Image: Propery of Bill Watterson

My three months as a tabbed blogger on iBankcoin come to an end today. It has been a pleasure writing again on iBC and I hope those who have read this tab have come away with a better understanding of the relationship between the weather and the market, just weather, just the market, or at least the meteorological rational behind the unfortunate lack of hurricanes this summer.

I would apologize for that if I could, but we will just have to take it up with the Weather Gods when we get up there. Compared to last summer when it seemed we were getting hurricane plays every week, blogging during the summer of 2009 has been the meteorological equivalent to offering trading advice on 90 consecutive Labor Days, Columbus Days, or whatever other silly stock market holidays there are. In other words, it’s rather difficult to make money when your market isn’t open for business. Don’t say I didn’t warn you–In my first post this summer, I remarked that “the 2009 hurricane season is going to blow if you are a fan of death and destruction and rock if you have a house out on Key West.”

That being said, I, like many traders on iBC, had a stellar summer. My best call was likely the decision in mid-August to dump my largest position, the Natural Gas Fund (UNG), as it showed signs of de-coupling from the commodity it tracked, for a <5% loss and using the assets to buy a truckload load of Chesapeake Energy, which I am still holding up 40%. Since June, I am up roughly 25% on my portfolio.

I leave you with both a few short Short-Term thoughts and a few longer Longer-Term thoughts.

Short Term Thoughts

- Hurricane season is NOT over. I still expect we will see another 2-3 named storms, although the chance of any of these affecting the United States as a hurricane becomes minimal by the second week of October.

- Stay away from the refiners, at least for now. I know they are cheap, but the low crack spread does not fundamentally support a rally in the sector.

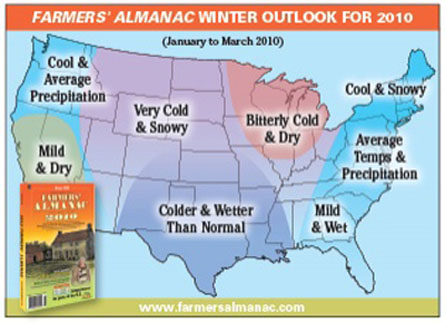

- Look for natural gas to pullback from its current price ($4.80/MMBTU) as it is up roughly 100% from its lows just three weeks ago. However, Based on my post yesterday discussing the upcoming winter, I believe the combination of a colder-than-average winter and rig count cuts may resolve our current supply glut and may put the commodity on a long term road to recovery. I continue to hold CHK, SWM, and FTK in the NG/energy sector.

- The PPT is a tool of the gods and should be taken advantage of. It will pay for itself in the first week if properly utilized.

- Life will get better in the Pacific Rim. They’ve had a rough couple of days–Typhoon Ketsana delivers epic flooding in the Philippines and Vietnam killing over 200 people, a tsunami in American Saoma washes a mile inland, killing untold hundreds leveling entire villages, and now Indonesia suffers a 7.0 earthquake potentially killing thousands. Those of us bemoaning the lack of Atlantic hurricanes should be counting our blessings.

Long Term Thoughts

I have stated several times that I would do a global warming post at some point during my time as a tabbed blogger. Because, you know, I’d hate to finish up on a positive note or anything…

Quickly, I believe in the phenomenon of climate change and I believe that it is caused by anthropogenic influences. You will find very few climate scientists out there today who refute the existence of global warming. Rather, the occasionally heated debate revolves around the severity and timescale of the warming. These are now the people who are commonly referred to as “Skeptics.” I have had the opportunity to work with such a scientist and I believe I greatly benefited from seeing both sides of the coin.

Anyways, instead of pulling out an epic Here’s-Why-Your-Great-Grandchildren-Will-Drown sort of post, I am going to focus on one particular aspect of climate change that I believe the be of greatest concern in our lifetimes: The melting of the Polar Ice Caps.

First, to refute one commonly held belief: the melting of the polar ice sheets will NOT directly contribute to sea level rise. Because they are floating on top of the Arctic Ocean and displacing their weight in water, their complete melting theoretically should contribute zilch to sea level rise.

What is of concern, however, is that the melting of the polar ice caps is part of a proposed positive feedback cycle (aka a Vicious Cycle) that has the potential to accelerate the rate of warming much faster than has been projected by many climate models. Here is how it works.

