I am, because of personal preferences, going to cash in at this time. Since I’m up 49% ytd, I have the luxury of “calling it good” and kicking back to enjoy the fruits of my “labor”. Between, an Alaskan cruise, flyfishing, family reunions, trips to the French countryside and the Italian riviera….who has time to follow the market?

Ergo, I will be taking the summer off from trading. In essence, I will be “playing” all summer, just not in the market. Maybe I will learn to play a musical instrument (or not). See, I just think the market goes nowhere this summer, or perhaps, worse….

My concerns are centered around the extent of the recent run up in the stock market, the action in the bond market and interest rates, and the amount of government intervention and regulation in the capital markets.

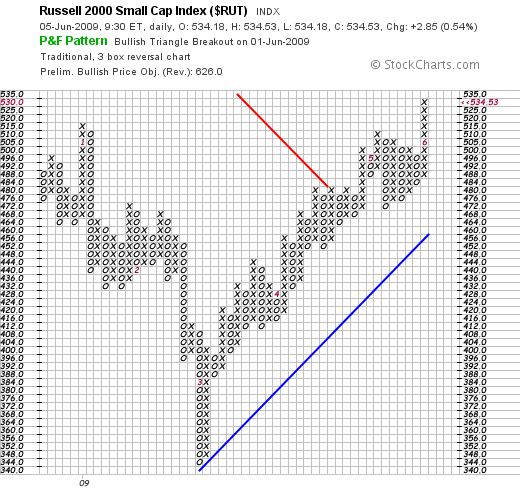

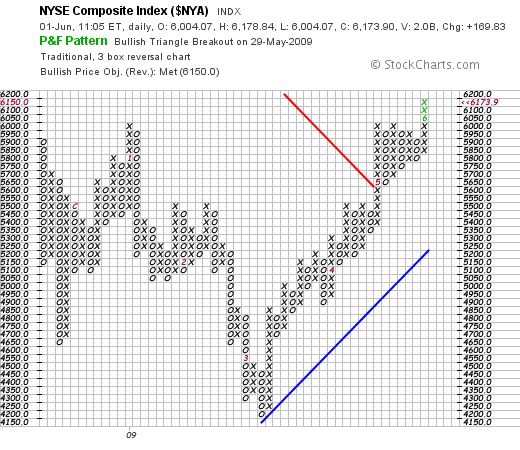

Given that the recent market rally is over two standard deviations from the annualized mean over the past 100 years, this condition will not last. It is simply a matter of time. Even now, the rally is fizzling out. Consider that many traders and investors have made egregious returns the past three months, and many will be parking their funds and taking vacations.

Economic news on Wednesday was uneventful and the Treasury market remained depressed from the open. The 10 year note auction was pitifully weak, and by midday, Treasuries were lower, with the 30 yr crashing 2 3/4 of a point, reaching a 4.833% yield before rebounding late in the day. The 10 yr yield spiked at just under 4% during the sell-off after the auction results. All this should be concerning to us all, even as the Russians announced yesterday that they will be reducing a portion of their U.S. Treasury holdings in the future. This news contributed to driving the dollar lower. Russia holds about $120 billion in Treasuries in reserves. The dollar is heading down long term.

The Chinese are of the same mindset. Maybe they won’t be selling Treasuries, but they won’t be buying in size either. (Sorry, Mr. Obama). Still, they don’t have a choice. They have to buy some Treasuries given their egregiously large trade surplus with the U.S.. So they will still be buyers, but just on a residual basis. So, where will the government get the money to fund the deficits?

Don’t be surprised if Obama uses his rhetorical skills to scam the U.S. consumer, since the consumer is in “savings mode” right now. You will be called “unpatriotic” if you don’t invest in U.S. Treasuries. Mark my word on this.

It is only common sense to believe that more government regulation and taxation means less free enterprise and available capital. Capital will leave the U.S. and seek investment elsewhere. It is coming. Add a protectionist mindset, not only in the U.S., but globally, and you have a recipe for another meltdown in the markets. The bureaucrats just don’t get it.

As for me, I will be in cash, at least for the summer, losing out on the chance to make gains, but gaining peace of mind and the enjoyment of family and friends.

However, if you will permit me to throw in my two cents: look to the commodity markets. My top picks for you non-futures traders are: DBC, FXA, FXC, and USO. Stay away from UNG, as it will go lower because of supply. I’m not bullish on gold or bearish on it either, just neutral.

On a global / macro scale, stay away from the Euro. Hold fast to the English-speaking commodity producing countries, and short the commodity consuming countries.

In closing, I bid you farewell. I have asked The Fly to take me off the active duty roster, since I will be playing “rich man”, cruising the seas and visiting my vineyards.

I’ve been following and blogging on IBC / Fly on Wall Street for over two years now. It has been a fun experience. I’ve definitely enjoyed all of you, including the personalities and alter-egos (thanks, Jake), and the banter, but more importantly the many perspectives and views on the market.

Thanks to all of you bloggers and readers, but especially a big thanks to The Fly / Sr. Tropicana / Horatio Clawhammer / Plutonium Petey, the Space Alien Magician.

Good day!

Comments »