent result showed a loss of ¥5.3tln (US$5.2bln) for the current fiscal year through March 2016. The fund’s quarterly loss through June 30, 2016 was > ¥5tln (-3.88%). They run ¥130 trillion (US$1.27 trillion) leading Mizuno-san to characterize the latest qtly loss as peanuts. The joke was not well received, perhaps because it was so unexpected, leading Hiro to quip that perhaps there were Japanese pensioners in the audience. The fund increased their allocation to equities in recent years. Global equity investment totals US$600bln, 80% of which is allocated in a passive fashion and 20% ($120bln) of which is actively managed. All investment are mandated to external manager, counter to the global trend in the pension arena of in-sourcing. Fellow panelist Paul Smith, President & CEO at the CFA Institute noted that one advantage of being old is that “you see everything twice” with such decisions as out-sourcing vs. in-sourcing set to very long term market cycles.

Several panels touch on infrastructure finance with GPIF mentioning their joint investment effort with Canada’s CPP on ESG brownfield infra projects. Mizuno-san noted the challenges of crafting/originating greenfield projects as funding challenges often drive the cheap option and the cheap option is usually dirty (materials, supply chain, etc.). GPIF will not finance dirty deals, full stop.

A deeper discussion ensued on better was to measure and compensate performance with a general aversion shown to managing to qtly earnings guidance. The average hold period for SPY, the > $100bln S&P 500 SPDR, the largest ETF tracking the benchmark for US stocks is 5 days. In the last 15 years 52% of the Fortune 500 companies as no longer in existence. In 1955 the average Fortune 500 company life expectancy was 55 years, in 2015 it is 15 years. Traditional valuation metrics clearly must evolve to address the realities.

The ESG investment construct must be turned on its head, to my mind. Social investing = investing and “dirty” or non-socially minded investment should be the type requiring explicit sponsor/board/member approval. JCG

Follow me on twitter @firehorsecaper

Shenzhen “beach” September 2016

Mark Carney, Chair, Financial Stability Board (FSB). Awesome 30 minutes of your life, watch it. Carnage, indeed.

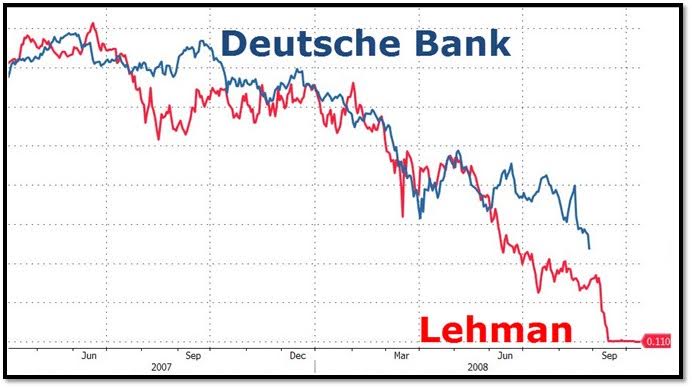

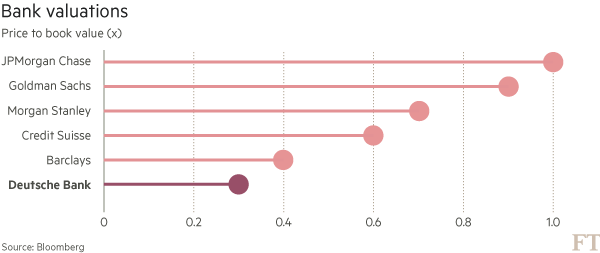

“Here be Dragons” means dangerous or unexplored territories, in imitation of the medieval practice of placing dragons in uncharted areas of maps. With respect to considering an investment in Deutsche Banks’s (DB) equity, I would argue we are instead dealing with “known unknowns”, as Rummy would put it.

Much of the risk and potential upside going forward hinge on non-financial risks, legal being #1. DB has now paid $9bln in fines, 1/2 their current market cap of $18.2bln, for various settlements post GFC. No opinion to provide on the validity of any given case from a merit or $ perspective, but clearly through a process of elimination, DB is closer to the end of the financial spartan race. The ability of John Cryan, chief executive of DB, to reduce the dominance of litigation charges from results going forward will dictate the very survival of the bank that led the financing of Germany’s economic miracle post WWII. Those drawing parallels to Lehman are data mining in my view, DB is too important to the German, European and Global banking/financial system to be euthanized.