- Humans burn carbon-based fuel which generates carbon dioxide.

- The carbon dioxide behaves as a greenhouse gas raising the temperatures a small amount.

- The marginally elevated temperature slightly accelerates the melting of the Polar Ice Caps exposing more of the Arctic Ocean during the summer melt season. This is the stage we are right now.

- The Heat Capacity of water is greater than that of ice, meaning that is better at absorbing incoming radiation (i.e. heat) rather than reflecting it back into space. This introduces the idea of an Albedo, or the extent to which an object reflects rather than absorbs light, expressed as a ratio. Sea Water has an albedo of near .90 while sea ice has an albedo of around 0.70, meaning sea water absorbs more heat than ice.

- Newly exposed ocean absorbs more heat than the ice that used to cover it, compounding the warming from greenhouse gasses

- This leads to further ice-cap melting, exacerbating the compounded warming, which melts more ice, and so on and so forth…a vicious cycle that feeds on itself.

This is illustrated in graphic form below in Figure 1 for the visual readers.

Figure 1: Proposed positive feedback loop due to the melting of the polar ice caps

Polar Sea Ice is generally very thin (less than 75 feet thick) compared to continental glaciers (over a mile thick) and thus it forms a very cyclical pattern of melting during the summer and reforming during the winter. Figure 2 below shows the maximum extent of ice coverage in March following winter and in September following the summer melt season.

Figure 2: Maximum ice extent in March after Northern Hemisphere winter and minimum extent in September after summer (Source: National Snow and Ice Data Center)

Basically, this transient nature of sea ice means that the polar ice cap is very vulnerable to small changes in temperature when compared to more permanent continental glacial ice. Since it responds very quickly to small changes in temperature, it is also a very sensitive measurement of global warming.

Polar ice caps have been melting consistently since the mid-1970s (and probably before that, though detailed records were not kept), with the pace accelerating over the past 10 years. 2007 saw the greatest melting on record, with the minimum ice extent in September diverging nearly 5 standard deviations from the 30-year mean, or about 60% of normal.

For the past three years including this summer, the melting has been substantial enough to open the fabled Northwest Passage around Canada and Northeast Passage around Russia for the first time since the human race has turned its eyes to the seas. One final piece of investment advice: Take a look at Canadian and Russian shipping companies. They could make a bundle off of this once the various license agreements are sorted out.

Anyways, the extent of arctic sea ice melting since the mid-1950s is shown below in Figure 3.

Figure 3: Ice Cap extent, deviation from 30 year average (Source: National Snow and Ice Data Center)

You will notice that the past two years have seen a bit of a recovery. However, I just equate this to an “oversold” rally, in which some negative feedback mechanisms/flukey cold winters kick in and stop the bleeding. Figure 4 below shows the melting over just the past five years and indicates that while 2009 is comfortably above 2008 and 2007, it still remains more than 2 standard deviations below the mean.

Figure 5: Polar Ice Cap melting over the past four years, compared to a 20 year average (Source: National Snow and Ice Data Center)

I predict with near 100% confidence that we will see new arctic sea ice lows within the next five-to-ten years. There is even an outside chance that sea ice may disappear altogether during the summer months by 2030-2040.

Okay, so based on the Positive Feedback cycle I outlined above in Figure 1, the next step in the cycle is warming of the water exposed/near the melted sea ice due to its increased heat capacity. Well, Figure 6, which shows sea surface temperature anomalies for this past August, indicates that the greatest warming is localized in the extreme northern latitudes exactly as expected.

Figure 6: Sea Surface Temperature anomalies showing the greatest departure from average in the far northern latitudes. Some warming is also seen in the equatorial east Pacific, indicative of a weak El Nino (Source: NOAA)

Such extreme (>5 degree) warming in the arctic has been a common theme in the arctic for the past half decade or so. Global temperatures respond much slower and it will be several years before we begin to see the effect of melting polar ice caps on accelerating the rate of Global Warming. In the short term, however, I expect the warming of the Arctic Ocean to continue to positively feedback on the rate of sea ice melting and a gradual downtrend of summer polar ice coverage will resume.

