Apple brought a $12 bln debt offering today in 9 parts. This was the 2nd largest debt deal of this year after AB InBev’s $46bln deal. Many scratch their heads at why a company with as much cash as Apple has issues so much debt. The biggest reason is that Apple’s cash is largely held offshore, and to repatriate it would be costly from a US taxation perspective. Another reason is the pricing of the debt, due to the fact they had $26bln in orders (order book) for $12bln of bonds, which allowed them to issue at a tighter spread;

$500mm 2 year fixed printed at +60 US Treasuries (UST) versus guidance of +60 and initial price talk (IPT) of +75

$1bln 3 year fixed printed +80 UST vs matching guidance and +90 IPT.

$500mm 3 year FRN printed L+80 versus matching guidance.

$2.5bln 5 year fixed +105 UST, in from +115 IPT.

$500mm 5 year FRN L+113.

$1.5bln 7 year green bond, +135 UST vs +145 IPT.

$2bln 10 year fixed +150 UST vs +160 IPT.

$1.25 20 year fixed +190 UST versus +200 IPT.

$2.5bln 30 year fixed +205 UST versus +215 IPT.

There is strong demand for high grade debt with no tithe to the oil & gas or mining & metals sectors. Apple is rated Aa1 by Moody’s.

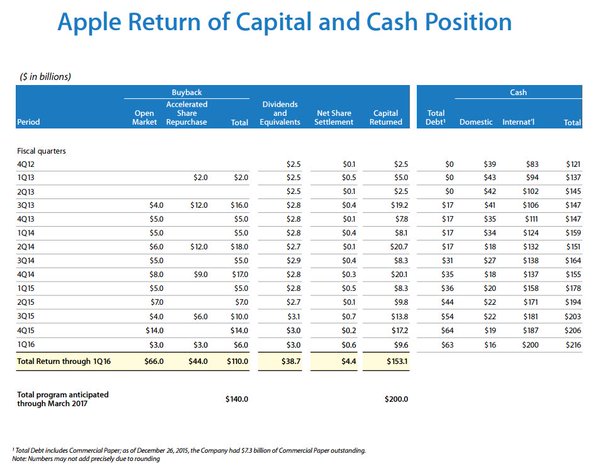

The following details the split between domestic and offshore of Apple’s cash hoard, quite striking:

Moody’s noted that at the current issuance trajectory, Apple could have $100bln of debt by the end of 2017. There has been a great deal of debate on the merit of a tax amnesty on foreign profit for US corporates. It has been done before (5.25% instead of typical 35%), but it is not politically correct to suggest an election year is the time to do it again. There are risks to delaying. Tax inversions should be easier for cash rich tech companies that already outsource critical components overseas. JCG

If you enjoy the content at iBankCoin, please follow us on Twitter

Should be a nice fight between those shorting off Icahn and Einhorn’s selling and AAPL’s buyback.

92 – 107 range anyone?

Firehorsecaper- This is interesting. Thank you for taking the time to blog about areas of your interest and expertise. Here’s a comment from a consumer. It’s not meant to slam you, just an observation…

I hope well-paid and skilled people at Apple are focusing on these financial matters, enabling company leadership to focus on Apple’s products, the consumer and competitive marketplace. Did Apple initially make that cash as an enterprise driven by financial operations?

mx2101 One would hope the company focus in on forward looking innovation (the internet of things) and that the mgmt of a war chest 68% the size of Berkshire Hathaway and almost 6X Harvard University’s endowment is largely if not completely ring-fenced. The skills sets are quite different, I would imagine. Apple has a knack for picking the low’s in yields for certain which might have some looking at TBT tactically and to hire/poach their staff (computer?).

Great article, right to the point and succinct. A couple quick follow ups. First, what do you mean by $26bln in order for $12bln of bonds; what does that $26bln represent? Second, do you mean $100bln in debt by the end of 2017, not $100mln? Thanks!

Boyaj, As they priced it well they had a huge order book for the deal. Only the 2 year FRN was dropped and the biggest demand was for the longer dated fixed rate tranches. On debt extrapolation I meant 100bln.