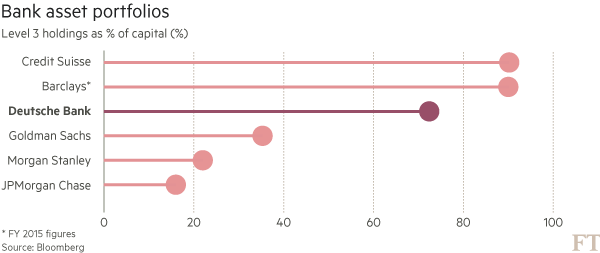

€31bln of Level 3 assets remain on balance sheet, but this is down 65% from the peak of €88bln in 08′.

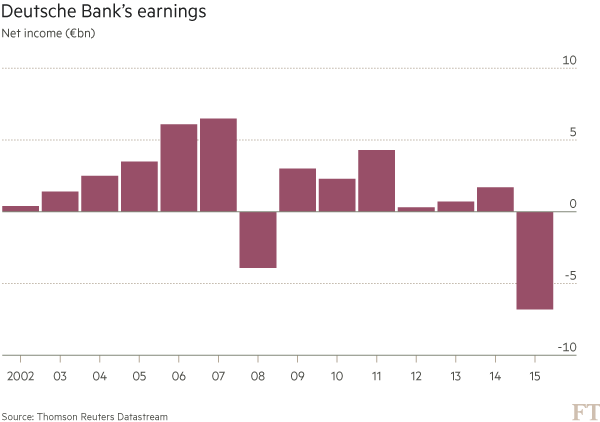

2015 was the kitchen sink year for Deutsche Bank. Litigation costs and re-structuring charges led to a €6.8bln reported loss. GM was once appropriately described as a health-care company that also made cars. DB is a law firm that dabbles in the capital markets and asset valuation. Modest earning are expected for full 2016 ($1.11 per share), but the first “clean” year expected by chief executive John Cryan is in 2018.

Fixed Income Currencies & Commodities (FICC) has become a dirty 4 letter acronym for many players in the capital markets in an environment of ZIRP, since trumped by NIRP. The transition from Anshu’s Army (once responsible for 85% of DB “earnings”) to Cryan’s Janitors has clearly hampered returns. DB was a top 3 players over the 2008-2014 period, earning approx. 20% “share of wallet” in FICC. This share has slipped to 17% and is not trending well, with share ceded to venerable competitors like JP Morgan (JPM is now trading at 1x book versus 0.25x for DB). Approximately 1/3 of the slippage has been expected as DB exited high risk weighted asset (RWA) businesses they no longer have an edge in. Risk reduction efforts include improving the leverage ratio (CET1/total adjusted assets) to 4.5% by the end of 2018 and 5% by 2020. DB has run with leverage as low as 2% previously and the leverage ratio currently stands at 3.4%. Daily VaR (99% confidence interval), has dropped 57% since 2007, from €86mm to €37mm. Liquidity reserves (HQLA- cash and highly liquid government, agency and government guaranteed bonds and other Central Bank clearable securities) as at Q2 2016 stand at €223bln, up 243% from 2007’s €65bln. As a result DB’s liquidity coverage ratio (LCR) stands at 124%, well ahead of the 100% required by Jan. 1, 2019 under B3.

Price to book and price to tangible book have become somewhat interchangeable terms in analyzing bank stocks post GFC. Few have sizeable goodwill yet to be written down. To temper expectations, DB would likely be over the moon if they could get back to 0.6x P/TNAV by the end of 2017 which would put the stock back in the high 20’s, roughly a double from the US$14 it stands at now (NYSE listing). This would put DB in line with where Citi trades, on a metric of price to tangible book. The list of global banks that trade > 1.0x book is dominated by the Canadian and Australians (i.e. RY at 1.9x and WBK at 1.7). Wells Fargo & Company is the rare American that trades at a premium, 1.4x book at present.

The “to do” list for DB by the end of 2018 is long, but achievable; a 10% return on tangible equity, a leverage ratio of 4.5%, a 12.5% CET1/RWA (10.7% at present), efficiency ratio of 65% (perhaps the most challenging metric to achieve, low 70’s arguably more achievable interim step), and achieving €3.5bln per annum in cost savings by cutting 30,000 staff and the exiting 10 non-core markets. In their home market of Germany, plans include selling their remaining stake in Deutsche PostBank AG and closing >25% of their 700+ retail branches.

DB is currently rated Baa2 with Moody’s (Senior Unsecured Debt), BBB+ with S&P, and A- by Fitch. The most recent 5 year CDS level for DB was 216bp (JPM in comp. is 60bp).