What will be the end result should the ice caps vanish for part of the year? There are several “doomsday” scenarios that result in runaway climate change, and while I am somewhat skeptical of all of them, I see the rapid increase in warming from melting polar ice caps as a possible trigger. These scenarios include:

- The overturning and release of carbon dioxide and methane currently sequestered in the oceans (i.e. the dire sounding “Clathrate Gun Hypothesis”)

- The accelerated melting of the Greenland Polar Ice Sheet since the continental ice sheets are no longer held back by sea ice. Compared to the melting of polar sea ice, the collapse of the Greenland Ice sheet will raise sea level (by about 20 feet)

- The collapse of the Thermohaline Circulation that drives heat transfer in the oceans. Interestingly, this is believed to have resulted in the Younger Dryas, a period of rapid cooling and glaciation about 12,000 years ago (The movie The Day After Tomorrow tries to show something like this)

- The extinction of the poor polar bears.

These theories likely sprung up as the result of a bunch of climate scientists getting together late at night in tents and trying to top each-other’s scary stories, while illuminating their faces with cheap flashlights. While they may logically make sense, there is no reason to become concerned in the short term.

.

Hurricane Identification Contest Results: All Hail DPeezy

![]() So for the past three months I have been running a contest here on my tab for readers to identify hurricanes based on an unknown satellite image. I am pleased to announce that after 90 days and 42 different storms, DPeezy has emerged the winner, defeating second place finisher Wabisabi 17-12. Props for ending on a prime number. Figure 7 below shows DPeezy’s path to victory.

So for the past three months I have been running a contest here on my tab for readers to identify hurricanes based on an unknown satellite image. I am pleased to announce that after 90 days and 42 different storms, DPeezy has emerged the winner, defeating second place finisher Wabisabi 17-12. Props for ending on a prime number. Figure 7 below shows DPeezy’s path to victory.

Figure 7: Hurricane Contest Final Rankings

I was very impressed with the weather IQ of iBC readers over the course of these three months as every single storm was ID’d. I assure you, if Accuweather or another weather site had a Ticker Symbol Identification contest, there woulld likely be a lot of crickets chirping…

For his efforts, DPeezy is awarded a hurricane warning flag like those you might see at the beach telling people to get the hell out of the water, and, most likely, out of the county.

Congratulations DPeezy. I strongly advise everybody to read his work in the Peanut Gallery. His posts focus on options, a realm that is not strongly covered anywhere else on ibankcoin. Since the founding of iBC he has been one of the most consistent posters on the site and is one of few whose posts I always take the time to read. The guy has a good work ethic, knows his hurricanes, and is one of the favorites to win the 2nd annual iBC Fantasy Football League. Quality.

DPeezy, email me a shipping address to receive your flag.

In conclusion, I would like to thank everybody who has taken the time to read and comment on my blog here. It is a rare thing to be able to write about two of the topics that one enjoys most. I would like to thank the Fly for bullying me into accepting this honor. Having followed the site since the Blogspot days, I can honestly say iBankcoin is truly the premier investment website on the web (as well as the most entertaining). Should anything of interest arise, I may post in the Peanut Gallery, either as Dr. Cane or as my old name, Veritas5. I will continue to hang out on Twitter as DrCane09 as well.

Congratulations to Henry Fool on his tab. I’m looking forward to the picks.

Peace.

Dr. ‘Cane

Comments » Obviously, today’s storm is not a hurricane, but it relates well with the theme of the post. This will be the final storm in the contest. “Awards Ceremony” tomorrow…

Obviously, today’s storm is not a hurricane, but it relates well with the theme of the post. This will be the final storm in the contest. “Awards Ceremony” tomorrow…

Figure 3: Hurricane Frequency

Figure 3: Hurricane Frequency Figure 4: Tropial Storm Ketsana in the South China Sea

Figure 4: Tropial Storm Ketsana in the South China Sea

Figure 1: Gas-Oil Crack Spread

Figure 1: Gas-Oil Crack Spread Figure 2: Crude Oil Supplies

Figure 2: Crude Oil Supplies Figure 3: Gasoline Stocks and differential between 2009 and average

Figure 3: Gasoline Stocks and differential between 2009 and average Figure 4: Refiner Capacity and Differential between 2009 and average

Figure 4: Refiner Capacity and Differential between 2009 and average

Figure 3: Current satellite of the Tropical Atlantic showing generally quiet conditions.

Figure 3: Current satellite of the Tropical Atlantic showing generally quiet conditions.