Exxon took advantage of ultra low absolute rates to build on their war chest of liquidity, keeping the rating agency wolves from the door. XOM is rated Aaa/AAA and this monster bond issue matches Apple for the 2nd largest of 2016 year to date. Issuance is down considerably year to date by number of issues, but is only down 3% by volume given the huge scale of the issuance that has been brought to market.

The two biggest tranches at $2.5bln each were the 10 year (spread of +130bp to UST) and 30 year (+150 to UST from initial price talk as wide as +180 over). Apple (Aa1/AA+) as a reminder came at +150 (20bp wider than XOM) and +205 in longs (55bp wider).

Very little to complain about here. A non gas & oil name could have purportedly come 25bp tighter, but these are very attractive all-in funding levels. Japan issued 10 year at a negative yield for the first time ever. German 10 years are at 0.10% (10bp) so you would have to hold to maturity to make 1%. The folly of this will become evident with the passage of time.

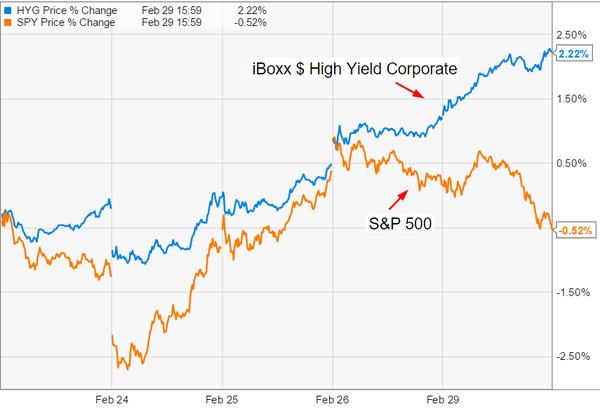

We stand with oil closer to $40 than $20 which is a good thing. High grade debt aside, we have seen a sizeable recovery in CCC rated debt and the high yield space has de-coupled from the equity market the last week of February (outperforming smartly with spreads tighter by 100bp in 2 weeks), a positive sign for risk assets for those focussed on looking forward. March is typically a positive month for risk assets.

In related news, Goldman was finally able to get a challenging bond deal done for Solera, the Caa1 rated risk-management software company on the same day. The size was scaled back from $2bln to $1.73bln ($300mm in leveraged loan bump to make up the difference) on a 10.5% 8NC3 (8 year final, non-callable for 3 years) at a price of $95.00 for an effective yield of just under 11.50%.

Useful as a point of reference, as it gives you current “book ends” of what fixed income returns are achievable in the current market, Japan 10 year JGB -0.024%, 10 year German bunds 0.10%, 10 year US Treasuries 1.75%, 10 year XOM 3.05%, 8NC3 SOLERA 11.5%. JCG

If you enjoy the content at iBankCoin, please follow us on Twitter

30 year, uh, no, yeah, no…

CRC awakens this week!