The largest dragon investors worry about with respect to DB is their sizeable otc derivatives book. The focus on headline notional exposure of €46 trillion materially overstates the true economic risk. Looking at the €46 tln notional amount of contracts across fx (27% of net exposure), rates (54% of net exposure), and index/equity (12%) can be daunting, but as with other areas noted, steps are being taken to reduce the size and improve the liquidity of their derivative books. DB intends to exit the CDS business for one and has novated over 2/3rds of their book to other cptys since 2015 (JP Morgan the biggest CDS player by wide measure). The previously noted number for level 3 assets include level 3 derivative related assets (DRA). As with the rest of the market, the vast majority of DB’s derivative contracts are centrally cleared. Those contracts not centrally cleared (i.e. bi-lateral contracts) are typically collateralized above rating based mark-to-market threshold amounts. A Credit Support Annex (CSA) is the legal document which regulates credit support (collateral) for derivative transactions. A CSA is one of the four parts that make up an ISDA Master Agreement, but it is not mandatory. Some classes of cpty are legally restricted from posting collateral and even impose 1-way CSA against their Bank cptys, although such instances are much more rare than pre-GFC. Banks are keen to renegotiate such legacy ISDA/CSA’s given the spike in the cost of funding their DRAs. 85% of DB’s net derivatives exposure of €41bln (after consideration of master netting arrangements and the €72 bln in aggregate collateral pledged to them, split €58bln in cash and €14bln in liquid securities) is with investment grade counterparties. Further, DB have disclosed that they actively manage their net derivatives trading exposure to further reduce the economic risk. This practice is common across the street where the credit valuation adjustment (CVA) desks are often one of the most active credit customers, given the immense scale of their books and their diversity as to cpty.

It appears a floor is in on DB equity. Near term, a lessening of the legal risk is the biggest factor in building capital to 12.5% from 10.7%. While a return to former glory is not likely in the cards, the combined view of Deutsche Bank is too pessimistic at present, in my view. DB is down 42% year-to-date in 2016 and 91% below their all time high of $159.59. The short interest in the stock is 1.68% of the float.

Less risky bank plays certainly exist, ING at 0.7x book on a move to 1x (they even make money in Germany, think FinTech) being one. JCG

Disclosure: Studying investable European banks. Long RBS pref shares and Lloyd Bank common shares. No current position in Deutsche Bank.

Investors in listed private pension companies Corrections Corporation of America (CXW), and The GEO Group, Inc. (GEO), got murdered yesterday. $CXW fell nearly $10 to close $17.57 (mkt cap $2.1bln), down 35% on the day, with $GEO closing down 40% to $19.50 (the smaller of the two, mkt cap $1.44bln).

Most articles published since that I have read focus on the morality issues, but IBC readers have their own steady compass on that front, the Peanut Gallery is here to guide your investment thinking and analysis when tape bombs like Deputy Attorney General Sally Yates memorandum to the Bureau of Prisons (BOP) hit the wire (link to actual letter at top of post). Amazon’s Washington Post broke the story that stated the US Justice Department plans to end the use of private prisons.

This is a big deal and should not be discounted as a driver of the valuation of these companies going forward. The Democrats have had this issue on their radar for some time. Obama has been keen to push reforms of the criminal justice system in the US, acknowledging the fact that the US incarcerates too many,almost 0.7% of the entire population (the “1%” nobody likes to talk or think about) with an undue weighting of African-American inmates (2.7% versus 0.5% for other races). It is clearly too late for “Obamabars” or whatever catchy reform slogan they might come up with, but Hillary is clearly ready to take the baton and she is not likely to miss the hand off. In her well publicized tweet of November 2015 Hillary tweeted, “We need to end private prisons.” The aforementioned prison outsourcing stocks were down 4-6% of the day of the tweet, but bounced back in the absence of immediate follow up. Enter Sally Yates.

The typical legacy contracts which granted private prison operators 20 year terms with 90% occupancy will be no more. More lucrative deal which were negotiated on a “set price” basis, irrespective of occupancy levels, will likely be re-negotiated.

The Bureau of Prisons (BOP) contracts for Federal prisons and have traditionally have up approximately 1/2 of the revenues for both $CXW and $GEO. State and Municipal contracts make up the remainder and while BOP’s directive will have sway going forward, the pace of contract roll-off will likely be measured due to tight budgets.

While only 8% of Federal prisoners are housed in private prisons, 62% of immigration detainees are housed in private facilities. Immigration & Customs Enforcement (ICE), a division of the Department of Homeland Security (DHS) are the ones that contract for immigration detainees. Immigration offenses now exceed drug offenses in absolute number and full 1/3 of all Federal criminal cases are immigration related.

Politicians, regardless of level of government, do not like having things blow up in their faces. When the US already spends 6x more on prisons than on education, cost containment will be key as BOP figure out the optimal way to respond to the clear DOJ directive (a 5 year run-off period has been assumed).

Private prisons are officially in the “sin” category along with tobacco, liquor, and casinos.

What to do. My focus will be on $CXW; Correction Corporation of America. For those, like myself, without current exposure to either name this is a time for study and analysis.

Brave analysts to comment thus far appear to be in the buy the dip (BTD) camp and appear to have a modest preference for $GEO over $CXW, speaking to the listed equity. Looking at the capital structure, $GEO has more debt, $2.23bln with Senior secured rated Ba3 and Senior Unsecured rated B1. CXW was upgraded by Moody’s to Baa3 in June 2015 and has $1.4bln in debt.

CXR 4.625% May 2023’s were not immune from the carnage of yesterday’s trade, falling from $102 to $85.50 (-16.2%) on the day. My expectation would be for the equity to rebound from the current levels and for the bonds to drift lower concurrently. The catalyst for a sharper move in the debt would be loss of investment grade rating by Moody’s. Assuming the debt is taken back (i.e. downgraded) to Ba2 (speculative grade) from investment grade there may be an opportunity to buy the debt ($70.00ish) on a hedged basis, shorting $CXR equity to the expected recovery rate on the bonds. As this opportunity unfolds, I would expect there would be cuts to the dividend on the common shares which would reduce the negative carry on the hedge.

The closest proxy I could come up with in analyzing private pension debt is military housing debt. To be clear, no analogy is to be drawn between criminals and brave service men and women that protect the nation, this is purely an asset valuation exercise. A large portion of the USA’s military housing has been privatized. The debt issued is not municipal debt, an important distinction, but is supported by the “Basic Allowance for Housing” (BAH) that is earmarked annually as an appropriation from the Federal budget by the Department of Defense (DOD), the world’s largest employer. On balance, the location of the private military housing complexes is favorable (something to think about as bases get slated for closure on occasion) to private prisons. Military housing has a much better alternate use as well, including civilian use and/or re-purposing.

The fix is in, it would appear. Private prisons will be as popular as a coal seam in the Appalachians. Trade accordingly. JCG

The U.S. Financial Crisis 2007-2008, The Global Financial Crisis (GFC for short) and the Great Recession 2008-2012 all seem to have become interchangable terms. I recently came across some journal notes I made at the peak of the crazy in 2008. The reason for the note timing was my thought was that we were going through an unprecedented time in financial history that would have clearly have a deleterious effect on the world at large. I had just read some diary excerpts from my great-great-grandmother Henrietta’s diary, written circa 1905-1908, which got me thinking I should get pen to paper in case this page of history was of interest in another 100 years.

4 September 2008

“Ruthless markets continue. Dow < 300, NASD < 65. Merrill Lynch has now taken write-downs equivalent to 25% of all of the money they have made since they came into existence.”

We all had little idea that we were in the relative early innings. The S&P which was at 1217 coming into September 2008 would eventually fall another 45%.

5 September 2008

“If you find a path with no obstacles, it probably does not lead to anywhere.”

10 September 2008

“What a week! Sunday the Fed took over Fannie and Freddie Mac. Monday the Dow was up 300. Tuesday Lehman was down 45% and the Dow off 300. No trending markets to report.”

11 September 2008

“9-11 anniversary overshadowed by carnage in the financial markets today. Lehman sub $4 (was $17 on Monday). It does not look good for them.”

15 September 2008

“One of the most dramatic days in the history of the financial markets. Lehman Bros. files for bankruptcy, Ch. 11 late Sunday. Bank of America bought Merrill Lynch for $29 (1.8x book) in an all stock deal. Merrill Lynch closed at $17 on Friday past. Lehman to zero, incl. the pref I bought as a punt (oops). The risk reward was very good.”

17 September 2008

“This is getting comical, if it were not for the massive wealth destruction left in its wake. Last night the Fed took the reins of AIG, replacing management and taking an 80% stake in return for $85bln 2 year bridge loan at Libor + 8.5%. Wow. Yikes. Mommy.”

8 October 2008

“Quite a gap in my notes due to a new level of fear in the global markets. A truly scary time for all. No country or company is being spared here. Very glad to have my health, and to be young (relatively).

28 October 2008

“The smashing of dreams is not over. A wild month with everything cut in 1/2, read down 50%. The only currencies trading up are USD and JPY. USD/CAD from parity to 1.30. Trying to remain positive.”

Fast forward – 17 August 2016

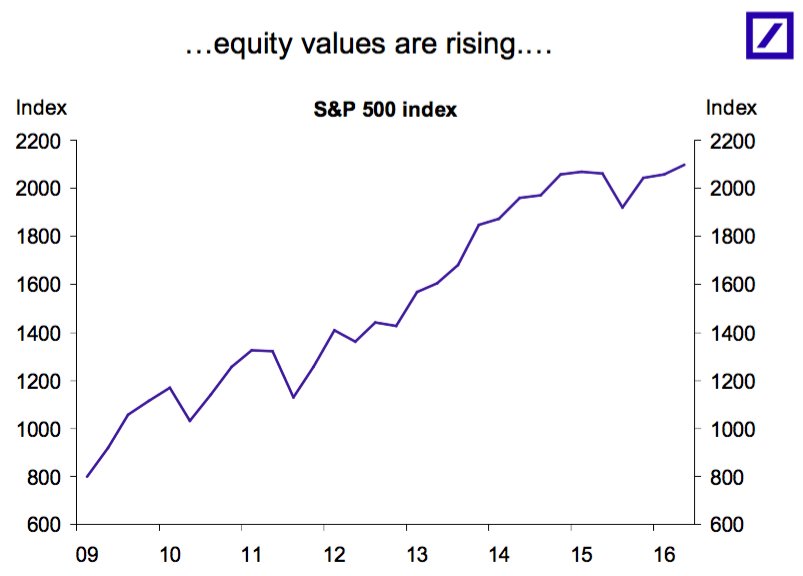

The current relative lack of volatility in the financial markets, masked in large part to the continuing largesse of global central bankers, makes the perilous 2008-2009 lows seem further back in history than the scant 7+ years it has been. The 17-month equity bear market which ran from October 2007 – March 2009 resulted in a near 50% drawdown in the S&P, finally basing at an ominous 666 on March 6, 2009. The return over the ensuing 7.45 years to the present S&P level of 2178 is a 17.25% compounded annual return. Nobody knows where we go from here. The thumb on the scale from central banks makes traditional metrics all but useless in charting the future course. The financial outcome will likely come to be inextricably intertwined with geopolitical outcomes.

NIRP has been a certified global failure. The banks are in triage. Only the Canadian and Australian banks trade > 1.0 book. Both Bank of America and Citi trade < .6x book and they are expensive compared to the European banks which are further behind in their capital raising efforts (DB price to book 0.26x). Global insurers are in the waiting room and feeling ill. A concerted move by the Fed, the ECB and the MoF to 1% would do a lot more to cure the ills of the global markets than to use the little remaining runway they have on the false hope of fighting the ogre of deflation in their theoretically walled nation(s).

Trading based on global interest rate differentials is poppycock as the hedging methodology for global fixed income is 100% clear. FX is ALWAYS hedged in foreign fixed income as the the vol of the fx moves dominate the vol of the underlying bond returns. Those thinking UST are a buy because Bunds or JGB’s are yielding negative need to give their head a shake and look at the empirical evidence.

This relatively recent phenomenon (on a 100 year time line) of allowing the non-profit maximizing players (i.e. central banks) to call the shots for a prolonged period will end in tears for all involved. JCG

Fri Aug 12, 2016 9:23pm ESTComments Off on $CXRX CONCORDIA INTERNATIONAL CORP. – SHAREHOLDER ATTENTION DEFICIT DISORDER

$CXRX IPO January 3, 2014.

Concordia International, regarded as the Canadian little sister of Valeant, was taken to the mat in Friday’s trade after a disaster of a Q2 2016 earnings report. Including after hours action, a full 40% was taken off the market cap of $CXRX ($510mm now). A $0.04 earnings miss (“adjusted” earnings of $1.38 vs. $1.42, < 3%) does not normally elicit such revulsion, but in concert with horrendous un-adjusted (i.e. GAAP) numbers, reduced forward guidance, departure of the CFO, and abolition of the dividend, all that was missing was a crow’s foot from this steaming mess of a report.

The qtly GAAP loss was -$570.5mm (-11.18 per share), largey due to the write down in the value of Plaquenil and Nilandron, both of which are under assail from generic drug competitors.

Founder, Chairman & CEO Mark Thompson formerly worked at Biovail, before Valeant tucked them under their wing in 2010. Concordia has been highly acquisitive since their formation, spending $5bln since 2013 (Covis and AMCo being the largrest). The focus has been on buying legacy drugs (i.e. buying spent oranges and extracting more juice from them) and tweaking the pricing (i.e. not lower).

A great deal of debt was assumed to finance the aforementioned m&a binge. Total debt is $3.3bln. The benchmark (cusip EK849878) US$735mm 7% April 15, 2023 , issued in 2015 to finance the Covis aquisition, broke through $80.00 in Friday’s trade to settle in the high $70’s. I would expect the rating agencies to take action, now that the horse has left the barn, in the coming weeks. CCC, aka “fish hooks” are likely in the cards. Credit ratings are alphabetic, it should be kept in mind. A is good, C much less so and D stands for default. Expect analysts that have not yet suspended coverage to turn their attention to recovery rates. The base case recovery rate assumption on Concordia debt, in a tap out situation, will likely not have a 7 handle, as in 70 cents on the dollar.

There are many unknowns for equity holders. The trading range on $CXRX has been a wide $9.65 (Friday’s intraday low) to $89.10, sitting 88% below their all time high. The margin for error on execution going forward is very low. Jesus take the wheel. I’d give it a wide berth. JCG

Thu Jul 28, 2016 9:05am ESTComments Off on INCOME FUND – PIMCO FUNDS GLOBAL INVESTOR SERIES; $PIMCMEI.ID

All investors have been extremely challenged to select plausible investments for the fixed income portion of their investment portfolio in the current environment. With so much of the world sovereign bond markets trading at negative yields, it is certainly a perilous time to be a fixed income investor. Alternative fixed income and unconstrained funds are all the rage.

This brief article introduces PIMCO’s venerable offering which is a global multi-sector fixed income fund. PIMCMEI is an open ended fund, incorporated in Ireland. The fund seeks and delivers high current income, 4.06% monthly at present. The fund duration is a modest 3.1 years.

PIMCMEI is up 4.81% year to date in 2016, compared to 7.43% for the S&P. This return comes with a lot less drama of course, as anyone long equities through February 2016 can attest.

The MER for the retail fund is high at 1.45%. PIMIX is the institutional version with a more modest MER of 0.45% but for $1,000,000 plus invested. The standard deviation of PIMIX is 2.81% and the Sharpe Ratio is a remarkable 2.01. The Sharpe ratio calc first subtracts the risk-free rate from portfolio return then divides the result by the standard deviation of the portfolio return. As a point of reference the S&P 3 year std. dev. is 11.23% and the 3 year Sharpe ratio is 1.02.

Pimco’s Daniel Ivascyn, CIO is the PM for the fund (est. 12/2012), assisted by Alfred Murata. Ivascyn, not yet 50, took over from aged Bill Gross as the “Bond King” at Pimco. The retail targeted PIMCMEI manages > $15bln and PIMIX has > $60bln in AUM.

I’m also long some of Gunlach’s Doubleline funds, but nowhere near the scale.

Wealth managers like the consistent Pimco Income Fund returns and offer up to 4x leverage on investment in the fund at Libor +50/+75 depending on the size of the relationship one has.

Clearly this fund gets many things right. The brain trust at Pimco is substantial and all PM’s benefit from the rigorous Secular forum, run annually, which looks out 3-5 years. The sister Cyclical forum takes a 12-18 month view and between them have allowed Pimco to get to the carrot first, in size.

For non-US investors, the PIMCMEI fund attracts no withholding tax and is not subject to US estate taxes given the Ireland domicile.

The fund fact sheet can give you a good window on where Pimco currently sees value. Weighting in high yield are low in comp to emerging markets. The highest weighting is in US mortgage backed securities at present.

Don’t write off fixed income just yet, you just have to dig. JCG

Disclosure: Long PIMCMEI levered 1:1. Leverage to be reduced as 3 month Libor setting reaches 1% (mid 2017?).

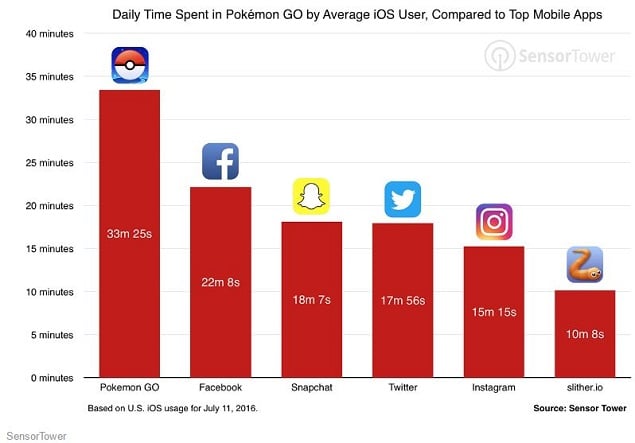

Pokemon Go, get used to hearing a lot more about it.

Thus far the limited release, including the all critical USA market, has been record setting.

From a trading perspective, the pin action has been awe inspiring, but without the wide trading ranges one would expect of daily double digit gains in the stock price of Nintendo. Buys have been exceeding sells by a factor of 7:1 on some platforms over the last week. Lower left to upper right as Gartman would phrase it. Nintendo officially has game, mobile game.

The global roll out of Pokemon Go is underway. I’m reporting from Japan, home of Nintendo (ticker 7974 on the Tokyo Stock Exchange), where fans can’t wait to get access to the app and begin their frolicking. The Japan roll out appears to have been set coincident with the end of the rainy season in Japan. As an outdoor “augmented reality” experience, Pokemon Go is best launched without torrential rainfall, hence I expect a release date the last week of July. The rain spigot ceases like clockwork around the 20th of July in Japan. Expect take up rates on app downloads, usage, paid users, $1 pokeball sales and overall hype to pierce the giddy precedent set by the US market.

The opportunities for Nintendo to exploit their extensive catalogue of intellectual property is immense. Pokemon, developed in 1995 by Satoshi Tajiri was already raking in $2bln in revenue per annum for Nintendo. Generations of gamers know the sketch, keeping advertising cost down and hence margins high. Others have pointed to the immense retail deals that could result with global franchises keen to build a stable of pokemonsters to drive traffic and resulting $. Poketourism can’t be far behind, I kid you not.

The many, including me, not yet long should study further for rational entry points. Shorting this rocket is not something characterized as an investment activity and should not be considered.

Nintendo has over $7bln on cash on their balance sheet and no debt. The previous high in the ADR’s was $78.50 in 2007 and there are 15% less shares outstanding now (held as Treasury stock by Nintendo, now the largest sole shareholder of Nintendo stock via timely buybacks at much lower levels).

The current $33.38 price for the ADR’s has come too fast, but it is difficult to fade this move for the multitude of reasons noted. Nintendo has a market cap of $32bln at present.

Pokemon Go was developed by Niantic Inc., a Google spin off which Nintendo holds a 32% stake in (yet another reason to own Alphabet too). One can bet there are many more augmented reality games in the wings. No gaming company has been more successful than Nintendo, who have brought 22 of the top 25 console games to market over the history of the gaming space.

The previous stock price pinnacle of JPY 75,000 (we closed at JPY 27,780 Friday last) was achieved when Nintendo’s Wii console took the market by storm, selling >100mm units. There are 2.5bln smartphones in use globally at present, and growing. Candy Crush has the record to date for smart phone penetration at 20% and it would appear Pokemon Go could easily exceed that metric. Those early to the story in January 2016 saw 3-4x upside for Nintendo shares. The recent spike of near 2x since the limited Pokemon Go launch clearly increases the risk for new holders, but it would appear a mobile gaming juggernaut has emerged in Nintendo.

For those that feel restricted trading only North American hours, the more liquid parent listing denominated in JPY, 7974.to is another option for those enabled to trade on foreign exchanges. Any medium to long term hold would be best currency hedged, as even though the JPY has rallied 15%+ at points in 2016 seems destined to depreciate versus the USD.

Play safe and trade safer. JCG

PS: Follow me on twitter, Caleb Gibbons @firehorsecaper

Mon Jun 27, 2016 5:33pm ESTComments Off on United Kingdom 2.0 – Installation Unsuccessful

Note: Problems at the Channel Tunnel

#Brexit caught many off guard, including yours truly. Tilted toward European equities going in and even chopped around long GBP versus USD as the referendum results cascaded in (tight stops, thankfully).

I have read that the referendum was taken with as much seriousness as an opinion poll, but clearly the real life effects have had the finality of triggering a guillotine. The head has been severed and is “in motion’. A brief respite at 1.37 has given way to 1.32 versus the Greenback.

At US$2.9tln, the UK is the World’s 9th largest economy and the 2nd largest in the EU, but clearly not for long. The UK accounts for 4% of global GDP which to put it in context is almost 2 Canada’s (1.8x rounded).

78% of the UK economy is service driven, on par with the US economy. London is the largest financial centre globally, followed by New York, Singapore, Hong Kong and Tokyo.

In terms of financial market importance, some have drawn parallels to German re-unification in 1990. At that time, there was talk of London losing some financial centre dominance in favour of a Paris, Frankfurt, London triangle. Such fanciful plans never came to fruition. On this go around, the spoils could be strewn further afield, think Dublin, Zurich, Luxembourg, Hong Kong, Singapore, Bangkok and Mumbai.

#Grexit was enough to upset the EU yogurt cart previously (US$220mm GDP). #Brexit, scaled by GDP, is 12x larger.

The Fly was all over the UK S&P downgrade story this afternoon before I could get my wonky vaca wifi to cooperate and it was laid bare, a 2 notch downgrade to AA, remaining on negative outlook. Fitch, the Sanders of the rating agencies, also downgraded post close today by 1 notch.

Value has yet to emerge in global equities. Higher than usual cash balances should be employed in such a treacherous market environment. Think capital preservation. Clearly the baby is being thrown out with the bath water is some sectors, and values will emerge.

I’m keeping a watchful eye on $ING equity, down 20% since last Wednesday (versus -40% for RBS equity). $ING Exodus stats again signals at threshold for both tech and hybrid OS. A 7% handle on dividend yield served as a good threshold for buys coming out of the global financial crisis in comparable globally safe banks (dominated then as now by the Aussie and Canadians).

USD/JPY is a decent barometer of the patient’s risk appetite and we probably need a clear break above 105 over the next week to signal anything near “all clear”. JCG

Intercept Pharmaceuticals, Inc., waiting until almost midnight, the Friday before the Memorial Day long weekend, 5/27/16, announced the FDA approved Ocaliva (Obeticholic Acid) for the treatment of the liver disease PBC (primary biliary cholangitis), formerly known as primary biliary cirrhosis. Approval was largely expected (the FDA Advisory Committee had previously voted 17-0 in favour), but the good news appears to be that the conditions attached to the approval are modest. Safety concerns had some worried that sales could be hampered by restrictions on use in patients with moderate or severe hepactic impairment, but the prescription label has no such restrictions from my reading of it (link for your perusal): ocaliva_pi

PBC is a rare, autoimmune cholestatic liver disease that puts patients at risk for life-threatening complications. PBC is primarily a disease of women, afflicting approximately one in 1,000 women over the age of 40.

Sales of OCA will begin In 7-10 days and expectations are that peak sales could reach $2.6 billion per annum. $ICPT closed Friday at $141.77 with a market cap of $3.5bln. With a typical valuation of 7x sales, clearly there is scope for a rally from here. ICPT’s float is small at 17.44mm shares and 3.4mm shares (19.5%) are held short. 78.5% of the shares are held by institutions. Fidelity Investments is the largest holder with almost 15%. The lifetime high for the stock was $462.26, which will not likely be eclipsed until OCA for NASH (fatty liver) is approved in early 2019, which obviously depends of the results of the 2,000+ patient Phase III global trial.

Another likely scenario is an approach from a larger player seeking a blockbuster drug to add to their stable. With OCA approved for PBC there is now a risk buffer to await the 2018 outcome of the phase 3 “Regenerate” trial for OCA in the treatment of NASH. Nonalcoholic steatohepatitis (NASH) is a significant metabolic form of chronic liver disease in adults and children effects a much larger percentage of the population that PBC. The OCA dosage for the treatment of PBC are 5-10mg whereas for NASH the trial is being conducted at dosages of 10 and 25mg. There are currently no drugs approved for the treatment of NASH and OCA for PBC is the first liver drug approval granted in the last 20 years. PBC & NASH are distinct, progressive liver diseases. Both diseases may lead to fibrosis and cirrhosis of the liver. From a valuation perspective most would argue 20% to the PBC application of OCA and 80% to the much larger NASH opportunity.

XBI the SPDR S&P Biotech ETF is -26% ytd in 2016. ICPT is the 4th biggest holding in the ETF at 2.6%.

What lies ahead:

Next week analysts will be tweaking their ICPT numbers based on the terms of the OCA for PBC approval. Most recently MS moved to underweight with a price target of $80. Stingy indeed when ICPT have > $22 a share in cash on their balance sheet! Merrill Lynch have an underperform on the stock and a $144 target. ML used to be the biggest bull on ICPT, with a target > $800 per share when Rachel McMinn Ph. D covered them, before joining Intercept Pharma as Chief Business & Strategy Officer in April 2014.

The street conjecture will also begin as to the timing of a bid and take-out premium likely on a bid for ICPT, now that a level of uncertainly has been removed. JCG

Disclosure: Long ICPT, 3% weighting, trailing stops, not inclined to sell < $200.